Updated. Happy New Year! 🎉 🥳 In terms of keeping my finances in order, what I’ve been finding most useful recently are credit monitoring alerts. The last time I applied for a credit card, I received multiple e-mails within minutes alerting me that someone had checked my credit report. I’m also told if a new account is added. This makes me feel more comfortable knowing that I’ll be alerted quickly if someone does try to steal my identity. The following third-party services listed below provide you a free credit score (of various algorithms) and/or free continuous credit monitoring from select credit bureaus.

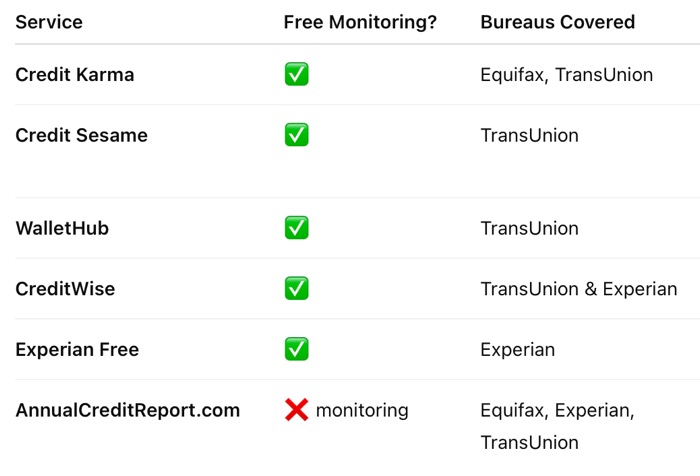

- Free credit score (VantageScore 3.0) from both Transunion and Equifax.

- Free credit monitoring from both Transunion and Equifax. Via e-mail alerts or app notification. Will let you know about things like a new credit check or a new account added.

- Limited identity theft monitoring. Credit Karma uses your email address to search and notify you if they are listed in public data breaches.

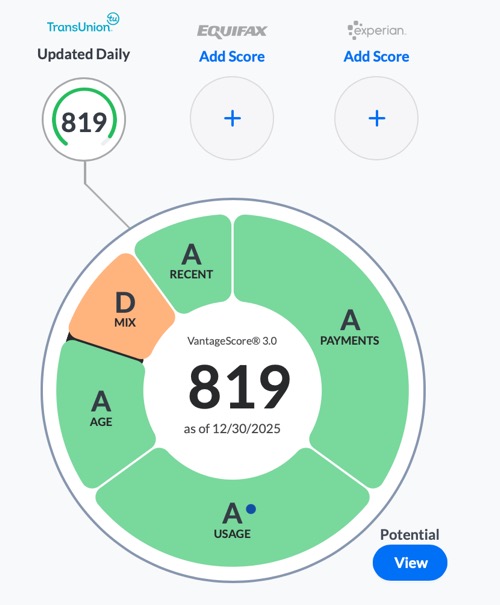

- Free credit score (VantageScore 3.0) from Transunion. Daily credit score updates and weekly credit report profile updates.

- Free credit monitoring from Transunion. Via e-mail alert. Will let you know about things like a new credit check or a new account added.

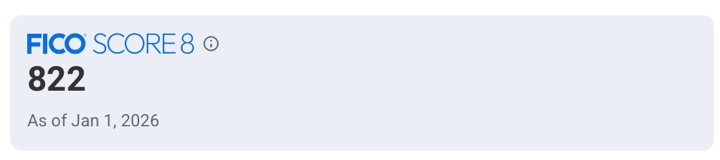

- Free credit score (FICO 8) from Experian. Daily credit score updates and daily credit report profile, refreshed upon login.

- Free credit monitoring from Experian. Free e-mail alerts.

- Warning that Experian will regularly try to upsell you to a paid membership tier. Simply click “No, keep my membership” to stay on the free tier. I’ve been on it for years.

- Improve your credit score by adding utility payments. Experian Boost is a free option that can potentially improve your Experian-based credit score by adding on-time utility and phone bill payments.

- Free credit score (VantageScore 3.0) from Transunion. Daily credit score updates and free daily full credit reports.

- Free credit monitoring from Transunion. Via e-mail alert. Will let you know about things like a new credit check or a new account added.

- Free credit score (FICO 8) from Transunion. You do not need to be a Capital One customer to sign up.

- Free credit monitoring from both Transunion and Experian.

None of the services above require a trial or credit card number to sign up for their free tiers. They may ask for the last 4 digits of your SSN for verification. These are all ad-supported (they will pitch you stuff) and usually have a paid upgrade option (but you can stay on the free tier forever).

The government requires the credit bureaus to provide you a free credit report at least once every 12 months (now actually weekly since the pandemic). However, the site will not provide you credit scores or pro-active alerts if anything changes on those reports.

Note that some of the scores above are not FICO scores because Fair Isaac might charge more money in licensing fees. If you really want a FICO number, nearly every major credit card issuer now includes a monthly FICO score with their cards: Chase, Citi, Bank of America, Discover, Barclaycard, and American Express.

Bottom line. Used in combination, I use the services above to keep track of changes to my credit reports across all three credit bureaus for free. None of them require my credit card number, and they quickly alert me to things like new accounts, new credit check inquiries, and high credit line usage. I just ignore the generic ads and upsells.

People are usually quite eager to share their stories of amazing wealth and riches. If you bought Apple in the early years or Bitcoin at $40, why not mention that at a party? Folks are usually much more quiet about their failures. But you can find such admissions thanks to the anonymous nature of social media. Reading these confessions can hopefully provide a clearer perspective of potential dangers.

People are usually quite eager to share their stories of amazing wealth and riches. If you bought Apple in the early years or Bitcoin at $40, why not mention that at a party? Folks are usually much more quiet about their failures. But you can find such admissions thanks to the anonymous nature of social media. Reading these confessions can hopefully provide a clearer perspective of potential dangers.

Mortgage rates have hit another all-time low, with some 30-year fixed rate mortgages below 3% and 15-year fixed below 2.5%. I know that many folks have already refinanced successfully, but these lower rates may offer even more homeowners the ability to lower their payments and/or pay off their home sooner. Importantly, Fannie Mae and Freddie Mac announced an additional 0.5% fee on refinances that was supposed to start on 9/1, but that was just

Mortgage rates have hit another all-time low, with some 30-year fixed rate mortgages below 3% and 15-year fixed below 2.5%. I know that many folks have already refinanced successfully, but these lower rates may offer even more homeowners the ability to lower their payments and/or pay off their home sooner. Importantly, Fannie Mae and Freddie Mac announced an additional 0.5% fee on refinances that was supposed to start on 9/1, but that was just

While not exactly a fun exercise, do you know where you’d turn for some extra cash in an extended emergency? Morningstar has

While not exactly a fun exercise, do you know where you’d turn for some extra cash in an extended emergency? Morningstar has

Apparently, my

Apparently, my

Fintech (financial technology) is supposed to make our lives better. You’ll hear how they want to nudge us to save more, invest better, spread risk, and lower costs. But if you look a little deeper, another thing many want to make easier is debt.

Fintech (financial technology) is supposed to make our lives better. You’ll hear how they want to nudge us to save more, invest better, spread risk, and lower costs. But if you look a little deeper, another thing many want to make easier is debt.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)