New Gift Card deals, Earnify 25 cents/gallon gas offer. Amazon Black Friday 2024 is here. Is it Black Friday Week? Black Friday Month? Who knows anymore. Hopefully this curated post will help you find the good stuff. I also like to check this “Buy Again” tab for any steep discounts on the specific stuff that you already buy. There are also several refreshed promos for linking certain credit cards as payment methods and/or using their points. I recommend trying all the links again.

(Note: If you are reading this in an email/RSS reader, unfortunately I am not allowed to include any Amazon affiliate links in e-mails, so they have been removed. Please click here to view the links.)

Some deals require a Prime membership. New members can sign up for a 30-day free trial. Amazon Prime Student (student OR age 18-24) has a 6-month free trial and 50% off the regular price ($7.49/month). If you’ve already done the trial, you can simply buy a month of Prime for $14.99 ($6.99 with SNAP, EBT or Medicaid card).

Deals and Offers

- List of all current Black Friday deals (updated constantly).

- NEW: Buy $100 in Apple Gift cards, get $15 promo credit. Similar to the previously-mentioned Target and Best Buy deals on Apple gift cards.

- NEW: Gift Card Sale – Up to 20% Off. Examples include Roblox, Krispy Kreme, DoorDash, Google Play, Lyft, Instacart, Walgreens.

- NEW: Earn 25 cents/gallon of gas on your next 2 fill-ups with Earnify. After that, save 10¢ a gallon at BP, Amoco, and participating ampm stations when you link your Amazon and earnify™ accounts. Expires 12/2.

- NEW: WyzeCam OG Camera $10. I have several Wyze cams all around the exterior and interior of my house. Really good value to see what is going on around your house, although you will have to pay extra for cloud video storage now.

- Expired: Free $5 Amazon credit from Coca-Cola with short form. Supplies are limited.

- Don’t have the Prime Visa? Get a $200 instant Amazon gift card (limited-time offer).

- Already have the Prime Visa? Get 10% back on these Prime Card Bonus items.

- Amazon Device Deals (Echo, Blink, Eero, Ring, Kindle, Fire, etc).

- Apple Deals (Apple Watch, Airpods, Macbook, AirTags, etc).

- Samsung Deals (Galaxy Phones, Galaxy Tab, Galaxy Watch, etc).

- YETI Deals (YETI tumblers, bottles, coolers, etc)

- Sony Deals (headphones, earbuds, cameras)

- Playstation Deals (headphones, earbuds, cameras)

- Dyson Deals

- Apple iPad (10th Gen, 64 GB) – $279 (20% off)

Amazon-related Services

- Kindle Unlimited – 3 months for $1 trial. Usually $11.99 a month. Targeted.

- Amazon Music – 3 months free. Usually $10.99 a month. Targeted.

- Audible Premium Plus – $0.99/month for 3 months + $20 Audible credit. Includes 1 free credit per month, so that could be 4 free audiobooks. Targeted.

- Amazon Photos – $15 credit with first-time use.

Credit card linking bonuses (check again if targeted). Offers for simply adding a specific credit card type as Amazon payment method.

- Get $15 off when adding your eligible American Express Card to Amazon. Promo code 24AMEX15OFF.

- Get $15 off when adding your Discover® Card to Amazon. Promo code 24DISCOQ4.

Set as default payment method bonus (check again if targeted). Offers for simply making a specific credit card type your default payment method.

Shop with points (check again if targeted). Offers for using your rewards points to offset your Amazon purchase. If you haven’t linked your card, you may enroll your card and check back in after 24 hours.

- Get $10 off with Discover® rewards. Minimum spend $75.

- Get 15% off with Membership Rewards points. Maximum discount $15.

- Get $ off with American Express Reward Dollars.

- Get $ off with Chase Ultimate Rewards points.

- Get $ off with Capitol One Rewards points.

- Get $ off with US Bank Rewards points.

- Get $ off with Citi ThankYou points.

Stuff I Like

- Apple Watch SE (2nd Gen) [GPS + Cellular 40mm] . Now $219. See Apple Watch as Standalone Phone For Kids. Still working well with daily use, even with a $9 fun stretchy band.

- Dyson V11 Origin Cordless Vacuum. Expensive. Powerful. Useful. Daily driver.

- Amazon Eero mesh WiFi router system (3-pack). This is the older model now, but it’s also only $115 now and has the same coverage area size as the new model. Used reliably every day for years now.

- Amazon Eero 6+ mesh WiFi router system (3-pack) (newest model) . Supports WiFi 6 with faster speeds and bandwidth, $195.

- COSORI Air Fryer 5 Qt. Love this air fryer. We use it almost daily, just like a microwave, except it keeps things crispy instead of soggy. Easy to clean.

- Vitamix 5200 blender. Had it for many years. Kitchen staple, sometimes we use it a lot, sometimes rarely, but it’s always there ready and powerful.

- Takeya Patented Deluxe Cold Brew Coffee Maker. I like that I can store this thing sideways and it never leaks.

- KitchenAid Artisan Series 5 Quart Tilt Head Stand Mixer. 20 years of use on ours and counting.

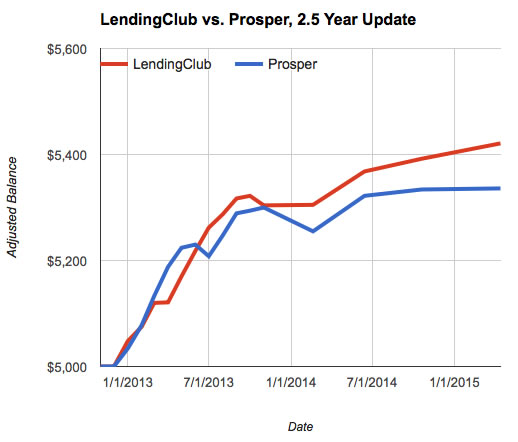

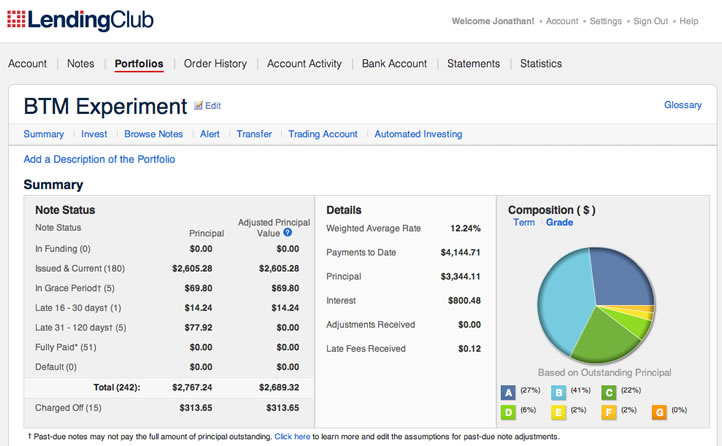

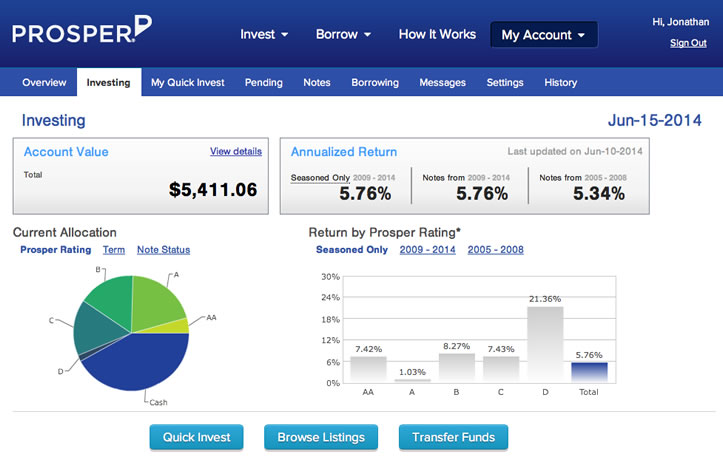

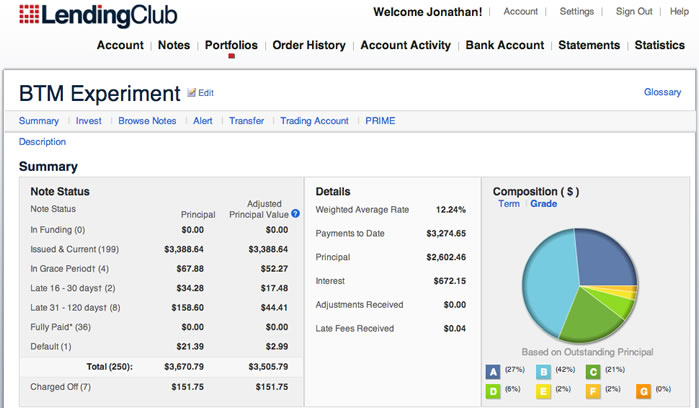

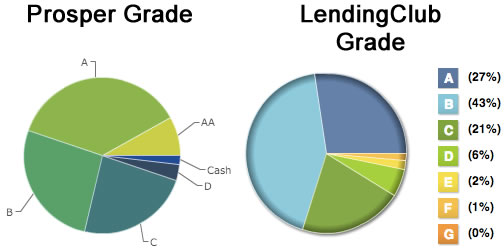

In November 2012, I invested $10,000 into person-to-person loans split evenly between

In November 2012, I invested $10,000 into person-to-person loans split evenly between

After posting the 1-year update (

After posting the 1-year update (

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)