Limited-time Referral Bonus Boost: The Raisin referral bonus for new accounts has been hiked for a limited time, doubled on some tiers and now up to $200. The new tiers are below. At the $5,000 and $10,000 amounts, the bonus works out to 1% of the deposit for a minimum 90 day hold, which works out to a 4% annualized boost above the existing interest rates. ($50k tier = 1.2% APY annualized boost, $100k tiers = 0.8% annualized boost). Here is my referral link and my personal referral code is jonathanp31786. Thanks if you use it.

Full review:

Updated rates for July 2024. Raisin.com (formerly SaveBetter) is a financial marketplace that allows you to access high-interest certificates of deposit and savings accounts from multiple different banks and credit unions without having to open up a new account at each one. Every participation institution is either FDIC-insured or NCUA-insured. The participating banks, product terms, and interest rates change regularly. SaveBetter is now Raisin, to better match the same popular service that runs in Europe. Here are the top Raisin offers as of 5/1/2024:

High-Yield CDs

- 5.10% APY for 12-month CD. CDs are for locking in a rate. I don’t really consider anything less than a year term to be useful. Minimum opening deposit is $1.

No-Penalty CDs

- 5.10% APY for a 9-month No Penalty CD. Your rate will never go down, but there is also no early withdrawal penalty. Withdrawals may be made 30 days after opening.

Liquid Savings

- 5.27% APY Savings Account. Minimum opening deposit is $1. No limit on number of transactions.

Background on Raisin. Raisin is a marketplace for partner banks and credit unions looking to promote their deposit products. They offer liquid savings account, No-Penalty CDs, and High-Yield traditional CDs. Funds are held in a custodial account at the bank or credit union that is providing your selected savings product(s). The banks are all FDIC-insured and the credit unions are all NCUA-insured. Raisin does not charge any monthly maintenance fees. Raisin’s US operations are a subsidiary of Raisin GmbH, a German financial company that also offers high-interest deposit products across Europe.

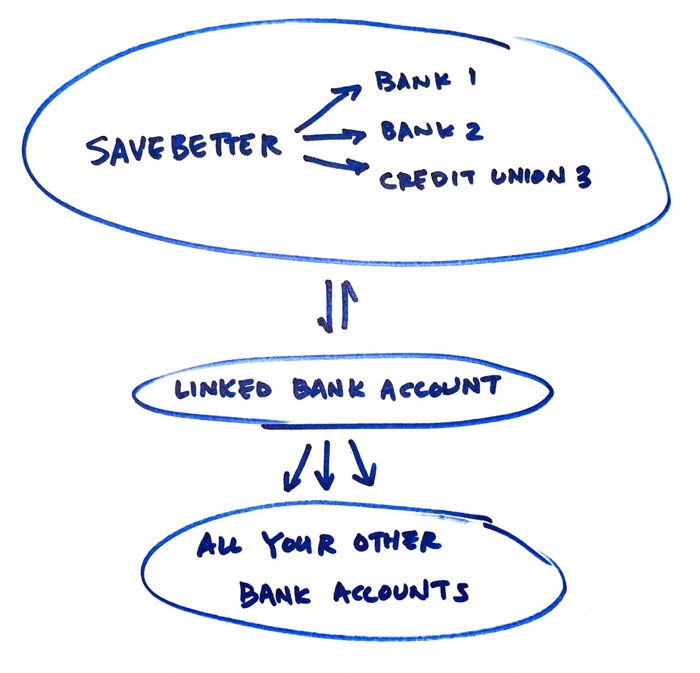

The benefit for the consumer is that you can easily access promotional rates at a new bank or credit union without having to open yet another new account (and endure credit checks, identify verification hurdles, join partner organizations, leave funds in share savings accounts, etc). This makes it easier to chase higher savings accounts and CD rates. You must link a single external bank account and make all your deposits and withdrawals electronically through that linked account. You can only have one external bank account linked at a time, so choose carefully.

A drawback is that you do not get direct access to your Raisin sub-accounts via routing number and account number. You must go through the Raisin site to open accounts, make deposits, and make withdrawals. Your single linked external bank is your only access to Raisin, so in a way I mentally name it also as my “Raisin bank account”. Here is a simple illustration I made that helps me visualize this setup:

Here are some more details from the Raisin site:

5. What is a custodial account and how does it work?

Custodial accounts are involved in how Raisin directs the money transfers from customers to the banks and credit unions holding their savings. When a customer makes a deposit through their Raisin account into a savings product offered by a given financial institution, the funds move from the customer’s external bank account (also referred to as the reference account) to an omnibus custodial account held by Lewis and Clark Bank (functioning in the role as a custodian bank) at the financial institution offering the savings product.6. How does pass-through deposit insurance work?

Although Raisin customers’ deposits are pooled in omnibus accounts, there is no impact on the eligible deposit insurance coverage you receive from the financial institution holding your savings. This is because the government entities providing federal deposit insurance — the FDIC for banks and NCUA for credit unions — permit pass-through coverage. So your money that’s pooled in a custodial account still has the coverage it would have were it held in an individual account in your name.

I suspect this setup is a lower cost structure for the banks as well, which in turn allows higher interest rates. After learning about omnibus accounts, I noticed that other places like Fidelity Investments also use them in their cash sweep accounts as temporary holding accounts. Search for “omnibus” in your terms and conditions. This is also similar to how “brokered CDs” are usually managed when you buy them through a broker like Vanguard and Fidelity – the funds are pooled together at the issuing bank and don’t include individual account numbers. Same with the FDIC-insured accounts inside many 529 plans.

Referral bonus ($5,000+ deposit required). The minimum deposit for both their savings and CDs are usually as low as $1 (each product has different terms). However, if you are new to Raisin and plan to deposit at least $5,000, they do have a referral program if you open via a referral link and enter my personal referral code jonathanp31786. You must deposit $5,000 for 90 days to earn $25, and then additional $5 for every subsequent $5,000 deposit past that, up to a max of $125 bonus ($105,000 total deposit). Here’s the fine print:

Making $125 has never been so easy or rewarding. Simply enter in the code you received from your friend or family member when you sign up for an account with Raisin. Once you fund your account and maintain an initial balance of $5,000 or more for 90 days, you will earn a minimum bonus of $25 and a maximum bonus of $125 depending on the account balance you maintained after 90 days. The bonus will be paid out within 30 days of qualification. Funds will be deposited into your external bank account linked to Raisin.

The referral bonus has gone up for a limited-time. Please see the top of the post for the current tiers.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Are there people really going through those 3rd-person middlemen apps?

I mean, even if they’re FDIC, it’s hard to drop $$ on a fresh fintech platform with many bad reviews (see reddit)… I pass

So if five people opened an “account” for $5,000 each with Sallie Mae through this save better site, essentially Sallie Mae gets $25,000 but doesn’t know our details? Save Better sends the tax forms at the end of the year under their logo?

So we rely on Save Better actually passing the money through to the bank with no way to confirm that Sallie Mae got the funds?

Good review of how it works.

https://youtu.be/4_sMB3z5zz0

You can buy brokerage CDs via the big brokerage companies, like Charles Schwab, Merrill Edge, Fidelity, Vanguard, right? What’s the advantage of signing up with Savebetter.app?

I agree I just found out about fidelitys ability to buy cds, have been getting a bunch at 5,3% the only major difference is there it’s $1k minimum.

Brokered CDs can be a good option, but you have to understand the differences. For example, the only 12-month CDs at 5.30% from Fidelity that I see right now are callable, which means that the bank can call the CD back if rates drop in the future. Of course, the bank will only do so if it is profitable for them and not helpful to you. The early withdrawal rules are also more vague. Unlike with traditional bank CDs, you may be able to sell your CD if you want to withdraw early, but you may not, and you don’t know what the penalty will be if you do.

Your money at Savebetter will be mixed with everyone else’s money into an “Omnibus” account. You won’t have an account number at the Product Bank. If Savebetter ceases to function, you have no record of your money or account. Good luck getting your money back. On another note, their top product bank (Western Alliance) has lost half it’s value in the last week. Savebetter was risky before the SVB collapse. Now…I wouldn’t touch this with a 10 foot pole. Certainly not to get an extra half percent on a CD.

Seems similar to (although on Savings Accounts) to: https://maxmyinterest.com/

Seems risky especially during these times of bank failures. I would give this financial scheme some time to make sure it weathers the storm.

With ongoing non-giant bank crisis, it’s not a time to give yourself headaches with a little bit more interest…

For new depositors, banking with Savebetter is not as simple as it may appear.

There are a bunch of traps for newbies to fall into. You might want to call

Customer Service. At Savebetter, that sounds easy. But try it and see.

And even if you succeed in contacting them, they may not always be able to

help you right away. If you need to use a new or different service

bank to add or withdraw funds, you will need to wait 60 days after account

opening and only then will they be able to help you do that. See, it is not all

Easy Peazie!

This is just unnecessary risk. Look for brokered CDs at your BROKERAGE, not some fintech bullshit.

You can do similar thing at Schwab, find and open CDs through Schwab which are then at other banks. Would trust Schwab more then raisin(or grape)

Raisin? Why would they change the name to Raisin? LOL

Raisin is apparently a relatively well-known brand in Europe. They’ve been doing this thing over there for a while before coming over to the US.

Used the referral but never received the bonus. Emailed them a few times without any response. I think I am done with those Fintechs.

Which bank is Raisin involved with for the 5.4% no penalty CD? In other words, if I can just go to the origin bank directly for this offer instead of joining Raisin if possible…

Seems risky, especially in considering the recent bank tragedies. I’d give this financial plan some time to see if it can withstand the crisis.

-John Cyruz Masacayan

Note that the 16 month no penalty CD at 5.60% is offered by Western Alliance Bank which is one of the banks that was affected by the 2023 banking crisis. Seems like there is a high chance of a bank failure, I personally wouldn’t risk trying to get my money back through the FDIC insurance scheme without an account number.

Does Empower Personal Cash connect to Raisin?

Empower Personal Cash doesn’t connect to Raisin; however within Raisin you can input your Empower Personal Cash program account number and routing number (both can be found on your monthly statement) to send transfers between the two programs. Raisin only supports having one account linked at a time, though.

Raisin is also not available on Empower Personal Dashboard, so you’d need to manually update the balances there periodically if you use it to track your net worth. (In most cases with Raisin, interest accrues daily but is paid monthly.)

Can you transfer funds from one bank to another within Raisin?

Example: I have funds in Bank A with Raisin. I noticed another financial insitution (Bank B) within Raisin that offers a higher APY. Can you transfer funds from Bank A to Bank B within Raisin or do first have to transfer funds from/to the external account to move funds from from Bank A to Bank B?

Hi there. I have Raisin, and for now, it’s the latter. I heard (can’t remember where) that Raisin is working on the capability to transfer directly from bank to bank without having to withdraw the money first. (And once you have a Raisin account I think it’s super easy to withdraw and then re-deposit because your account is already linked.) If you sign up, make sure you enter a referral code to get a bonus. Feel free to use mine: jeffh029272

You have to transfer to an external bank first. A HYSA account with fast ACH is a good choice, such as SoFi. The top banks fluctuate somewhat; you can use yieldalarm.com to get alerts if your bank’s rate drops. Unfortunately you won’t earn interest while the funds are in transit so it’s sometimes not worth it to transfer if the % change is very small.

Than you for the reply and the yieldalarm tip.

Just an update on this – Raisin has a cash account now which is typically a 1-business-day transfer each way within the platform.

Use your referal code, Jon. Do I need to keep lonely there to avoid fee after 3 months? I open an nexbank high yield savings account

Thanks! No, there is no minimum, you can take it all out if you want.