William Bernstein, author of several books on investing, has recently released a short book targeted at giving young folks a primer on saving for retirement. The title is If You Can: How Millennials Can Get Rich Slowly (Amazon link for the reviews). It costs the minimum 99 cents there, but you can also download it for free in PDF, MOBI ebook, and Amazon AZW3 formats. From his website:

William Bernstein, author of several books on investing, has recently released a short book targeted at giving young folks a primer on saving for retirement. The title is If You Can: How Millennials Can Get Rich Slowly (Amazon link for the reviews). It costs the minimum 99 cents there, but you can also download it for free in PDF, MOBI ebook, and Amazon AZW3 formats. From his website:

For years I’ve thought about an eleemosynary project to help today’s young people invest for retirement because, frankly, there’s still hope for them, unlike for most of their Boomer parents. All they’ll have to do is to put away about 20% of their salaries into a low-cost target fund or a simple three-fund index allocation for 30 to 40 years. Which is pretty much the same as saying that if someone exercises and eats a lot less, he’ll lose 30 pounds. Simple, but not easy.

Not easy because unless the millennials learn a small amount about finance, they’ll fall victim to the Five Horsemen of Personal Finance Apocalypse: failure to save, ignorance of financial theory, unawareness of financial history, dysfunctional psychology, and the rapacity of the investment industry.

The book is only 27 pages long, but there are also several “reading assignments” of other books to complete your education. Those other books are not free but they have all been around long enough that it shouldn’t be too difficult to borrow a copy from your local library.

(

(

(Update: Offer now live again until March 31, 2021.)

(Update: Offer now live again until March 31, 2021.)

The third book in the “Investing for Adults” series by William Bernstein is

The third book in the “Investing for Adults” series by William Bernstein is

While we see the live price of the S&P 500 index everywhere, there is much less talk about its dividends. Dividends are an important component of the total return from stocks. I love seeing my quarterly dividend payments arrive every quarter, and combined with our reduced work income, they are enough to cover our household expenses. How reliable is the income stream from owning an S&P 500 index fund (or similar total market fund)?

While we see the live price of the S&P 500 index everywhere, there is much less talk about its dividends. Dividends are an important component of the total return from stocks. I love seeing my quarterly dividend payments arrive every quarter, and combined with our reduced work income, they are enough to cover our household expenses. How reliable is the income stream from owning an S&P 500 index fund (or similar total market fund)?

After finishing

After finishing

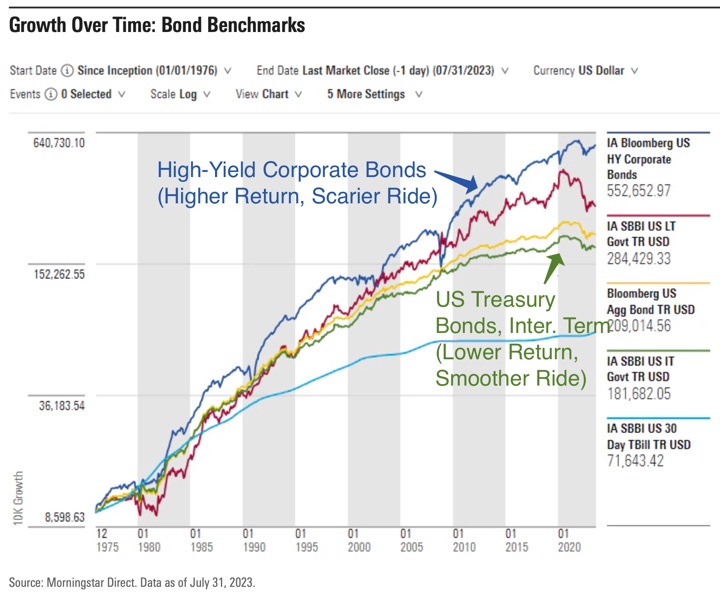

Here are some helpful resources on owning only bonds of the highest credit quality as part of your portfolio asset allocation.

Here are some helpful resources on owning only bonds of the highest credit quality as part of your portfolio asset allocation.  The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)