Businessweek has an article discussing the difficulties when trying to make a retirement nest egg last for the rest of your life. Most people just worry about the average returns of their investments. But another important concern during the withdrawal phase is sequence of returns risk.

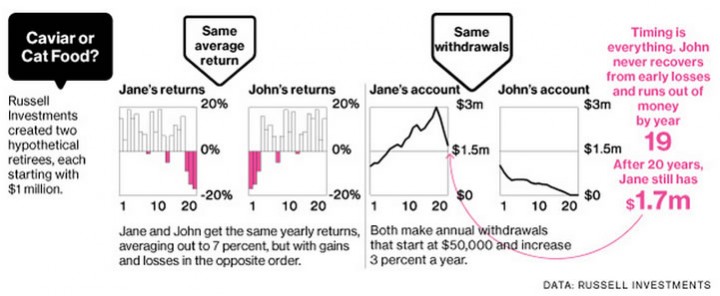

Two retirees can start with the same initial portfolio balance and experience the same average return, but if one experiences highly negative returns in the first few years of withdrawals they can end up with very different outcomes. Instead of explaining this concept with a list of numbers, here is a graphical version from the BW article. Both Jane and John start with $1 million, experience 7% average returns, and take out $50,000 a year with a 3% increase each year for inflation.

Jane ends up 20 years later with $700,00 more than she started, and John is flat broke. Although the sequence of returns shown is a bit extreme, they are simply mirrored and it is still entirely possible.

Some people take this to mean that you shouldn’t retire when the market has been on a good bull run, but I think the point is that you simply don’t know what order your future returns will be. The bull run could keep on going and create a bubble, and then pop many years later. Or something like a declaration of war could crush the market even further even if things have already been bad for a while.

Briefly, a couple of options that can help alleviate this sequence of returns risk are a dynamic withdrawal strategy that continually adjusts to actual returns (no set number every year), and also annuitizing part of your portfolio using a single-premium immediate annuity. Finally, don’t forget the traditional advice of holding a sizable chunk of quality bonds in your portfolio.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I think the lesson here is to have a sizable cash or cash equivalent (CDs, money market, G-Fund in the TSP, etc.) fund saved up before you pull the trigger and stop/reduce your trading time for money. If you have a year of expenses in cash and an additional 2-4 years of expenses in cash equivalents, you can ride out any bear markets that you encounter early in your withdrawal period. Then you don’t have to worry about timing your retirement with the market and you can get out whenever you’re ready!

Totally agree. The key is to either de-risk your portfolio (which means saving more) or hold a cushion in bonds or cash that allows you to not sell your risky assets for x (maybe 5) years in a downturn. That way you consume your cushion first rather than spending out of your entire portfolio, which would mitigate a lot of this problem.

yup!

people forget the good old adage about too many eggs in one basket.

It’s beyond me why an overwhelming majority of your nest egg would be in 1 basket either.

Greed is not a good reason to take risque risks

Jonathan,

This is why I invest in dividend paying companies. The dividend checks are always positive, they are much more stable than capital gains, they tend to rise faster than the rate of inflation, and the amount and timing is relatively certain. I do not have to worry about selling off portions of my nest egg during protracted bear markets, and watch my nest egg dwindle in horror.

Best Regards,

Dividend Growth Investor

Thats all well and good, but you need to have a much larger retirement portfolio saved up in order to live off just the dividends and not touch the principle. A good goal to shoot for, but perhaps unrealistic for everyone.

Hi Kevin,

What you are saying is simply not true.

I have constructed a well diversified dividend portfolio with over 40 individual components, representative of many sectors, and average yield of say 3.50%. You do not need more money to use dividend investing. The beauty of DGI is that I can create my own portfolios and keep my expenses to the minimum. I also pay much less per year than what the lowest cost Vanguard fund pays, and have a much lower turnover rate.

Also, my goal is to succeed and hit my goals, not the goals of “everyone”.

I agree with Dividend Growth Investor. You can collect about 5% from dividends and covered calls. And you will never have to touch the principle. I still see that 1 million as my target for retirement. And the principle will continue to double every 7 years (historical average). Which means my children will never have to work. Maybe my calculations are incorrect?