I written about Dimensional Fund Advisors (DFA), a mutual fund family that is powered by top academic research. Another things that makes DFA unique is that they are only sold through approved financial advisors. You can’t buy them with just any old brokerage account. (Exceptions are certain 401(k)-style retirement plans and 529 college savings plans.) Allan Roth has new article about DFA funds in Financial Planning magazine, which is a trade publication targeted to financial professionals.

Why not sell directly to Average Joe investor? Here is David Butler, head of DFA Global Financial Advisor Services:

DFA has no intention of bypassing the advisor channel and offering its funds directly to retail investors. “We think advisors help keep investors disciplined,” Butler says.

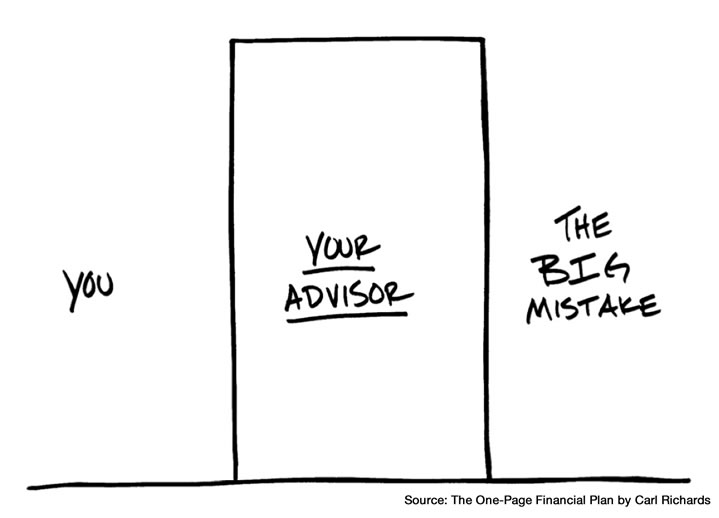

In my previous post The True Value of a Real, Human Financial Advisor, I wrote about this concept. A good client advisor will help you keep your cool when the next disaster comes. Vanguard says that the biggest “value add” from good advisors is their “behavioral coaching”. A good financial advisor keeps you from making the “Big Mistake” that derails your plans.

But later in the same Allan Roth article, the idea of advisors as disciplinarians is called into question.

But do investors get better returns? I tested Butler’s claim that DFA advisors help keep investors disciplined by asking Morningstar to compare the performance gap between the two fund families. The performance gap is the difference between investor returns (dollar weighted) and fund returns (geometric).

Over the 10 years ending Dec. 31, 2014, the DFA annualized performance gap stood at 1.28% versus only 0.22% for Vanguard. When I showed these figures to Butler, he responded, “It’s hard to make an argument about the discipline of advisors based on these figures.”

Here’s a primer on investor returns vs. fund returns. Investor returns are the actual returns earned by investors, based on the timing of their buying and selling activities.

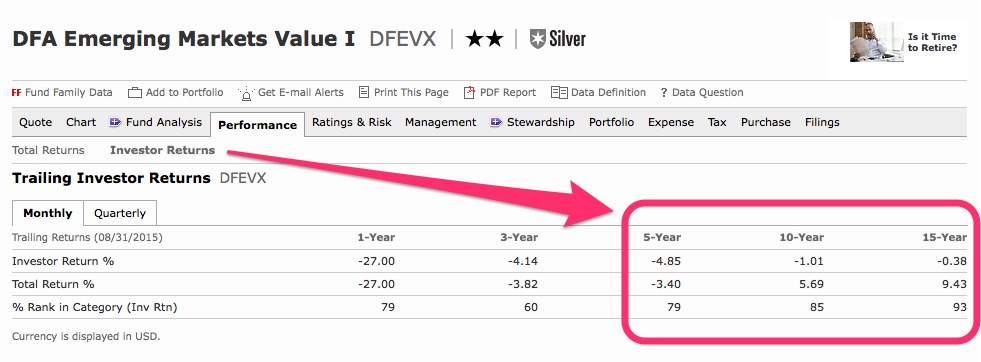

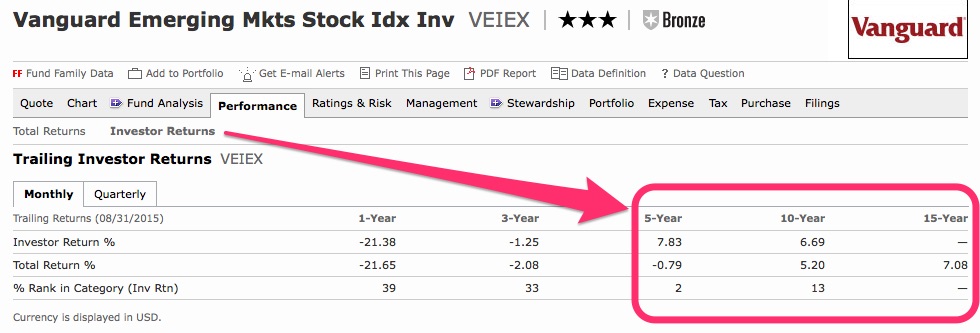

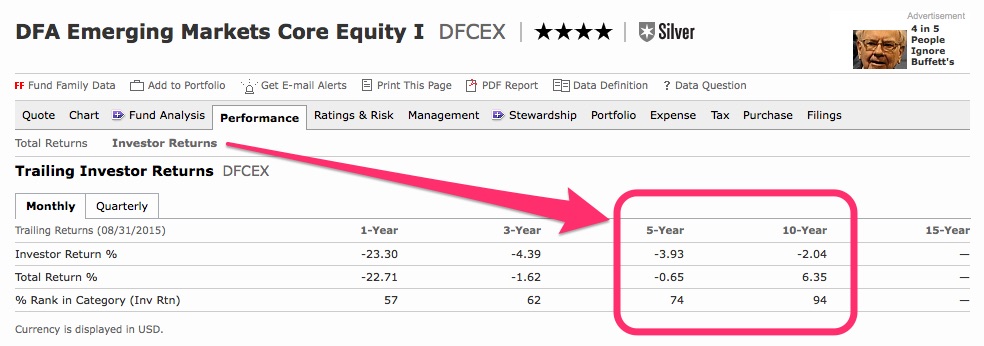

The next step was to compare the investor returns of DFA’s largest fund, DFA Emerging Markets Value I Fund (DFEVX) with $14B in assets with the closest Vanguard competitor, Vanguard Emerging Markets Index Fund (VEMAX) with $54B in assets. I personally think a better comparison would be with their DFA Emerging Markets Core Equity I Fund (DFCEX), so I’m throwing that in as well.

DFA fund returns are often higher relative to index fund competitors. Here’s a Morningstar chart comparing the growth of $10,000 invested 10 years ago in each of the three funds. You can see the DFA funds do slightly better in terms of fund returns. Click to enlarge.

But what about investor returns? I took some screenshots of their respective Morningstar Investor Return pages.

We see that after accounting for the timing of actual cashflows, the average investor in the DFA fund actually lost money with an annualized return of -1.01% and -2.04%! Meanwhile, the average Vanguard investor earned over 6% annualized.

The three mutual funds don’t have the exact same investment objective, but they do both all pull from the overall Emerging Markets asset class. The DFA funds try to focus ways to earn greater long-term return by holding stocks with a higher “value” factor, but it also has a higher expense ratio. The Vanguard fund just tries to “buy the haystack” and passively track the entire index.

Let’s recap. The stated reason why DFA is only sold through advisors is that they offer more discipline. We are told that such behavioral coaching is where human advisors provide their greatest value. However, the evidence available suggests that DFA advisors are less good at trading discipline than when a similar fund is completely open to retail investors.

I found this rather surprising. I used to think that restricting my potential advisors to those were affiliated with DFA was one way of getting an “above-average” advisor. But after doing my own research, I found that even though DFA investments are generally lower-cost, the additional fees charged by individual advisors ranged widely from reasonable to quite expensive.

I am confident there are financial advisors that can provide the proper behavioral coaching that makes them well worth the cost. At the same time, clearly many are not providing the advertised guidance and discipline. The problem remains – how does Average Joe investor find the good ones? I still know of no clear-cut way.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Thanks so much for posting, I think financial planners have their use but there does come a time where you can really become your own financial planner, and just learn/apply things yourself. Especially if you way out-earn what your financial planner does.

Thank you for this in depth analysis re: DFA! I’m a Bogle head, so it doesn’t surprise me. No matter how you slice it, name it, slap an academic label on it — it’s still an ongoing fee structure that takes the life out of your returns

On the other hand, I’ve had a fee-only financial advisor use a modern portfolio analysis of my investments to give me some direction. She developed an asset allocation for me to stay within as I manage my own, and convinced me to use it by pointing out that this asset allocation only dropped 4% during the 2008 crisis.

Keep the posts coming!

Thank you for this article. The sad part is that the people buying those funds also had to pay for the adviser. Hopefully it wasn’t based on assets under management or something like that

Very interesting and not what I expected…but if the investor chooses to hire or leave an advisor, this timing might affect investor returns.

I would also like to see the analysis with another equity asset class, perhaps US small value or US core, to see if this behavioral pattern persists.

I have used DFA for about 10 years. I pay 1/4 percent per year for the funds which I consider a good value. With some of their new funds, it makes it even easier. (My favorite is DGSIX) I’m not promoting DFA, do your own research and do what you are most comfortable with.

The use of M* investor returns is a non-starter. Investor returns tell us a lot more about the sequence of returns than they ever will about behavior. For example, take 2 investors who behave identically by dollar cost averaging over a 10 year period. Now assume the market has a great performance in the early years for investor A, and great performance in the late years for investor B. Using investor return math, one will show a negative gap, the other a positive gap. This tells us nothing about behavior, they behaved identically, it’s just a sequence of returns story. Also consider the experience of the 2008 downturn. We witnessed 500 billion give or take coming out of the markets. Bad behavior? Not really if you dive into the data. That 500 billion was a single digit percentage on a 10 trillion (give or take) asset base. Does that mean 95% behaved perfectly fine and bad behavior occurred at the margin? I think so…But actually, it’s even less of an issue when you consider that much of those assets coming out migrated from active to passive strategies. That’s great behavior! The issue is that the industry is grasping for a way to state their value proposition, but resorting to paternalistic/condescending marketing and stereotyping is questionable at best. The value of an advisor is not paternalism for a limited client, it’s empowerment for an unlimited client. This is also more consistent with what we see in practice – the vast majority behave just fine, which makes sense because they didn’t achieve financial success in the first place by being a behavioral mess…In a nutshell, We don’t have investments with client problems. Most clients are sensible. Most investments are foolish. We have many sensible clients using a few sensible investments.

But wouldn’t Vanguard Emerging Market Index and DFA Emerging Markets Core experience similar effects from sequences of returns and dollar-cost averaging? Same asset class. Very different investor returns.

Jonathan, first, those 2 funds are technically not the same. DFCEX is tilted to size/value, VEIEX is not, but that’s not a big factor to the discussion. DFCEX and VEIEX have experienced dramatically different cash flows, and therefore a different investor returns number. Over the past 10 years DFCEX has gone from less than 1b AUM to over 15b with consistently positive inflows. VEIEX, on the other hand, peaked in assets in 2007 (somewhere between 10b and 15b) and since then has dropped to less than 2b. What’s going on there? Looks like a lot of hot money chasing and abandoning that asset class at Vanguard no?

As a follow up, since markets are zero sum, how can general participants fall short of market returns? The investor return data exists to paint a false narrative. Yes, it does tell us quite a bit about fund flows, sequence of returns, etc., but those may have absolutely nothing to do with behavior. For example, if I sell DFEVX or DFCEX in the heat of the downturn in 2008, does that mean I have bad behavior? No, you have to answer the question of why instead of stopping right there and assume it’s bad behavior. If I sell those funds tax-efficiently (lower cap gain or tax loss) to get to a better position, such as moving from component funds to broad “core” funds (i.e., lower cost, lower turnover, better overall efficiency in keeping taxes low and/or fully capturing risk premiums…), that’s very good behavior, but it doesn’t fit the narrative and it’s very difficult to measure in the aggregate. Investor behavior can only be measured one investor at a time, and IMHO, it’s not the epidemic our industry claims it is.

> how can general participants fall short of market returns?

Actually, it is very easy. If you take money from the market when it falls, you will only be getting interest on your cash. That interest is generally far lower than the expected market returns. You underperformed the market by not being invested in it.

mb, “general participants” refers to all participants in the market and assumes a zero sum game, for every winner there is a loser and vice versa. Collectively, all participants cannot underperform or outperform themselves…For those who did not participate in the market, they are then not “general participants.”

Derek,

I am not sure what you mean by a zero-sum game.

Suppose we have two classes of assets — the market and cash. The market returns, say, 8% on average, the cash returns 2%. Every person is invested in both with some allocation to the market and some to cash. If the drop in the market makes you change your allocation by moving money from the market to cash, you are likely losing 6% on the part of your assets that you moved. You may still be a participant of the market (you can even go back to 100% stock allocation after a while) but underperforming. Note that the part of your assets still invested in the market performs just fine.

MB, part-time investors experience partial returns. Some outperform, some under-perform, but neither have a consistent/exploitable advantage. It’s a zero sum game because we can’t just focus on those who under-perform. To assume that one group consistently under-performs is to assume that another group consistently outperforms. That’s not supported by evidence…The degree of under-performance is a function of risk factor consistency and cost. Those who are the most risk-consistent (full-time investors) and manage cost (explicit and implicit) best have the highest expected return for a given portfolio mix. “Outperformance” is technically not possible relative to gross market returns. To assume otherwise is to assume alpha exists. One might “outperform” a given index, but that’s a function of risk factor differences and implementation costs vs. the index. No free lunch.

Derek, I am not disagreeing with you about “no free lunch” and the lack of exploitable advantages. My point (which has been made many times before) is that behavioral patterns can lead to underperformance of individual investors relative to the market.

Yes, we agree that behavior matters, but it’s my stance that we can’t use DALBAR or M* Investor Returns to prove it, so we should question the true motivation of blog posts like this one (“advisors don’t provide discipline”), or especially articles from the advisor community that are nothing more than examples of data mining to fit a pre-conceived theory (that their true value is behavior management and that bad behavior is the norm, not the exception, both false IMHO.)

Overall, “bad” behavior cuts both ways. Some win, some lose. The expected outcome is a net loss attributable to the aggregate cost of implementing the “behavior.” But we can’t assume bad behavior is never profitable. Random chance indicates otherwise.

Thanks!

DT

>Overall, “bad” behavior cuts both ways. Some win, some lose. The expected outcome is a net loss attributable to the aggregate cost of implementing the “behavior.” But we can’t assume bad behavior is never profitable. Random chance indicates otherwise.

Derek, this is where we disagree. “Bad behavior” (i.e. withdrawing from the market because of price fluctuations) can sometimes be profitable in some cases, but on average leads to losses.

not sure what part of “the expected outcome is a net loss attributable to the aggregate cost of implementing the “behavior.” isn’t clear? Sounds like you and I agree just fine…

Great article. And it rings true when you say,”I still know of no clear-cut way” (to find a good advisor). That’s sadly too true — and I say that as a Registered Investment Advisor. At the very least, however, the advisor should be able to provide a prospective client with a sheet showing long-term investment performance. And the advisor should also acknowledge, in writing, that the firm accepts “Fiduciary” responsibility, which basically means it puts your interests ahead of its own.

Interesting data point. Is this generally true across a wide range of funds? Has anyone done a similar analysis with the core funds (Total International, Total Stocks, Total Bonds, Emerging Markets, Inflation-protected, and REIT)?

These posts do a great job of helping us make up our own mind on who we should invest our money with!! These posts are the reason why I keep coming back to your blog year after year.

To many financial bloggers fill there posts with fluff and useless common sense information. Your posts consist of great information based on real data.

Thanks for the great post.

1.I would add that investing could be simple, but it is not easy. So most people do need help.

2.Quote “A good financial advisor keeps you from making the “Big Mistake” that derails your plans.” This is true only if the advisor is experienced.

3.M* data is amusing, but it is not your returns.

4.Quote “The problem remains – how does Average Joe investor find the good ones?” It is difficult to find an ethical and trustworthy advisor. Just like any type of population, take for example tenants, 1 in 100 are good tenants, the rest are scums.

5.The right financial advisor provides value above holding your investments. After a little bit of reading many people think that are expert in investing (it could be simple as stated in 1). If you ask 100 drivers about their driving skills, all of them will say they are above average.

I just looked up DFAs largest US small value fund (DFFVX) and Vanguard’s Small Value Index fund (VISVX). The former had investor returns 2% per year higher than investment returns. The latter had investor returns 2% per year lower than investment returns. Does that mean we can conclude investors using DFA funds (through advisors) are 4% per year better behaved than DIY investors (I sincerely hope no advisor with access to DFA is using the Vanguard fund)?

Looking at diversified portfolios (Vanguard Lifestrategy Growth & DFA Global Equity), we see the former saw a -0.9% spread between investor/investment returns, the latter saw only -0.4%. That’s probably reasonable: with a good advisor, they’re adding maybe 0.5% per year in the behavior department compared to experienced DIY investors who know enough to use Vanguard. Compared to less knowledgeable investors or those too smart for their own good, that number is easily over 1%.

But there’s also a hidden behavior cost not seen in investor/investment return calcs: DIY investors tend to gravitate towards less volatile/lower return portfolios. “Age in bonds” is a common metric here. And, as we all know, that exposes them to considerable inflation/purchasing power risk. If you are sticking with a portfolio that will barely exceed inflation over your lifetime compared to a pro-growth allocation like 60/40, you are still costing yourself a tidy sum, even I you are staying the course.