Bank of America’s “Preferred Rewards” program officially switched over to the “BofA Rewards” program as of May 27, 2026, although most existing members will be grandfathered into their current tier for up to 11 more months or so. One of the list of program changes was the promised addition of “Subscription credits – Get up to $180 annually in credits for streaming services you use most”. Here’s what the fine print said:

BofA Rewards™ Subscription Credits. In order to be eligible for the subscription credit benefit, you must:

(1) Be enrolled in the BofA Rewards program’s Preferred Honors or Premier tiers.(2) Agree to the full terms of the subscription credit benefit from the subscription credit benefit page within BofA Rewards.

(3) Make payments directly to eligible merchants using your Bank of America debit card linked to a checking account that you designate via the subscription credit benefit page.

Preferred Honors tier members may receive statement credits up to $8 per month, and Premier tier members may receive up to $15 per month. Eligible merchants are subject to change without notice. Currently eligible merchants can be found on the subscription credit benefit page.

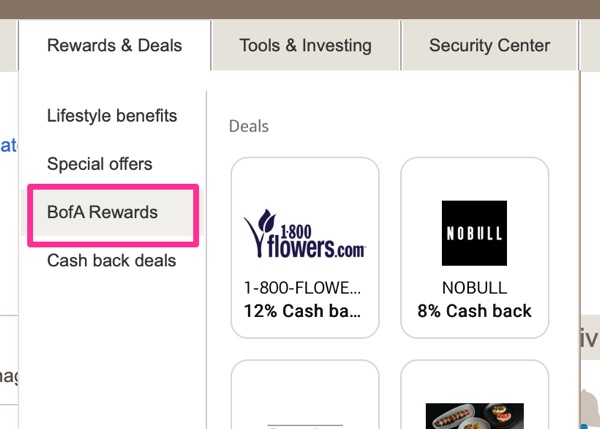

I could not find a public “subscription credit benefit page”, and it looks like it’s only visible for actual members. I am still on the new “Premier” tier, which is their highest current tier. I logged into my BofA account and navigated to the “Rewards & Deals” tab and then “BofA Rewards”.

After that, I scrolled down to “Feature Benefits” to the subscription benefit details. I can only assume that they are same for everyone, but this is what I have:

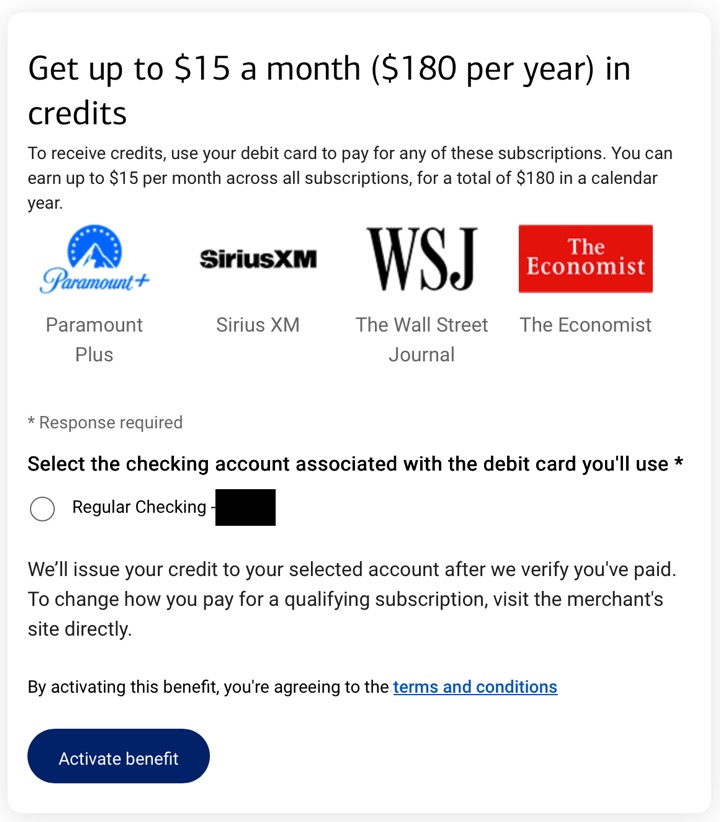

Here are the current merchants along with their regular monthly prices, as the credits can only be earned in monthly increments:

- Paramount+: $8.99/month for the ad-supported Essential tier and $13.99/month for the ad-free Premium tier (which includes Showtime).

- SiriusXM: $11.99/month for the App-Only All Access plan, while an Car+App All Access plan normally lists for $25.99/month.

- Wall Street Journal: Digital access is $11.25/week, but the first year is $8 every 4 weeks right now.

- The Economist: Digital access is $29 every 4 weeks.

I’m rather disappointed with the limited selection. Personally, I don’t pay for Paramount+ right now so I might get it for “free” with this offer, but I doubt I’ll use it very much. WSJ is probably the service I use the most but I already have access via alternative means, and it doesn’t even cover the entire cost anyway. I hope BofA changes up the options regularly. Netflix would have been nice.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)