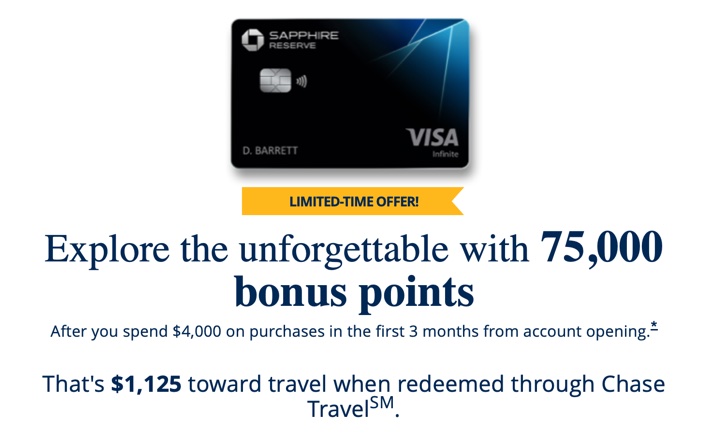

The “ultra-premium” Chase Sapphire Reserve® is offering an opening incentive of 75,000 Ultimate Rewards points which can be redeemed for at least $1,125 of travel when you redeem through Chase Travel(SM), but can also be used in many other ways which can bring even more value. Right now, there is a limited-time offer with increased bonus points. Here is the long list of card perks:

- 75,000 Bonus Ultimate Rewards points after you spend $4,000 on purchases in the first 3 months. Get 50% more value when you redeem your points for travel through Chase Travel(SM). For example, 75,000 points are worth $1,125 of airfare, hotels, and other travel through Chase Travel(SM).

- $300 Annual Travel Credit . Every year, the card will automatically rebate you back up to $300 in travel purchases such as airfare and hotel nights charged on your card.

- 5X total points on flights and 10x total points on hotels and car rentals when you purchase travel through Chase Travel(SM) immediately after the first $300 is spent on travel purchases annually.

- 3X points per $1 spent on travel & dining worldwide. The 3X points on travel kick in immediately after earning your $300 travel credit. 1 point per $1 spent on all other purchases.

- Up to $100 statement credit towards Global Entry, NEXUS, or TSA PreCheck® every four years.

- Airport lounge access via Priority Pass Select membership. Access to 1,300+ airport lounges worldwide after an easy, one-time enrollment in Priority Pass™ Select.

- New: Access to Chase Sapphire Lounges, which are new airport lounges starting at New York’s LaGuardia Airport (LGA), Boston Logan International Airport (BOS), and Hong Kong International Airport (HKG).

- 1:1 point transfer to leading airline and hotel loyalty programs.

- Complimentary DashPass + $5 monthly DoorDash Credits from DoorDash through 12/31/2024. 12 months of complimentary DashPass + Get $5 in DoorDash credits each calendar month while enrolled in DashPass through 12/31/2024. Activate by 12/31/2024.

- Complimentary Instacart+ Membership.: 12 months of complimentary Instacart+ membership, when the membership is activated between 6/15/2022 and 7/31/2024.

- NEW: 2 free years of Lyft Pink All Access and a 3rd year at 50% off when you activate by Dec 31, 2024 (a value of $199/year). Membership auto-renews. Details here. Benefits here.

- Annual fee is $550; $75 for each additional authorized user.

Note the following offer language:

The product is not available to either (i) current cardmembers of any Sapphire credit card, or (ii) previous cardmembers of any Sapphire credit card who received a new cardmember bonus within the last 48 months. If you are an existing Sapphire customer and would like this product, please call the number on the back of your card to see if you are eligible for a product change. You will not receive the new cardmember bonus if you change products.

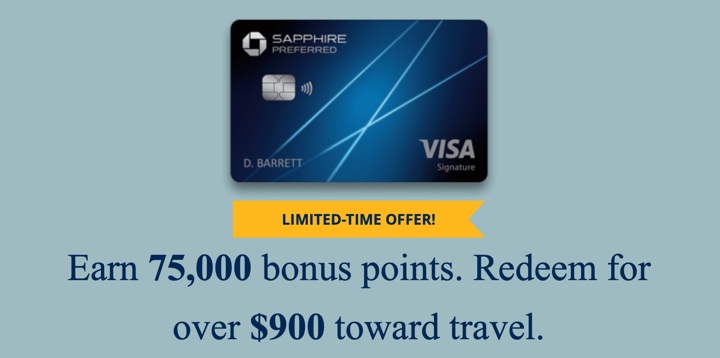

Ultimate Rewards points. The Chase Sapphire Reserve card offers a special 50% bonus on travel redemptions made through the Chase Travel(SM) website. Compare that with the 25% bonus on the Chase Sapphire Preferred. 60,000 Ultimate Rewards = $900 in travel. Similar to Expedia or Travelocity, you can book flights on most major airlines and hotel chains. This makes it much more flexible to spend your points. You can even buy something more expensive than what you can afford with solely points and pay the difference in cash.

If you have other Chase cards that earn Ultimate Rewards points like the Freedom, Freedom Unlimited, Ink Business Cash or Ink Business Unlimited, you can transfer points into this card account and take advantage of the this higher premium. In other words, your existing Ultimate Rewards points balance could be increased in value by getting this card.

Possibly even better value via airline and/or hotel points. This card also allows you to transfer Ultimate Rewards points into hotel and/or airline miles. Transfer to United Airlines, British Airways, Air Canada (new), Singapore Airlines, Korean Air, Southwest, Hyatt Hotels, IHG Hotels, and Marriott Hotels at a ratio of 1 Ultimate Rewards point = 1 mile/hotel point. Miles redemption continue to offer great value for savvy travelers, especially for last-minute travel and business class seats.

Personally, my preferred redemption method is Hyatt points, where I can consistently get over 2 cents per points of value for my hotel bookings. Recently, I have also been using my Ultimate Rewards points on the new Air Canada option.

Cash redemptions are a simple and easy option, but the conversion is a straight 100 points = $1.

Sharing points. Ultimate Rewards points are instantly transferable to other accounts like family members, as long as they have their own Chase card with Ultimate Rewards as an authorized user (free with Chase Freedom). This way, you can pool points together for transfers and redemptions if you like.

Additional card benefits:

- Dedicated customer service line with a live person that answers the phone 24/7. No waiting or complicated phone trees.

- No foreign transaction fees.

- Primary car rental collision damage waiver insurance. Decline the rental company’s collision insurance and charge the entire rental cost to your card. Coverage is primary and provides reimbursement up to $75,000 for theft and collision damage for most rental cars in the U.S. and abroad. Most other cards only offer secondary coverage that kicks in only after the deductible of your individual insurance policy is used.

- Trip Cancellation/Trip Interruption Insurance. If your trip is canceled or cut short by sickness, severe weather and other covered situations, you can be reimbursed up to $10,000 per person and $20,000 per trip for your pre-paid, non-refundable travel expenses, including passenger fares, tours, and hotels.

- Trip Delay Reimbursement. If your common carrier travel is delayed more than 6 hours or requires an overnight stay, you and your family are covered for unreimbursed expenses, such as meals and lodging, up to $500 per ticket

- Enjoy special car rental privileges from National Car Rental, Avis, and Silvercar when you book with your card.

Note that Chase has an unofficial rule that they will automatically deny approval on new credit cards if you have 5 or more new credit cards from any issuer on your credit report within the past 2 years (aka the 5/24 rule). This rule is designed to discourage folks that apply for high numbers of sign-up bonuses. This rule applies on a per-person basis, so in our household one applies to Chase while the other applies at other card issuers.

As for the $300 annual travel credit, “annually” means the year beginning with your account open date through the first December statement date of that same year, and each 12 billing cycles starting after your December statement date through the following December statement date. So it’s not exactly by calendar year, but roughly close and you can likely get this twice under the first year’s annual fee. When you log into the Chase website, there is a handy tracker that tells you how much of your $300 annual credit has been reimbursed, and how much is remaining.

Bottom line. The Chase Sapphire Reserve® Card has a 75,000 Ultimate Rewards points sign-up bonus, 50% boost to all your travel credit redemptions of Ultimate Rewards points, $300 annual travel credit, 3X points on Dining/Travel (more if you use Chase Travel(SM) to book), Priority Pass Select airport lounge membership, up to $100 Global Entry application credit, DoorDash perks, Lyft perks, and more… in exchange for a $550 annual fee. You should compare against that of the Chase Sapphire Preferred card, which has less perks but also a lower annual fee.

Increased offer.

Increased offer.

New limited-time offer. The

New limited-time offer. The

Southwest Rapid Rewards® Plus credit card

Southwest Rapid Rewards® Plus credit card Southwest Rapid Rewards® Premier card

Southwest Rapid Rewards® Premier card Southwest Rapid Rewards® Priority card

Southwest Rapid Rewards® Priority card Southwest Rapid Rewards Performance Business card

Southwest Rapid Rewards Performance Business card Southwest Rapid Rewards Premier Business card

Southwest Rapid Rewards Premier Business card

The Best Credit Card Bonus Offers – May 2024

The Best Credit Card Bonus Offers – May 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - May 2024

Best Interest Rates on Cash - May 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)