(Update: Here is an alternative version, which only requires a checking account and does not require direct deposit nor a savings account. Thanks to reader Sweepster.)

Back again, new expiration date 7/15/2026. Here’s another megabank bonus to pick up if you haven’t already. Chase Bank has a Total Checking + Savings account promotion offering up to $900 total for new customers that open both a checking and savings account with them along with additional specific requirements. This offer comes around regularly, but right now the bonus amount is higher than the standard amount. I recommend the e-mail option where you get an e-mail along with a unique 16-character coupon code. Otherwise, make sure you click on the correct online link on the $900 page to apply the proper code to your application. Current shown expiration is 7/16/2026, but it may end earlier.

Be sure to read all the requirements, including what is required to avoid the monthly fees for each account. Notably, you need direct deposit to the checking and you’ll need a $15,000 deposit for 90 days in the savings. You enter your e-mail address, and you will get a unique code for your online application. Some of the language suggests you should reside near a physical Chase branch, but the link lets you apply online and it should work from anywhere (you will know via instant approval). If you already have a Chase credit card, the application can be pre-filled.

Chase Total Checking $300 bonus details. Checking offer is not available to existing Chase checking customers, those with fiduciary accounts, or those whose accounts have been closed within 90 days or closed with a negative balance. You must:

- Open a new Chase Total Checking account, which is subject to approval;

- Have your direct deposit made to this account within 90 days of coupon enrollment. Your direct deposit needs to be an electronic deposit of your paycheck, pension or government benefits (such as Social Security) from your employer or the government.

- After you have completed all the above checking requirements, [Chase will] deposit the bonus in your new account within 15 days.

Avoid monthly service fees on Total Checking when you do at least one of the following each statement period. Otherwise a $12 Monthly Service Fee will apply.

- Have monthly direct deposits totaling $500 or more made to this account; OR

- Keep a minimum daily balance of $1,500 or more in your checking account; OR,

- Keep an average daily balance of $5,000 or more in any combination of qualifying Chase checking, savings and other balances.

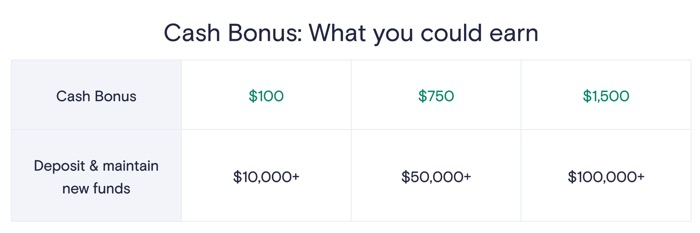

Chase Savings $200 bonus details. You must:

- Open a new Chase Savings account, which is subject to approval.

- Deposit a total of $15,000 or more in new money into the new savings account within 30 days of coupon enrollment;

- Maintain at least a $15,000 balance for 90 days from the date of coupon enrollment. The new money cannot be funds held by Chase or its affiliates.

- After you have completed all the above savings requirements, we’ll deposit the bonus in your new account within 15 days.

- 0.01% effective APY in the zip codes I checked.

Avoid monthly service fees on Chase Savings when you do at least one of the following each statement period. Otherwise a $5 Monthly Service Fee will apply.

- Keep a minimum daily balance of $300 or more in your savings account; OR,

- Have at least one repeating automatic transfer from your Chase checking account of $25 or more. One-time transfers do not qualify; OR,

- Chase College CheckingSM account linked to this account for Overdraft Protection, OR,

- Account owner who is an individual younger than 18, OR

- Have a linked Chase Premier Plus Checking, Chase Premier Platinum Checking, or Chase Private Client Checking account.

To receive the $400 extra bonus: You must open the checking and savings account at the same time and complete all requirements above for BOTH the checking bonus and savings bonus. After you have completed all requirements, [Chase] will deposit the remaining bonus due in your new account within 15 days.

I have read no reports of a “hard” credit check, and did not experience one myself on a previous offer years ago. Note that that to receive any of the above bonuses, the enrolled account must not be closed or restricted at the time of payout.

This is the highest bonus I’ve seen for this Chase combo. Earning $900 on $15,000 in 90 days is the equivalent of a 24% annualized return. The bonuses are considered interest and will be reported on IRS Form 1099-INT.

Bottom line. This is one of those bonuses that if you haven’t picked it up yet, it’s a pretty solid one. It’s a convenient megabank account with a large branch footprint, but also one that notably pays nearly zero interest. With a total opening deposit of $15,000 in new money, you can open both accounts and avoid both monthly fees. You’ll also need to change your direct deposit (any amount). Earning $900 on $15,000 in 90 days is the equivalent of a 24% annualized return.

New customer referral offer. If you don’t have a Marcus account yet, if you open with a

New customer referral offer. If you don’t have a Marcus account yet, if you open with a

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)