Updated and checked May 2024. That space in your wallet or purse is valuable, and you should be the one to get that value. By being smart and picky, you can find offers worth $500+ for a single card, all to encourage you to apply and try it out. This adds up to thousands of dollars in extra income (over $5,000 in 2023). These are the top 10 credit card offers that I would personally apply for right now (or have already). Notable recent changes:

Updated and checked May 2024. That space in your wallet or purse is valuable, and you should be the one to get that value. By being smart and picky, you can find offers worth $500+ for a single card, all to encourage you to apply and try it out. This adds up to thousands of dollars in extra income (over $5,000 in 2023). These are the top 10 credit card offers that I would personally apply for right now (or have already). Notable recent changes:

Added Sapphire 75k, Hawaiian 70k, LFCU 50k, WF Journey 60k, British Airways 75K+5X, Delta 70k+$200 credit, JetBlue 70k, Alaska 75k

Added Sapphire 75k, Hawaiian 70k, LFCU 50k, WF Journey 60k, British Airways 75K+5X, Delta 70k+$200 credit, JetBlue 70k, Alaska 75k  Removed Marriott 185k, CitiAA 75k, Hilton 100k, IHG 165k, Southwest CP, Aeroplan 100k, Wyndham 75k

Removed Marriott 185k, CitiAA 75k, Hilton 100k, IHG 165k, Southwest CP, Aeroplan 100k, Wyndham 75k

This is a companion post to my Top 10 Best Business Card Offers. Small business bonuses are on average even higher than those on consumer cards.

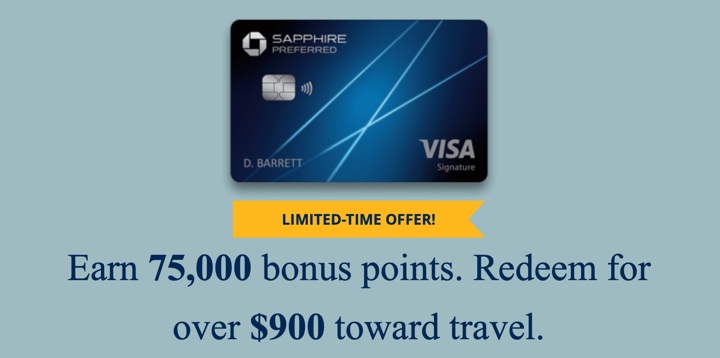

Chase Sapphire Preferred® Card

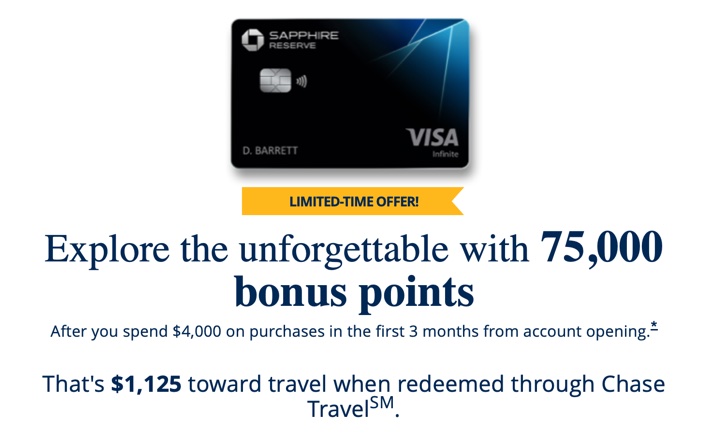

- 75,000 Ultimate Rewards points (worth $937.50 towards travel or transferrable to miles/points) after $4,000 in purchases within the first 3 months. See link for details.

- $50 annual Ultimate Rewards Hotel Credit, 5x on travel purchased through Chase Travel(SM), 3x on dining and 2x on all other travel purchases.

- $95 annual fee.

- Subject to 5/24 rule.*

- Upgrade pick: Chase Sapphire Reserve® Card. Higher travel perks including airport lounge access, higher annual fee.

British Airways Visa Signature Card

- 75,000 Avios after $5,000 in purchases within first 3 months. Also, get 5X Avios on up to $10,000 (up to 50,000 total Avios) in gas, grocery stores, and dining purchases for first 12 months. Limited-time offer. See link for details and redemption tips.

- 10% off British Airways flights starting in the US when you book through the website provided in your welcome materials.

- Free Travel Together companion ticket when you spend $30,000 in calendar year.

- $95 annual fee.

The Platinum Card from American Express

- 80,000 Membership Rewards(R) points after $8,000 in purchases in the first 6 months.

- $200 Hotel Credits, $240 Streaming Credits, $200 Airline Fee Credits, $200 Uber Cash, $189 CLEAR Plus credit, $300 Equinox credit, $155 Walmart+ credit and more annually!

- Up to $100 Global Entry or $85 TSA PreCheck fee credit.

- Premium airport lounge access through the American Express Global Lounge Collection®.

- $695 annual fee.

- 60,000 points – 60,000 points after $3,000 on purchases in the first 3 months. Redeemable towards any travel purchase with Pay Yourself Back. See link for details.

- Free first checked bags on Air Canada flights: one free checked bag for the primary cardmember and up to eight other travelers on the same itinerary.

- Aeroplan 25K Elite Status benefits for the remainder of the first calendar year, plus the following calendar year.

- Up to $100 Global Entry or TSA PreCheck credit.

- $95 annual fee.

- Subject to 5/24 rule.

Capital One Venture X Rewards Card

- 75,000 miles (worth $750 towards travel, or transferrable to airline miles) after $4,000 in purchases within the first 3 months. See link for details.

- $300 annual travel credit. Get up to $300 in statement credits when booking through Capital One Travel.

- Additional 10,000 bonus miles (equal to $100 towards travel) every year, starting on your first anniversary.

- Priority Pass + Capital One airport lounge access. Additional cardholders are free, and also get their own Priority Pass!

- Up to $100 credit towards TSA PreCheck or Global Entry application fee.

- $395 annual fee.

- 60,000 Membership Rewards points after $6,000 in purchases in first 6 months. See link for details.

- $120 in Uber Cash annually (good towards Uber Eats or Uber rides in the US).

- $120 in annual dining credit at Grubhub, Seamless, and more.

- 4X points at restaurants.

- 4X points at US supermarkets, on up to $25,000 per year.

- $250 annual fee.

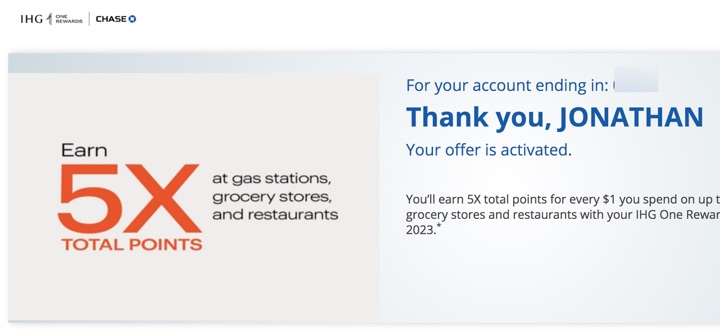

IHG One Rewards Premier Credit Card

- 140,000 IHG Points after $3,000 in purchases within first 3 months. See link for details.

- Free Night after each account anniversary year (valued up to 40,000 IHG points).

- $99 annual fee.

- Subject to 5/24 rule.

- Don’t like annual fees? The no-annual fee Traveler version also has a competitive offer with no annual fee.

- 50,000 miles after $3,000 in purchases within 3 months. See link for details.

- Free first checked bag for both you and a companion (a savings of up to $140 per roundtrip) when you use your Card to purchase your United ticket.

- Expanded award availability. Having this card makes it easier to find that saver award economy ticket.

- $0 annual fee for the first year, then $95.

- Subject to 5/24 rule.

Capital One Venture Rewards Card

- 75,000 miles (worth $750 towards travel, or transferrable to miles) after $4,000 in purchases within the first 3 months. See link for details.

- 2 Miles per dollar on all purchases.

- Up to $100 credit towards TSA PreCheck or Global Entry application fee.

- $95 annual fee.

Bank of America Premium Rewards Card

- 60,000 points (worth $600) after $4,000 in purchases within the first 90 days. See link for details.

- $100 annual Airline Incidental Statement Credit.

- Up to $100 credit towards TSA PreCheck or Global Entry application fee.

- $95 annual fee.

Wells Fargo Autograph Journey Card

- 60,000 points (worth $600 towards travel) after $4,000 in purchases within the first 90 days. See link for details.

- $50 annual statement credit with $50 minimum airline purchase.

- $95 annual fee.

Lafayette Federal Credit Union Platinum Mastercard

- 50,000 points (worth $500 towards gift cards or flights) after $5,000 in purchases within the first 90 days. See link for details.

- You must be a member of LFCU to apply. View membership eligibility options here. Anyone nationwide can join LFCU by joining the Home Ownership Financial Literacy Council (HOFLC) for a one-time $10 fee.

- Combine with LFCU new member program for potentially another $50 bonus.

- No annual fee.

- 70,000 Hawaiian miles after any purchase (of any amount) within the first 90 days. Any 6-digit code will work, like “000000”. See link for details.

- Free first checked bag for primary cardmember.

- One-time 50% off companion discount for roundtrip coach travel between Hawaii and The Mainland on Hawaiian Airlines.

- $99 annual fee.

Alaska Airlines Visa Card (Bank of America)

- 75,000 bonus miles + Companion Fare voucher after $3,000 in purchases within first 90 days. See link for details.

- Companion fare voucher is “Buy one ticket, get one from $122” ($99 fare plus taxes and fees from just $23).

- Free checked bag on Alaska flights for you and up to six other passengers on the same reservation (worth $60 roundtrip per person).

- $95 annual fee.

- 60,000 points (worth $600 in gift cards, or transferrable to miles/points) after $4,000 in purchases in the first 3 months. See link for details.

- 3X points for every $1 spent on restaurants, supermarkets, gas stations, air travel and hotels.

- Must not have gotten bonus from or closed a Citi Rewards+, ThankYou Preferred, Premier, or Prestige card in the past 24 months.

- $95 annual fee.

U.S. Bank Altitude Connect Visa Signature Card

- 50,000 bonus points (worth $500 in statement credits) after $2,000 in purchases within 120 days. See link for details.

- Up to $100 statement credit for Global Entry or TSA PreCheck.

- Includes Priority Pass Select membership w/ 4 free lounge visits a year.

- $0 annual fee the first year (effective September 9, 2024, $0 annual fee ongoing.)

Barclays AAdvantage Aviator Red Mastercard

- 50,000 American Airlines miles after any purchase and paying the annual fee in full, both within the first 90 days. See link for details.

- First checked bag free on domestic AA flights ($60 value per roundtrip, per person).

- $0 intro annual fee for the first year, then $99.

- 70,000 bonus TrueBlue points – 70,000 bonus points after $1,000 on purchases and paying the $99 annual fee in full, both within the first 90 days. Any 5-digit code should work, like “00000”. See link for details.

- First checked bag free for the primary cardmember and up to 3 companions when tickets are purchased with your JetBlue Plus Card.

- $99 annual fee.

Southwest Rapid Rewards Plus Card

- 50,000 Southwest points after $1,000 on purchases in the first 3 months. See link for details.

- Southwest still gives everyone two free checked bags.

- Timing for Companion Pass. If you can sign up for this one and perhaps also the small business version, and time the points to post in early 2024, you can qualify for a Companion Pass for 2024/2025.

- $69 annual fee.

- Subject to 5/24 rule.*

Delta SkyMiles® Gold American Express Card

- 40,000 Delta Skymiles after $2,000 in purchases within the first 6 months. See link for details.

- 40,000 Skymiles are worth at least $400 in Delta airfare with “Pay with Miles” option.

- $200 Delta flight credit after $10,000 in purchases on your card in a calendar year.

- First checked bag free on Delta flights ($60 value per roundtrip, per person).

- $0 annual fee for the first year, then $150.

- There is also a 50k bonus miles offer on the Platinum version.

If you pay off your balances every month, then you can join me and many others in funding a huge chunk of your annual travel budget with cash credits, points, and miles. I mostly use my rewards points on family trips – domestic economy flights, mid-range hotels, and cheap car rentals. If you have credit card debt, you should focus on paying that off first as the interest charges could offset most of the perks.

* 5/24 Rule? Certain Chase cards have a “5/24 rule” which is an unofficial rule that they will automatically deny approval on new credit cards if you have 5 or more new credit cards from any issuer on your credit report within the past 24 months (2 years). This rule applies on a per-person basis, so if you are new, you might want to start with those Chase cards.

The updated

The updated

Increased offer.

Increased offer.  Updated April 2024. Do you have small business income or work as an independent contractor? Freelance, Uber/Lyft, Amazon, eBay, Etsy, Airbnb? A small business credit card separates your personal and business expenses and can build up your business credit profile. If you are not a corporation or LLC, you can apply as a sole proprietorship, with your name as the business name and your Social Security number as the Tax ID number. These are the top 10 credit card offers that I would personally apply for right now (or have already). Recent changes:

Updated April 2024. Do you have small business income or work as an independent contractor? Freelance, Uber/Lyft, Amazon, eBay, Etsy, Airbnb? A small business credit card separates your personal and business expenses and can build up your business credit profile. If you are not a corporation or LLC, you can apply as a sole proprietorship, with your name as the business name and your Social Security number as the Tax ID number. These are the top 10 credit card offers that I would personally apply for right now (or have already). Recent changes:

New limited-time offer. The

New limited-time offer. The

Activation reminder for 2024 2nd Quarter. The credit cards below offer 5% cash back and up on specific categories that rotate each quarter. It takes a little extra attention, but it can add up to hundreds of dollars in additional rewards per year without changing your spending habits. You can also buy gift cards at places with 5% back now but spend the gift cards later. (* You can buy gift cards from lots of different places at grocery and drug stores…) New cardmembers may also get an upfront sign-up bonus.

Activation reminder for 2024 2nd Quarter. The credit cards below offer 5% cash back and up on specific categories that rotate each quarter. It takes a little extra attention, but it can add up to hundreds of dollars in additional rewards per year without changing your spending habits. You can also buy gift cards at places with 5% back now but spend the gift cards later. (* You can buy gift cards from lots of different places at grocery and drug stores…) New cardmembers may also get an upfront sign-up bonus. Chase Freedom Flex Card

Chase Freedom Flex Card Discover it Card

Discover it Card Citi Custom Cash Card.

Citi Custom Cash Card. American Express Blue Cash Preferred Card

American Express Blue Cash Preferred Card

The Best Credit Card Bonus Offers – May 2024

The Best Credit Card Bonus Offers – May 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - May 2024

Best Interest Rates on Cash - May 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)