Observer has an interesting profile of respected investor Howard Marks, excerpted from the book The Great Minds of Investing (found via Abnormal Returns).

Observer has an interesting profile of respected investor Howard Marks, excerpted from the book The Great Minds of Investing (found via Abnormal Returns).

I enjoy the writings of Howard Marks because his observations are logical and rational, and he doesn’t mind putting out stuff that is boring and hard to do. It is much more popular to write about exciting things that are easy to do like “sell all your bonds!” or “buy oil stocks now!”. This quote from the profile is a good example. (Bolding is mine.)

“You can’t control the environment,” Mr. Marks adds. So the key is to recognize how it’s changing, accept it, and respond as wisely as possible. “The screwiest thing you can do is to think you’re a Master of the Universe. We’re all just little cogs, and the universe will go on without us. We have to fit into it and adapt to it.” For example, at the time of our interview in late 2014, he sees scant investment opportunity and excessive complacency: “What bigger mistake could there be than to think you can safely get high returns in a low-return world?” Investors should adjust by assuming less risk and lowering their expectations. He cites a favorite quote from Peter Bernstein: “The market’s not a very accommodating machine; it won’t provide high returns just because you need them.”

Assume less risk. Lower your expectations. I’ve been reading a lot of Dr. Seuss recently, and I think he would say “you may yawn and boo, but that is what you should do.”

For some reason, this book is out-of-stock at Amazon, unavailable at my library, and third-party copies are $70?! I believe this is because it contains high-quality photographs of the people profiled. Not to worry, Oaktree Capital has all of Marks’ famous memos online for free, or you can read a distillation of them in his book The Most Important Thing Illuminated (my review).

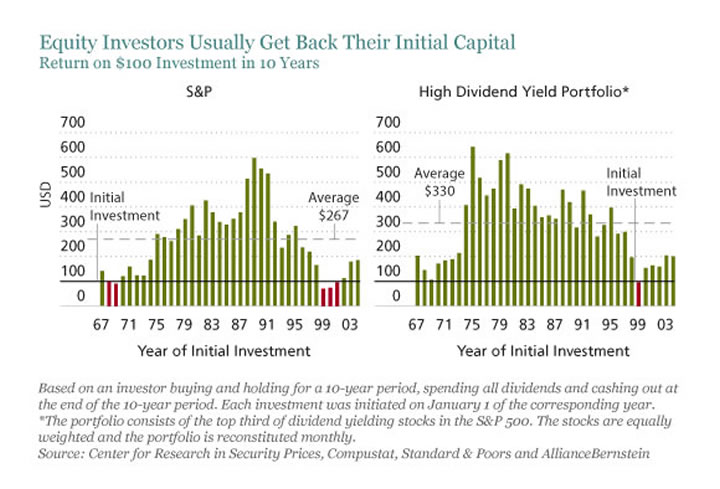

The following is a chart that I usually like to pull out during a crisis when people are scared of investing in the stock market, but since I just found a nicely updated version of it, I had to share. It is taken from Jeremy Siegel’s book

The following is a chart that I usually like to pull out during a crisis when people are scared of investing in the stock market, but since I just found a nicely updated version of it, I had to share. It is taken from Jeremy Siegel’s book

I just finished reading

I just finished reading

The Best Credit Card Bonus Offers – May 2024

The Best Credit Card Bonus Offers – May 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - May 2024

Best Interest Rates on Cash - May 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)