Limited-time offer now scheduled to expire 1/8. If you have an Amazon Prime membership, you probably spend a good chunk at Amazon and should at least consider the Prime Visa, a credit card (not store card) available only to Amazon Prime members. During the holiday season, the bonus has boosted to a high of $250 but is going to expire 1/8. Highlights:

- $259 Amazon Gift Card *instantly* upon approval exclusively for Prime members. No spending requirement.

- 5% back at Amazon.com, Amazon Fresh, Whole Foods Market with an eligible Prime membership.

- 5% back on Chase Travel(SM) purchases with an eligible Prime membership.

- 10% back or more on a rotating selection of items and categories

on Amazon.com with an eligible Prime membership. - 2% Back at gas stations, restaurants, and on local transit and commuting

(including rideshare). - 1% Back on all other purchases.

- No foreign transaction fees.

- No annual fee.

Rewards can be redeemed easily either on your next Amazon.com purchase or as a statement credit on your bill. But since you get 5% back on your Amazon purchases on this card… it’s slightly better to take the statement credit, even though it is also slightly more hassle.

I have this card set up as my default credit card at Amazon, and that’s its primary purpose in life, to absorb all my Amazon and Whole Foods purchases. (Which is still a lot, unfortunately…)

If you do this, remember that there are also the following extra protections built into the card:

- Extended warranty protection. Extends the time period for the U.S. manufacturer’s warranty by an additional year, on eligible warranties of three years or less.

- Purchase Protection. Covers your new purchases for 120 days against damage or theft up to $500 per claim and $50,000 per account.

Bottom line. If you are a Prime member that spends a lot of money at Amazon and/or Whole Foods and prefer simplicity, using the Prime Visa can add up with minimal extra effort. Be sure to make it your default card for your Amazon account. You can then track all your Amazon spending on one card, and also be sure you remember that you get extended warranty protection and purchase protection on those items.

The updated

The updated

Updated September 2025. That space in your wallet or purse is valuable, and you should be the one to get that value. By being smart and picky, you can find offers worth $500+ for a single card, all to encourage you to apply and try it out. This adds up to thousands of dollars in extra income (

Updated September 2025. That space in your wallet or purse is valuable, and you should be the one to get that value. By being smart and picky, you can find offers worth $500+ for a single card, all to encourage you to apply and try it out. This adds up to thousands of dollars in extra income ( The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

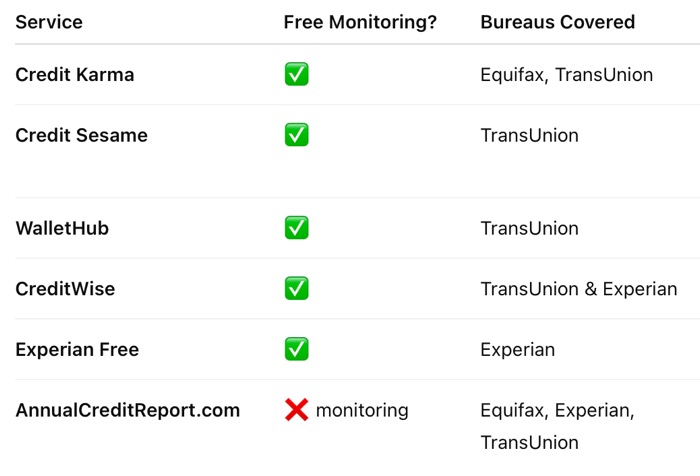

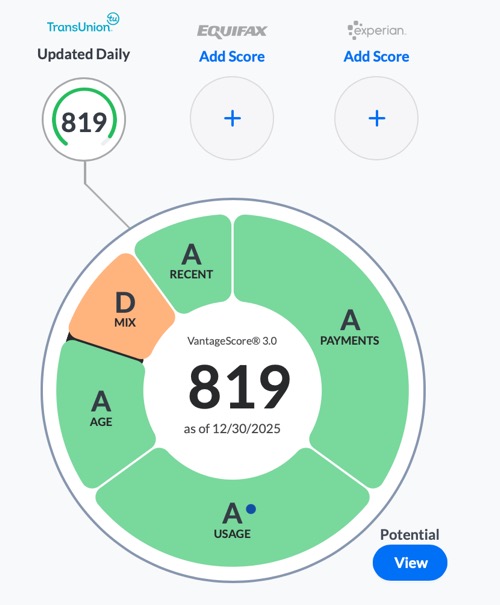

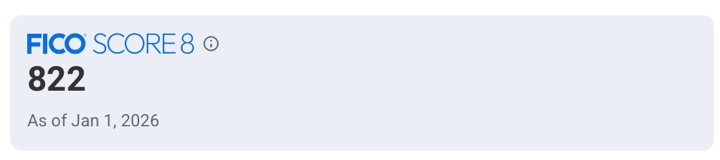

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)