Vanguard announced on January 16, 2019 that its founder, John C. Bogle, passed away on at his home in Bryn Mawr, Pennsylvania at 89 years old. There will no doubt be many tributes; here are a few same-day articles from WSJ, Bloomberg, Reuters, and great tweet from Morgan Housel.

Vanguard announced on January 16, 2019 that its founder, John C. Bogle, passed away on at his home in Bryn Mawr, Pennsylvania at 89 years old. There will no doubt be many tributes; here are a few same-day articles from WSJ, Bloomberg, Reuters, and great tweet from Morgan Housel.

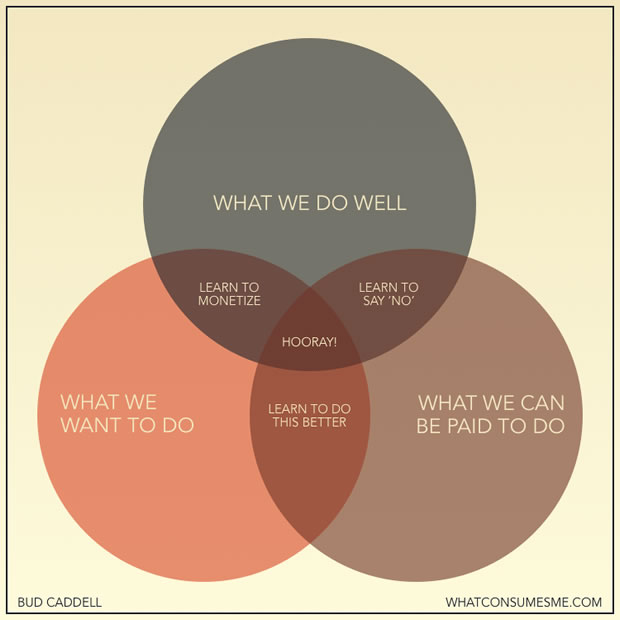

Jack Bogle was a champion of thrift, simplicity, and keeping investing costs low. While he reached the popularity level where people would write entire columns about “Why Bogle is Wrong about This or That”, I was always annoyed when people would pick at one little thing he said. I felt that his strongest message was that of common sense. Sometimes it took multiple readings and time, but he really offered a lot of valuable, reasoned knowledge in his books. Almost exactly a year ago, I wrote about my Jack Bogle Appreciation curve:

My first mutual fund investment was in the Janus Mercury fund in the very early 2000s. I was chasing performance and Morningstar ratings, and the fund was actively managed with high turnover and high expenses. Thanks to reading his books, my subsequent investments were in low-cost Vanguard funds that were available to a DIY investor. You can now buy ultra-cheap commission-free ETFs from nearly every brokerage account. New investors may take this for granted, but I’m old enough to remember that this was not always the case! This was solely due to Vanguard’s success:

He created a unique structure where the unnecessary “Helper” fees stayed in the pockets of the people who invested with Vanguard (and indirectly anyone who invests in a low-cost index fund today). This has resulted in an estimated $1 trillion saved by average everyday investors.

Today, my family is financially secure and we have a pretty clear plan for the future as well. The majority of my net worth is held at Vanguard. My life was materially improved by a man that I never got the honor to meet. The best I could do was to win a personally-signed book from a charity auction for his foundation.

Thank you, Mr. Bogle. I will try my best to heed your advice.

p.s. If you do not know that I am talking about, please do yourself a favor and read The Little Book of Common Sense Investing from the library or buy a copy. It is very short and a good place to start.

I’ve been catching up on some memoirs and recently finished

I’ve been catching up on some memoirs and recently finished

Reading children’s books to my kids has become a regular source of new wisdom. I guess that’s not surprising, if the goal is to teach kids about life. Here’s one that came across recently and keeps popping back in my head.

Reading children’s books to my kids has become a regular source of new wisdom. I guess that’s not surprising, if the goal is to teach kids about life. Here’s one that came across recently and keeps popping back in my head. Day 4 of the

Day 4 of the

With the ongoing bull stock market, more people are reaching

With the ongoing bull stock market, more people are reaching

Charles Munger is probably best known as the Vice Chairman of Berkshire Hathaway and partner of Warren Buffett. The University of Michigan Ross School of Business recently shared a

Charles Munger is probably best known as the Vice Chairman of Berkshire Hathaway and partner of Warren Buffett. The University of Michigan Ross School of Business recently shared a

Johan Norberg wrote Progress: Ten Reasons to Look Forward to the Future, which was a 2017 Book of the Year for The Economist and the Observer. I haven’t read it, but it seems like a well-researched book with hard evidence on why we should be more optimistic.

Johan Norberg wrote Progress: Ten Reasons to Look Forward to the Future, which was a 2017 Book of the Year for The Economist and the Observer. I haven’t read it, but it seems like a well-researched book with hard evidence on why we should be more optimistic. The Best Credit Card Bonus Offers – May 2024

The Best Credit Card Bonus Offers – May 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - May 2024

Best Interest Rates on Cash - May 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)