I was saddened to hear the news of the passing of David Swensen, a well-known investor, endowment fund manager, and educator. From the NY Times obituary:

I was saddened to hear the news of the passing of David Swensen, a well-known investor, endowment fund manager, and educator. From the NY Times obituary:

David Swensen, a money manager who gave up a lucrative Wall Street career to oversee Yale University’s endowment and proceeded to revolutionize endowment investing, in the process making Yale’s the best-performing fund in the country over a 20-year period, died on Wednesday in New Haven, Conn. He was 67.

In addition to “revolutionizing” endowment investing, he also wrote a book for the average individual investor called Unconventional Success: A Fundamental Approach to Personal Investment which I read at a very formative period in my investing education. Even though he is best known for being an early adopter of alternative asset classes like hedge funds, private equity, and direct real estate ownership farmland and timber, he recommended something different for those without the time, skill, and existing money (access). From an interview with the Yale Alumni magazine:

That’s why the most sensible approach is to come up with specific asset allocation targets that you can implement with low-cost, passively managed index funds and rebalance regularly. You’ll end up beating the overwhelming majority of participants in the financial markets.

Here is a brief summary of the important lessons that I learned from his book:

Alignment of interests is key. There are many conflicts of interest in the financial world. Learning to spot them is an important skill. For example, in terms of asset classes, owning shares of businesses (equities) are good because your interests are aligned as a shareholder. However, in the case of high-yield bonds, your interests are not aligned. The borrower wants the lowest interest rate possible, so their job is to seem as safe as possible even if there are significant hidden risks. This is why Swensen recommends sticking only with FDIC-insured cash and Treasury bonds (nominal and TIPS). Take your risks as an owner.

Stick with these six core asset classes. Swensen identified core asset classes that you should invest in. These share three main characteristics:

- They rely on market-generated returns, not from active management skill (as it is a very rare attribute and hard to separate from luck).

- They add a valuable and differentiable characteristic to a portfolio.

- They come from broad, highly-liquid markets.

The six core asset classes he identified are:

- US Equity

- Foreign Developed Equity

- Emerging Market Equity

- Real Estate

- U.S. Treasury Bonds

- U.S. Treasury Inflation-Protected Securities (TIPS)

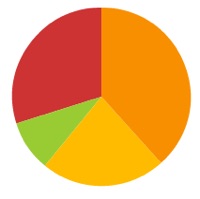

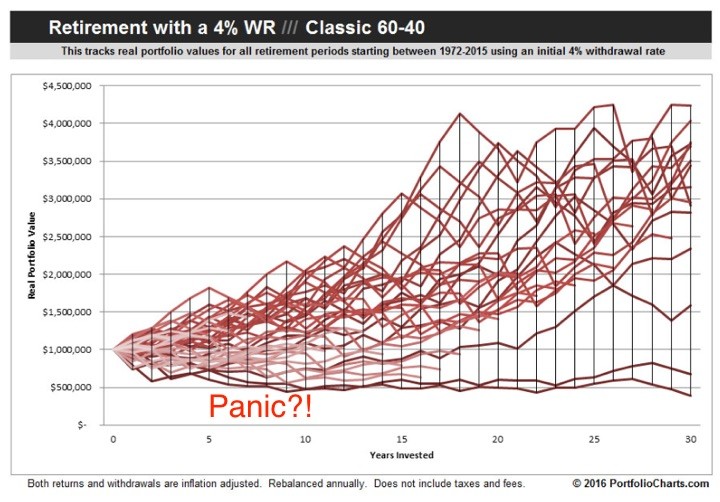

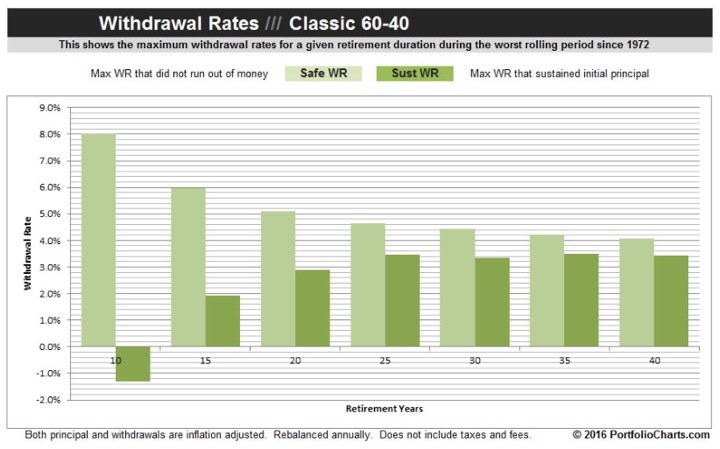

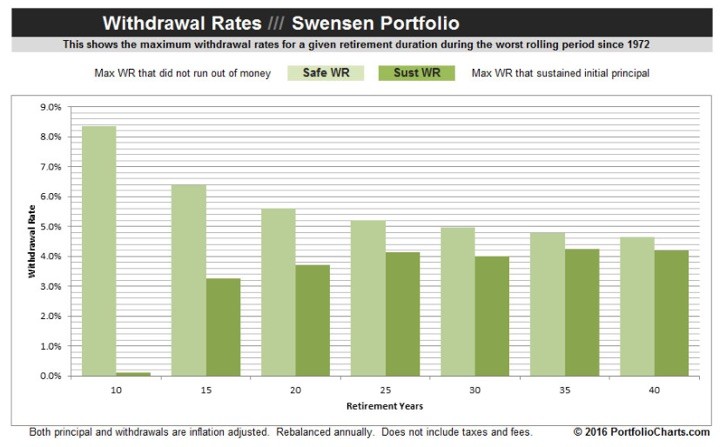

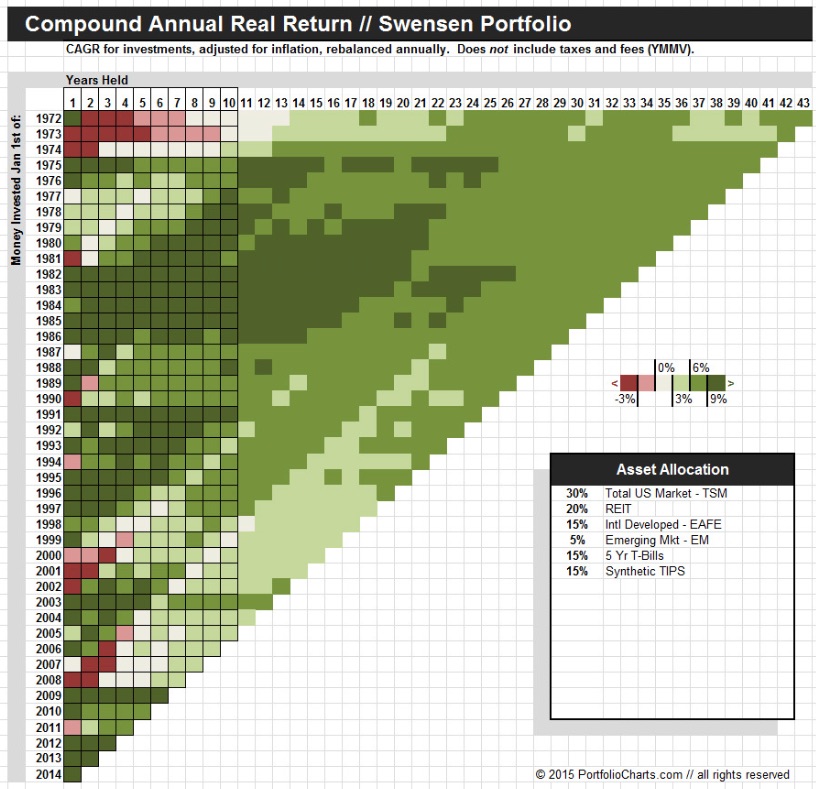

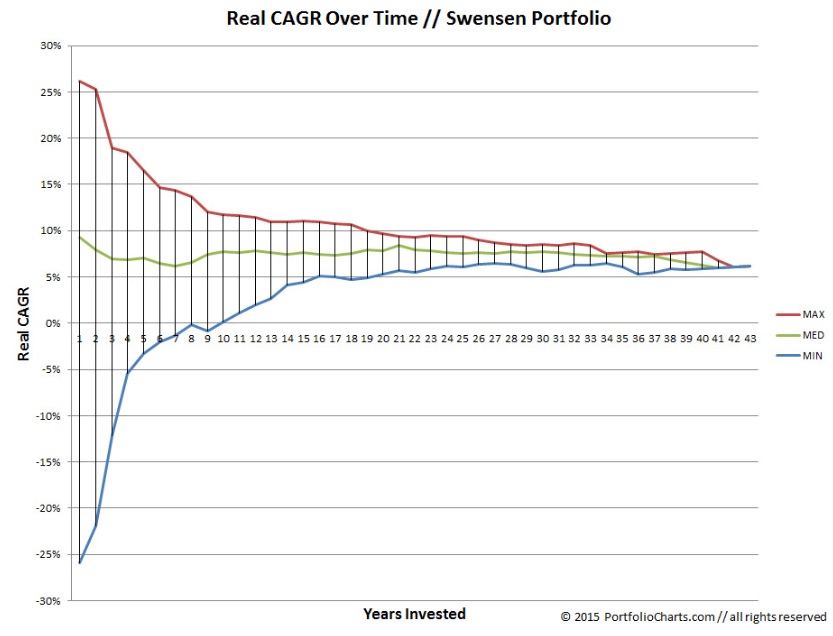

Swensen shared this sample model portfolio asset allocation:

30% Domestic US Equity

15% Foreign Developed Equity

10% Emerging Markets

15% Real Estate

15% U.S. Treasury Bonds

15% Inflation-Protected Securities

This also meant he was recommending against investing in the following:

- US Corporate Bonds

- High-Yield “Junk” Corporate Bonds

- Asset-Backed Securities (like mortgage-backed bonds)

- Tax-Exempt Bonds

- Foreign Bonds

- Hedge Funds

- Private Equity

Not that they are horribly bad, it’s just that you don’t need them. They either have increased risk that isn’t adequately compensated, added management fees and costs that aren’t adequately compensated, or aren’t different enough to add extra return. Don’t make things more complex without a good reason.

Tips on active management. If you still want to pay someone to pick stocks for you, he recommended looking for the following in a manager:

- Hold a limited number of stocks. Bet boldly on fewer companies (high “active share”), as opposed to being a “closet index fund”.

- High rate of internal investment. The managers should have a high percentage of their own net worth in the same funds that they ask you to invest in. They should “eat their own cooking.”

- Limit assets under management. If there is more money flowing in than they can invest efficiently, they should close the fund to avoid asset bloat. This requires them to turn down more money!

- Reasonable management fees. Active management hash higher internal costs than a passive strategy, but you can still charge less than average.

Money isn’t everything. Find a purpose. Finally, David Swensen walked the walk. He could have made billions by staying on Wall Street instead of moving to Yale. He could have made tons of money being a “money guru” on CNBC, etc. The guy didn’t even bother to publish a second edition or “revised” edition of his book, even though that would have also been easy money. He found a mission. More quotes from Swenson (same NYT article):

Mr. Swensen was particularly proud of how the growing endowment had helped the university contribute to financial aid.

“One of the things that I care most deeply about is that notion that anyone who qualifies for admission can afford to go to Yale, and financial aid is a huge part of what the endowment does,” he said in an interview for this obituary in 2014.

“People think working for something other than the most money you could get is an odd concept, but it seems a perfectly natural concept to me.”

Here are some helpful resources on owning only bonds of the highest credit quality as part of your portfolio asset allocation.

Here are some helpful resources on owning only bonds of the highest credit quality as part of your portfolio asset allocation.  Reading

Reading

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)