In a recent post on the NY Times Bucks blog, portfolio manager and author Richard Ferri shared his own personal portfolio. As a proponent of low-cost, passive investing, it was not surprising to see mostly index funds in his portfolio, but it was interesting to see that his overall asset allocation is 80% stocks and 20% bonds. He is quick to note that he does have a pension and defined-benefit plans which balance out his overall financial picture. Wouldn’t you like to know what all those financial advisors out there actually own?

Asset Allocation

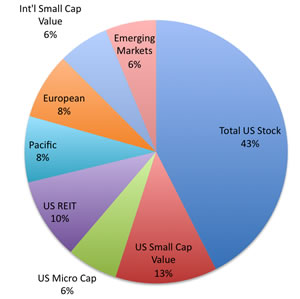

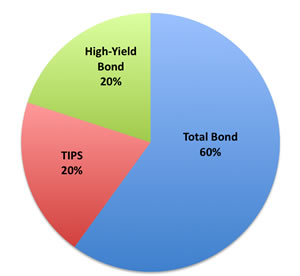

Here is his asset allocation broken down into stocks and bonds separately using pretty pie charts:

Stocks

Bonds

Here’s the overall 80/20 breakdown with ticker symbols (based on this Bogleheads post):

34% Vanguard Total Stock Market ETF (VTI)

10% S&P SmallCap 600 Value Index Fund (IJS)

5% Ultra-Small Company Market (BRSIX)

8% Vanguard REIT ETF (VNQ)

6.5% Vanguard Pacific ETF (VPL)

6.5% Vanguard European ETF (VGK)

5% DFA International Small Cap Value

5% DFA Emerging Markets Core

—- [alternative: Vanguard Emerging Markets ETF (VWO)]

12% Vanguard Total Bond Market Index Fund Investor Shares (VBMFX)

4% Vanguard Inflation-Protected Securities Fund Investor Shares (VIPSX)

4% Vanguard High-Yield Corporate Fund Investor Shares (VWEHX)

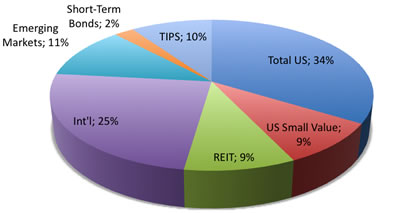

Reading his book All About Asset Allocation was very helpful in creating my own portfolio. (Also see Model Portfolio #3 taken from that book.) I haven’t been updating my own own portfolio asset allocation as diligently as I should, although I have been keeping track of it. Here’s the last snapshot I took:

I’ve had some asset allocation drift for sure, although I have been countering this by rebalancing with new funds. I really need an update…

Emergency Funds

It’s also interesting to note that he keeps an emergency fund of two years’ living expenses, and that he uses the Vanguard Short-Term Bond (BSV) with a current SEC yield of 1.08%. Very simple and almost no-maintenance.

I prefer using a mix of high interest savings accounts and longer-term CDs/rewards-type checking accounts. I figure that index fund investors get so excited by saving 10 basis points (0.10%) on mutual fund, but with a bit of work you could beat a short-term bond fund by 100 basis points (1%) with what I would call less risk.

Bond funds still have risk to principal, meaning you may have to sell for less than you bought in for, while FDIC-insured bank accounts do not. Money market funds are currently averaging less than 0.10% yield.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Looking fwd to your portfolio update and new funds in your portfolio

Thank you for continuing to provide good articles. I rarely comment, but was excited to see this manager’s allocation.

My wife and I have a similar system for investments and emergency fund. For simplicity, we use US Total Market (45%), International (30%), Small Cap (15%), Emerging Markets (10%). We are early/mid 20s and have a 3 months emergency fund; 1 month expenses in a savings account and 2 months in a bond ETF.

As always, thanks for the post. I was encouraged to see that we are headed in the right direction!

So, how’s it performing over the last 1, 5, 10 years?

Two year emergency fund?! WOW!

Jonathan – what vehicle do you use to add TIPs to your portfolio? Do you buy the TIP itself, use the Vanguard Fund referenced above, or hold an ETF (e.g., iShares “TIP”)?

I would like to have more inflation protection in my portfolio and am investigating the best options for me.

Thanks for this post and, as always, thanks for a great blog.

For a simple, yet plausible example of an asset allocation, look at the Google spreadsheet I put together. (It’s the website link above)

I’ve used a much more complex allocation for a while, and I’m coming to realize that it’s more cumbersome to rebalance and compute returns than it really needs to be. I’m leaning towards making this simple example my reality (though I’d probably split the bonds 50/50 with Vanguard’s TIPS fund.)

Things to notice:

+ The “spread” from best-to-worst years changes based on the asset allocation

+ In all these scenarios the rebalanced return is higher than the non-rebalanced return (See “Stock/Bond Actual History” tab)

— Steve

Thanks Mr. Ferri.

I’ve seen his portfolio about 4-5 years ago on a morningstar thread and it hasn’t changed much. That says something to staying the course with an allocation you see fit.

Still, never understood his VPL VGK combo. To keep things simple, a holding of VEA would suffice IMO. VEAs past performance appears to split down the middle of VPL and VGK, which one would think it should. Would love to hear his opinion on that.

Of course US economy still is the main. But well diversified portfolio should not depend to much on one economy. Isn’t 72% (in stock segment) of portfolio in US too much?

Rick uses Bridgeway Ultra Small Company Market fund (BRSIX) for his examples in the book. See the chapter called “Building your Portfolio.

One of the biggest mistakes investors make when considering an investment advisor is to look only at advisory fees and not at the portfolio recommended by the advisor and what the net historical and expected returns are. From your gross returns you subtract fund expenses, advisor expenses, and taxes. A lower fee advisor isn’t actually lower fee if they have delivered lower net of all cost returns.

The portfolio listed above is a great example of this. The firm charges a relatively low fee (the average fee on a $1M portfolio for the largest 200 firms with access to DFA funds is 0.75%), but the net results reveal a much higher cost associated with this philosophy.

Lets go back to 1990 so we can use emerging markets in our portfolio simuations and compare the returns of this index portfolio to a basic “DFA Balanced Equity portfolio”. The DFA allocation will simply serve as the average of all advisors who charge higher fees.

The portfolio listed above will be modeled using 60% DFA US Core 1 Index(the same size and value exposure as the Total Stock, Bridgeway, and S&P 600 Value indexes), 10% Wilshire Real Estate Index, 4.5% each in MSCI Europe ex. UK, MSCI UK, MSCI Japan, and MSCI Asia Pacific ex. Japan, 6% in DFA Int’l Small Value Index, 3% in Fama/French Emerging Markets Index, 1.5% each in Fama/French Emerging Markets Small Cap and Value Indexes (to approximate the DFA Emerging Core Equity Fund).

The DFA balanced portfolio will be 20% S&P 500, 20% DFA Large Value, 20% DFA Targeted Value, 10% REIT, 10% FF International Value, 5% DFA Int’l Small Cap Index, 5% DFA Int’l Small Value Index, 3% Fama/French Emerging Markets, 3% Fama/French Emerging Markets Small Cap Index, 4% Fama/French Emerging Markets Value Index.

If we deduct a 0.25% fee from portfolio 1 and a 0.75% fee from portfolio 2 we see annualized returns from 1990-2010 of 9.6% and 10.5% respectively. If we add up the three bear markets over this period including 1990, 2000-2002, and 2008, we also find that the first allocation averaged a -24.5% decline versus just 21.4% for the second allocation, so there doesn’t appear to be any real difference in risk between the two.

What this actually means is the low cost firm would actually have a fee of -0.9% per year, or pay you 0.9% of your portfolio value every year just to bring you to the expected growth level of a more intelligently constructed asset allocation. Another way to look at this is the total fee is 0.25% + 0.9%, or 1.15% per year, far higher than the 1% maximium that many advisors charge on smaller accounts.

If we were to instead look at balanced allocations, we find that using short term bonds instead of junk bonds allows one to hold a higher percentage in stocks versus bonds to achieve a given level of risk reduction, further improving our relative results.

This is just a public service announcement. Don’t take claims of “low fees” at face value, there is more to it than meets the eye.

An individual investor (without access to DFA) is better off using the following portfolio contruction formula:

(1) determine your stock/bond mix. Use exclusively short term high quality bonds to reduce risk and increase liquidity. Vanguard Short Term Bond Index is the way to go here

(2) determine your US/foreign allocation. Historically, 30% to 40% in non-US stocks has achieved the maximium diversification to a US only portfolio, meaning the least amount of risk. Both higher US and high non-US allocations have increased volatility.

(3) within your foreign allocation, consider your developed to emerging split, and don’t go to heavy on the later. Emerging markets are riskier countries from the standpoint of political risks and market instability, but their economies are also growing much faster (i.e. growth countries) which lowers their expected returns. We don’t know which effect will drive returns going forward, but investors are well advised to consider 1995-1998 and not just 1999-2010 when it comes to emerging markets. Use Vanguard Emerging Market Index here, and keep it to no more than 20% to 25% of non-US.

(4) looking to non-US developed stocks for diversification and high returns, you want to use exclusively value and small cap stocks. They at the same time have higher expected returns than large growth (like the EAFE Index or any subset thereof) and better diversification to a US stock dominated allocation. Here you have to use ETFs from iShares, the MSCI EAFE Value and MSCI EAFE Small indexes. A 50/50 split should be fine.

(5) within the US stock market, avoid speculative sector-like allocations. REITS are unnecessary, as are energy, commodities, or anything else you can think of that is being held up as a “diversifier”. In the US, “market tracking error” is an issue for investors, we don’t like to underperform the market over short stretches. But tilting to small and value are going to do that. Instead of fussing over your 6-12 month relative returns, just realize that it is healthy for a more diversified equity portfolio to deviate from the S&P 500 by 4-8% a year in expectations of higher returns over time.

You can still start with the Vanguard Total Stock ETF, but then should consider adding Vanguard Mid Value and Vanguard Small Value ETFs. Looking at the US side of the portfolio only, 3 examples would be 60% Total Stock, 20% each Mid/Small Value; 40% Total Stock, 30% each Mid/Small Value; or 20% Total Stock, 40% each Mid/Small Value.

So, to summarize, a much better overall allocation than the one listed above would be: 28% Vangaurd Total Stock, 21% Vanguard Mid Value, 21% Vanguard Small Value, 12% iShares EAFE Value, 12% iShares EAFE Small, and 6% Vanguard Emerging Markets Index. Add any allocation to Vanguard Short Term Bond Index necessary to lower risk to an appropriate level to you, and you should be set.

One word of caution, we are all still stinging from 2008, but don’t go too heavy into bonds. For most, anything less than 50% in stocks is too risky from a long term growth perspective. A lot of advisor firms will develop overly conservative allocations because it is easier to keep you in your seat and not have to do as much work talking you through the tough times. This is an additional hidden cost most investors pay that they may not be aware of.

Good luck!

To “Another Advisor” who made the two posts above. Thank you! That is really great analysis. Any updates for 2013? Do you still recommend short term high quality bonds exclusively?