In November 2012, I invested $10,000 into person-to-person loans split evenly between Prosper Lending and Lending Club, looking for high returns from a new asset class. After diligently reinvesting my earned interest into new loans, I stopped my after one year (see previous updates here) and started just collecting the interest and waiting see how my final numbers would turn out at the end of the 3-year terms.

In November 2012, I invested $10,000 into person-to-person loans split evenly between Prosper Lending and Lending Club, looking for high returns from a new asset class. After diligently reinvesting my earned interest into new loans, I stopped my after one year (see previous updates here) and started just collecting the interest and waiting see how my final numbers would turn out at the end of the 3-year terms.

It is now about a week shy of the two year anniversary of this experiment, so here’s another quick update.

$5,000 LendingClub Portfolio. As of October 20, 2014, the LendingClub portfolio has 157 current and active loans. 71 loans were paid off early and 21 have been charged-off ($314 in principal). 3 loans are between 1-30 days late. 5 loans are between 31-120 days late, which I will assume to be unrecoverable. $3,515 in uninvested cash from early payments and interest. Total adjusted balance is $5,392. LendingClub reports my adjusted net annualized return as 5.27%. Here is a screenshot of my account.

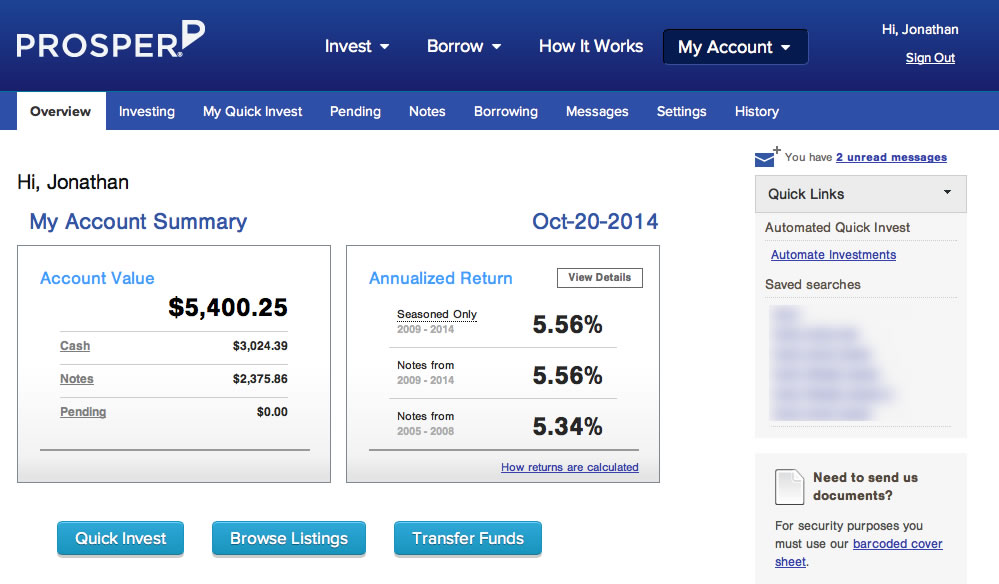

$5,000 Prosper Portfolio. My Prosper portfolio now has 142 current and active loans, 85 loans paid off early, 31 charged-off. 6 loans are between 1-30 days late. 6 are over 30 days late, which to be conservative I am also going to write off completely (~$66). $3,024 in uninvested cash (early payments and interest). Total adjusted balance is $5,334. Prosper reports my net annualized return as 5.56%. Here is a screenshot of my account.

Recap and Thoughts

- P2P lending is legit. LendingClub is preparing for an IPO on the NYSE. Institutional investors are buying a significant portion of LendingClub and Prosper loans. This WSJ article says 66% of Prosper loans in 2014 have been sold to institutional investors. What started out as the Wild West of unsecured loans is now accepted by Wall Street. This would suggest that reliable positive returns for investors are more likely, but also that chances for outsized returns will be diminished.

- If you continually reinvest your interest, the return numbers you see will be higher than your actual long-term returns. Due to how they are calculated, your reported return will deteriorate as your loans age and more borrowers default. After two years, Prosper reports my annualized return as 5.56%. 4 months ago, it was 5.76%. 8 months ago, it was 7.55%. LendingClub reports my annualized return after 2 years as 5.27%. 4 months ago, it was 5.94%. This doesn’t mean you shouldn’t invest and your returns may better than mine, but be aware of this pattern if most of your loans are new.

- If I were to invest all over again… First, I would do it within an IRA to avoid tax headaches. I would also buy at least 100 loans x $25, which also happens to be the $2,500 minimum for free automated investments at LendingClub (no minimum at Prosper). Picking loans can be fun for some but I got bored after a while.

- LendingClub vs. Prosper relative performance. I tried my best to invest at both websites with the same criteria and overall risk preference. Right now, LendingClub is ahead by a bit. I wouldn’t put too much importance on the absolute numbers as I stopped reinvesting into new loans (at both sites) after the first year. Here’s an updated chart tracking the LendingClub and Prosper adjusted balances separately over these past two years:

The Best Credit Card Bonus Offers – July 2024

The Best Credit Card Bonus Offers – July 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - July 2024

Best Interest Rates on Cash - July 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

How do you invest in Prosper or LC with an IRA? I love that idea, but not sure how to go about doing it.

For Lending Club, if you click the investing link, you can’t miss it.

Why are you keeping so much uninvested cash there? Why not withdraw it and put it in mutual funds or re-invest in new loans?

I forgot. I meant to move it into another “experimental” account that I’m trying out, but ended up getting the funds from elsewhere.

It is a bit misleading to say that your return will go down over time with your stated % of decline over the last year. To get the real return over time you will need to remove your uninvested cash, as that money earns 0% and quickly reduce the total return on your loan portfolio, especially when some of the loans are paid earlier. In fact I would bet it is by far the reason for the big drop in you return. Yes, the older your portfolio the worse your total return will be as you will lose more loans but it nothing like the numbers you quoted.

Actually, the return calculations all ignore uninvested cash, so that is not the reason why the returns drop over time as the loans age. You can view the specific formulas on the respective websites.

I stand corrected… Since we cannot see the loans, I was wondering how close lending club is to their projection of % of loses in a portfolio… I manage a portfolio purchasing mostly D, C and E… More Ds then Cs and more Cs than Es… My interest has changed over time but I am not seeing the kind of decline that you experienced… Of course the drop from day one to now was about 40% of interest returned… But it is still tracking to their projections…

Thanks,

Gideon

Jonathan, can you comment more on how you would do this inside of an IRA? For example, if we already have a Roth IRA, would this count towards the contribution limit, or is it completely separate? Are there similar restrictions on contribution?

Opening an IRA at Prosper or LendingClub is the pretty much the same as opening an IRA at any other brokerage. Either you make a fresh cash contribution for the year (yes it counts toward your annual limit) and then use that money to buy new borrower notes, or you roll over an existing IRA and the old securities get sold to buy these unsecured notes.

Jonathan, thanks for sharing your data. Those returns are really not very good given the lack of liquidity, but I suppose the investments have low correlation to other investments so there is some value as part of a diversified portfolio.

I have invested in lendingclub for about 3 years as well and my returns are about 8.5% which I think is reasonable given I don’t invest the lowest quality loans. I have slowed my reinvestment by steadily increasing the cash allocation of my portfolio so hopefully my returns don’t suffer too much, but I’d be happy with anything over 7.5%.

Bob

This is a great post and a very interesting “experiment”. I have to admit I have been contemplating the idea of lending money on either one of these companies but the potential risk of not getting my money back would stop me. From reading your post I see this is very legit and obviously you are getting a lot more return on investment than simply having your money sitting in a bank account. I have to many questions from, how long do people take to pay you back to whats the exact default risk, etc. But I suppose I can go on the websites and do some research on that. Thanks for sharing!

Are you going to participate in the Lending Club IPO for investors?

I was wondering about the IRA initial investment of 5K. I opened an account with Prosper at the beginning of the month with $500.00. I plan to invest $200.00 every other week. So, by next April, I will have $5000.00. Can I use this money already contributed to my account as the initial deposit to open the Roth IRA with them? Or does it have to by an additional 5K to open the IRA?

I do not believe they will let you fund with existing notes from a taxable account. I think you need $5,000 in cash sitting separately to fund an IRA. I would contact Prosper directly to be sure.

Im steadily adding anywhere from $500-$1000 a month to my account to invest. My goal is to keep adding every month and every year for several years. Do you think it would be possible to one day be living off solely from the interest I earn every month? Just reinvesting and taking out what I need. Im talking 15-20 years from now. I am 27 by the way right now.

Rafael: This is certainly possible, but I would caution against this. The money you wish you retire on should be diversified. Although prosper allows you to choose your investments, I would argue that the class of all your investments is too similar to represent a real diversification. I would keep Prosper/Lending Club as part of your total portfolio, but put a more significant portion into more traditional investments.