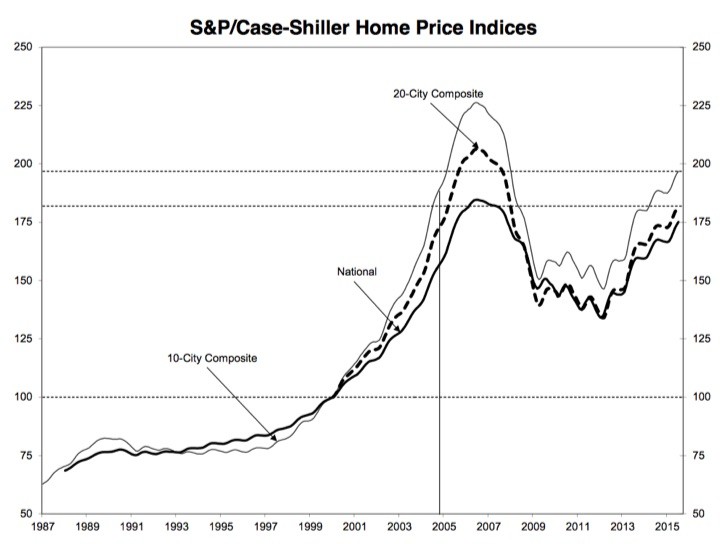

Here’s an update on residential real estate prices via the July 2015 update of the S&P/Case-Shiller Home Price Indices. Included is this chart of their 20-City Composite Home Price Index, which tracks the value of residential real estate in 20 metropolitan areas of the US:

Here’s an update on residential real estate prices via the July 2015 update of the S&P/Case-Shiller Home Price Indices. Included is this chart of their 20-City Composite Home Price Index, which tracks the value of residential real estate in 20 metropolitan areas of the US:

Overall, the S&P/Case-Shiller U.S. National Home Price Index recorded a 4.7% increase over the last 12 months. You can check more cities in the PDF, but the ones with the highest gains over the past 12 months are San Francisco at 10.4%, Denver at 10.3%, and Dallas at 8.7%.

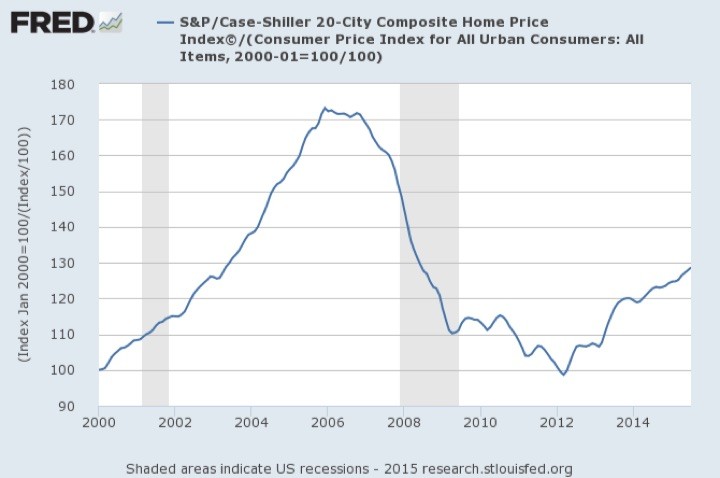

What do home prices look like after being adjusted for inflation? We all tend to think of house prices in terms of nominal values. For example, I bought my first house in 2007 (of course) and I’ll always remember my original purchase price. But that was 8 years ago and even though inflation hasn’t been high it has still been inching along. From June 2007 to June 2015, inflation rose 12% (CPI-U).

As shared in previous updates, here is the Shiller 20-City index adjusted for inflation (CPI-U). Both data sets are not seasonally-adjusted and scaled to 100 as of January 2000.

Home prices are rising even after accounting for inflation, but this bottom chart presents a more tempered view of things.

Still, I feel for first-time homebuyers faced again with housing prices that appear to march upwards every month (and potentially out of reach).

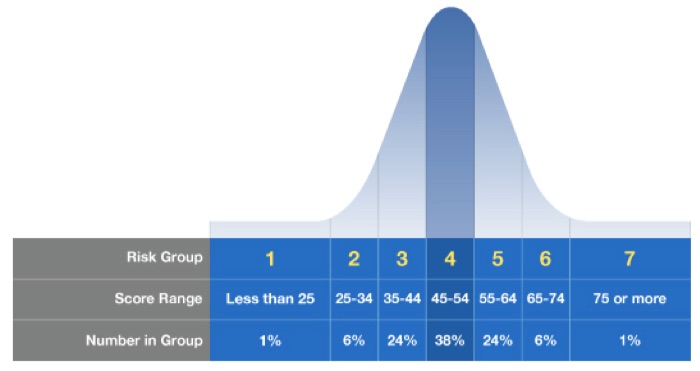

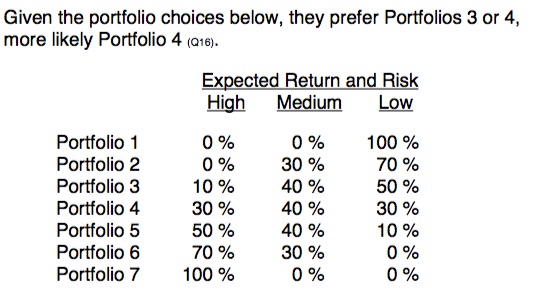

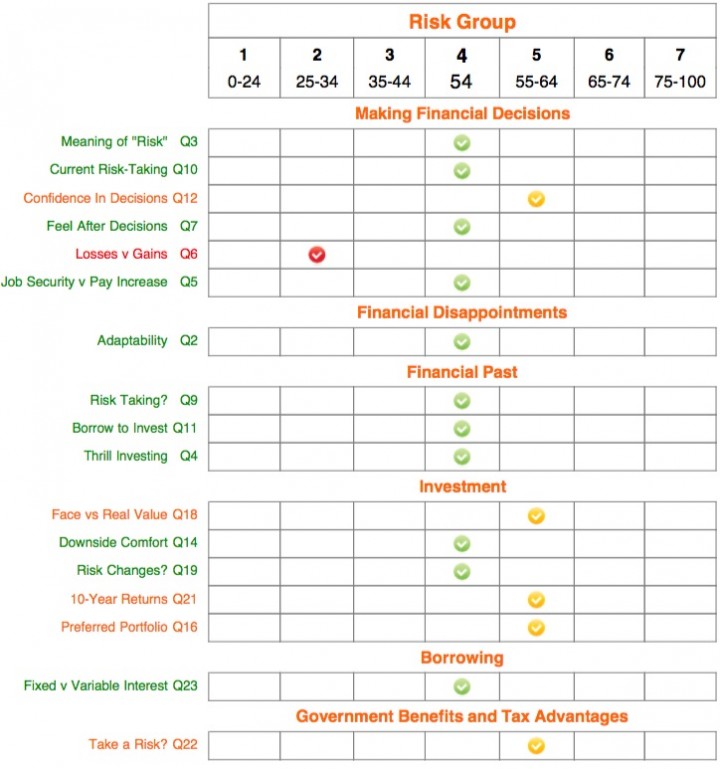

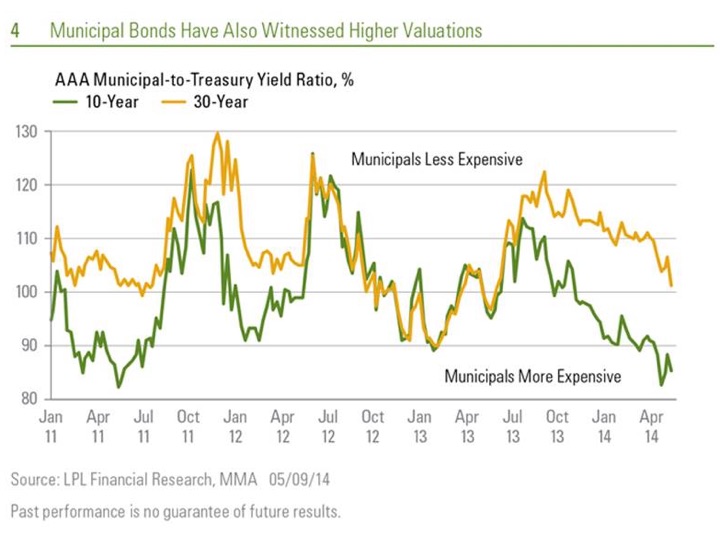

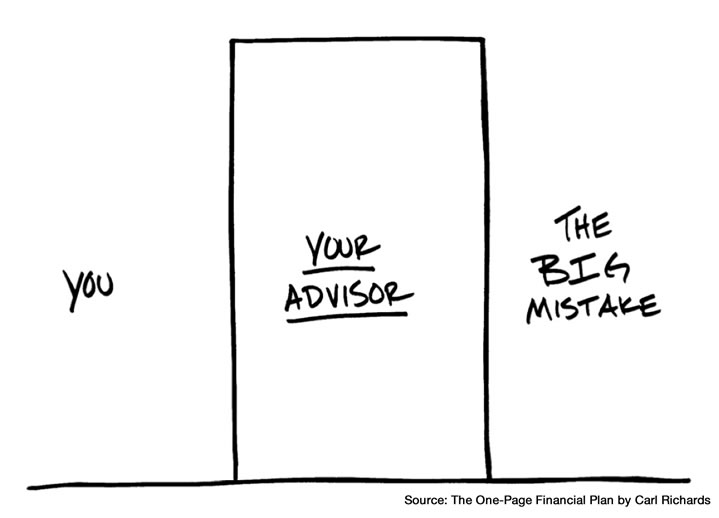

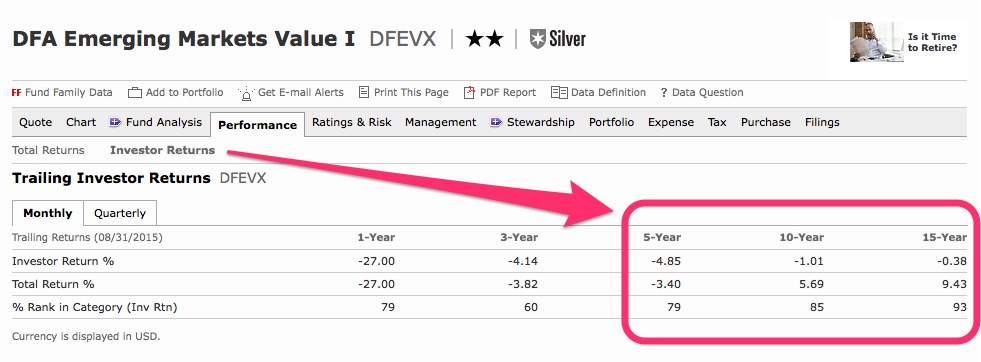

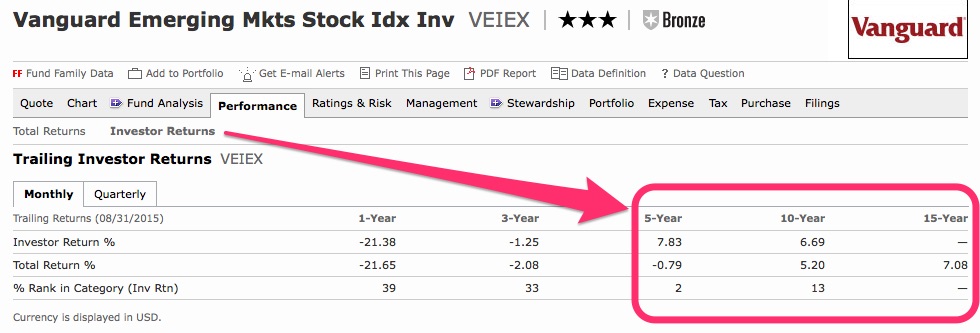

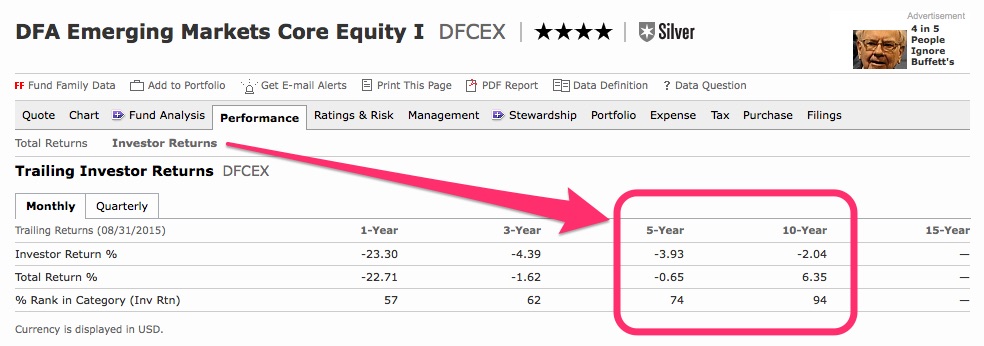

Spend any time researching investments, you’ll eventually run across the concept of “risk tolerance”. If you don’t hold an investment through both the ups and downs, then you won’t enjoy its average returns, either. So how can you predict your behavior ahead of time?

Spend any time researching investments, you’ll eventually run across the concept of “risk tolerance”. If you don’t hold an investment through both the ups and downs, then you won’t enjoy its average returns, either. So how can you predict your behavior ahead of time?

Update 2015. The Tennessee Promise program has welcomed 15,000 students in their first year of offering free community college tuition. The number of students attending community college full-time straight from high school grew 14%. This

Update 2015. The Tennessee Promise program has welcomed 15,000 students in their first year of offering free community college tuition. The number of students attending community college full-time straight from high school grew 14%. This

BullionDirect.com sold gold and silver bullion and even offered to store it in a vault for you for free. How nice of them. Unfortunately, they lied. From a

BullionDirect.com sold gold and silver bullion and even offered to store it in a vault for you for free. How nice of them. Unfortunately, they lied. From a  I’ve written about American Express gift cards several times in the past, mostly when they had a promotion waiving both their purchase fees and shipping fees. In such cases, they were a cheap and efficient way to “time-shift” your purchases if you needed to meet a spending threshold soon to obtain a sign-up bonus, or if you needed some miles sooner for a reward.

I’ve written about American Express gift cards several times in the past, mostly when they had a promotion waiving both their purchase fees and shipping fees. In such cases, they were a cheap and efficient way to “time-shift” your purchases if you needed to meet a spending threshold soon to obtain a sign-up bonus, or if you needed some miles sooner for a reward.

Discover credit cards will work with Apple Pay starting on September 16th, 2015. But the big news is that per this

Discover credit cards will work with Apple Pay starting on September 16th, 2015. But the big news is that per this  The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)