😎 First made 20 years ago, last updated in 2026! Zero AI used! 😜

Thinking about moving your cash to a different bank account with a higher interest rate? Each month, I research the high interest rates available on cash. Big banks and corporates earn billions of dollars on your idle cash when it earns you nothing.

For example, you might have $10,000 in a savings account earning 3.00% APY and you want to know if it’s worth moving to one earning 4.00% APY. Use this handy calculator to find out how much more money you could earn by switching, which you then can weigh against the time and effort required.

My Money Blog Ultimate Rate Chaser Calculator

Notes

- This calculator is based on a rate-chasing breakeven time formula developed here a long, long, long time ago (2006!) which takes into account the “days of lost interest”, or the time in between transfers where the money is not earning interest in either account.

- The formula actually uses APR, not APY. APY takes into account compounding frequency. The overwhelming majority of online savings accounts compound interest daily. I also made a APY to APR calculator. Nowadays, I just assume daily compounding so that you can just input the APY instead of having to convert. A small minority of savings accounts do compound monthly, but most of those are the megabanks paying you 0.01% APY anyway.

- Usually, there can be between 0-3 days of lost interest when going from one bank to another. This depends on the policies of either bank and also which bank initiates the transfer. (It also may depend on if you straddle a weekend with the money earning no interest.) This value can significantly affect the break-even time when the difference is small.

- The 6-month value (182 days) isn’t simply 6 times the 1-month value (30 days), as the calculator takes into account the time needed first to “break-even”.

- Another factor to consider is how likely the current rate difference will persist. Interest rates on savings accounts can change at any time, whereas certificates offer a fixed rate over the guaranteed period.

Last updated 2/16/26.

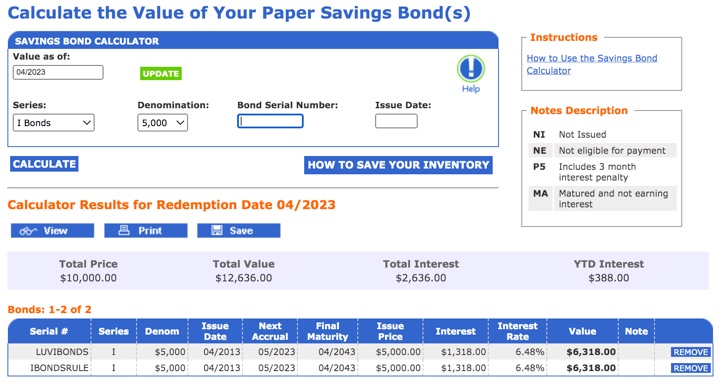

If you have accumulated some savings bonds but don’t really enjoy logging into TreasuryDirect.gov all the time, here are some alternative methods to tracking your balances over time. Each has its own strengths and weaknesses, and the unofficial ones are the results of motivated DIY investors. As an example, I will track a Savings I Bond purchased in April 2013 for $10,000.

If you have accumulated some savings bonds but don’t really enjoy logging into TreasuryDirect.gov all the time, here are some alternative methods to tracking your balances over time. Each has its own strengths and weaknesses, and the unofficial ones are the results of motivated DIY investors. As an example, I will track a Savings I Bond purchased in April 2013 for $10,000.

While updating my posts on

While updating my posts on

If you are an individual investor that usually buys bank certificates of deposit, right now you may want to compare against a US Treasury bond of similar maturity. Treasury bond rates are traded constantly, but this

If you are an individual investor that usually buys bank certificates of deposit, right now you may want to compare against a US Treasury bond of similar maturity. Treasury bond rates are traded constantly, but this

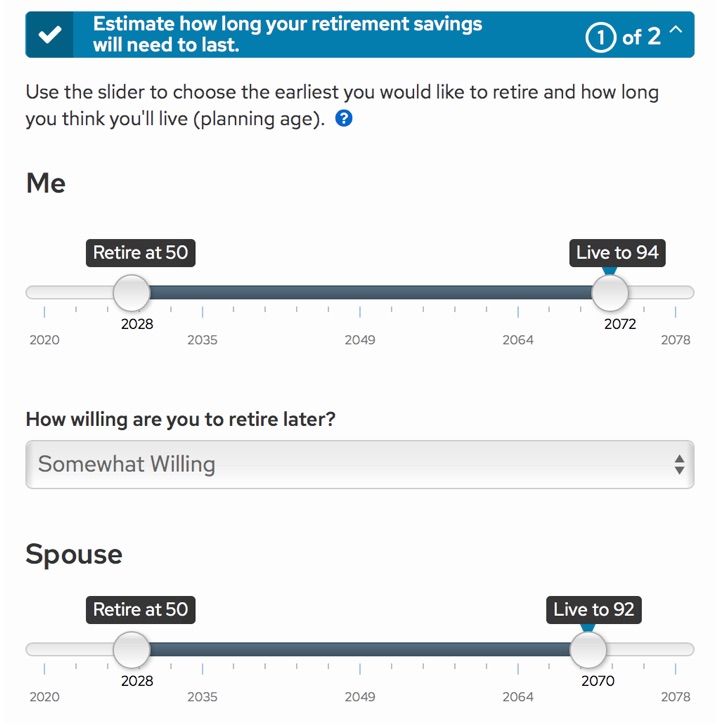

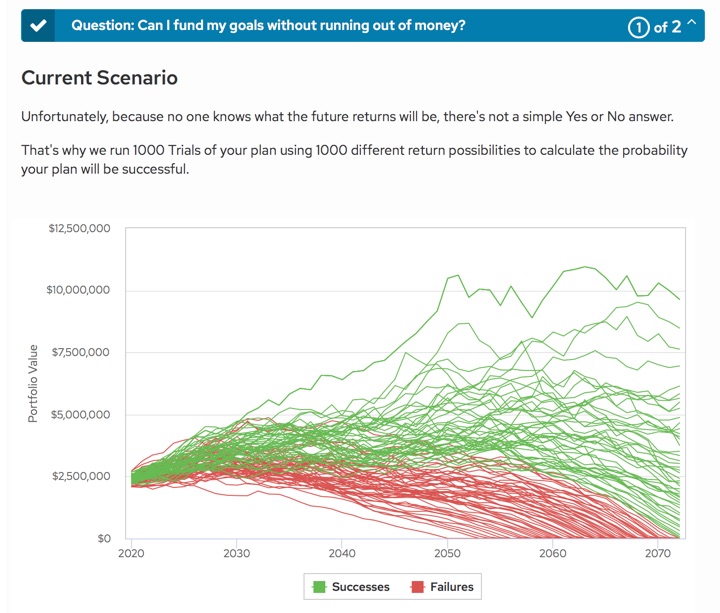

Schwab has rolled out a new digital financial planning tool called

Schwab has rolled out a new digital financial planning tool called

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)