Even though we as Americans like dining out a lot more than cooking at home, even if it costs more, we’re not totally crazy spenders. From Sherwood News:

We are keeping our cars for longer.

We are keeping our iPhones for longer.

Dang, looks like I have to keep the 2015 minivan around at least three more years in order to keep my frugal cred. (Minivans are classified as light trucks!)

When creating financial statements, there are “generally accepted accounting principles” (GAAP) so that all companies follow the same standardized set of rules. After reading 100+ books on personal finance, you could also create what I would call “generally accepted personal finance principles” (GAPFP?), as organized into a

When creating financial statements, there are “generally accepted accounting principles” (GAAP) so that all companies follow the same standardized set of rules. After reading 100+ books on personal finance, you could also create what I would call “generally accepted personal finance principles” (GAPFP?), as organized into a

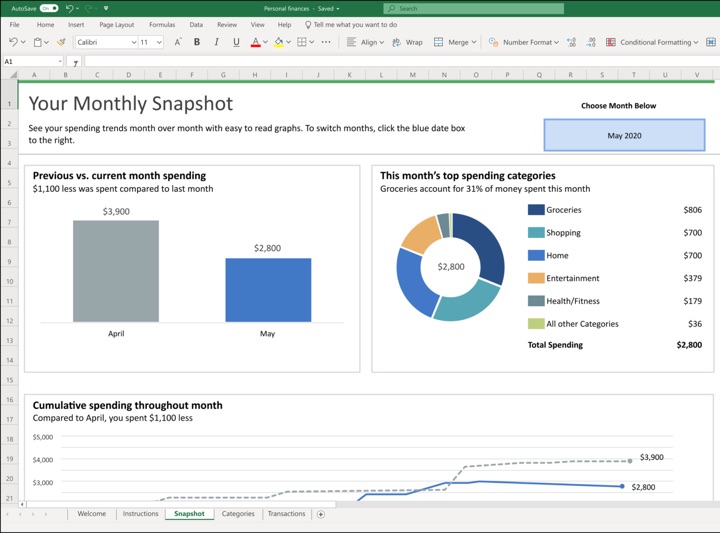

Thanks to generous assistance from a reader, I was able to spend some time poking around the

Thanks to generous assistance from a reader, I was able to spend some time poking around the

If there’s one topic that’s probably more sensitive than people talking about their money, it’s how they split their money with their partners. I am swayed by the method proposed by this post –

If there’s one topic that’s probably more sensitive than people talking about their money, it’s how they split their money with their partners. I am swayed by the method proposed by this post –  After finishing

After finishing  The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)