![]() Vanguard is making a few changes to their Vanguard Prime Money Market Fund, which is often their highest-yielding option:

Vanguard is making a few changes to their Vanguard Prime Money Market Fund, which is often their highest-yielding option:

- Name change. Vanguard Prime Money Market Fund will change its name to Vanguard Cash Reserves Federal Money Market Fund.

- Even safer. It will now invest only in securities fully backed by the U.S. government or cash. I believe that they used to invest in some highly-rated short-term commercial paper.

- Even cheaper. Basically, everyone will get the lower expense ratio from Admiral shares which previously had a $5,000,000 minimum (!). The minimum investment to get started is still $3,000.

- No more checkwriting. You can still get checkwriting with certain other funds, including the Vanguard Federal Money Market Fund.

The actionable event here is that if you own the Prime Investor Shares (VMMXX), you can manually convert to the Admiral Shares (VMRXX) to immediately take advantage of the lower expense ratio (and thus higher yield) instead of waiting until possibly 2021:

Existing Investor share owners (VMMXX): You have the option to immediately convert† to Admiral Shares to begin taking advantage of the lower expense ratio. You can find simple step-by-step instructions here. If you don’t initiate a conversion, you’ll be automatically converted sometime between late 2020 through 2021. Note: Our checkwriting service isn’t available for the fund’s Admiral share class. Checkwriting is available for Vanguard Federal Money Market Fund and other Vanguard money market funds.

While this fund usually offers one of the highest cash sweep amongst brokerage accounts, the interest rate is still really low at about 0.10% SEC yield right now. At the same time, many online savings accounts are at about 0.80%. Still, if you own this fund you might as well convert now. The Vanguard Federal Money Market Fund remains Vanguard’s default cash sweep option, which historically has yielded slightly less than Vanguard Prime.

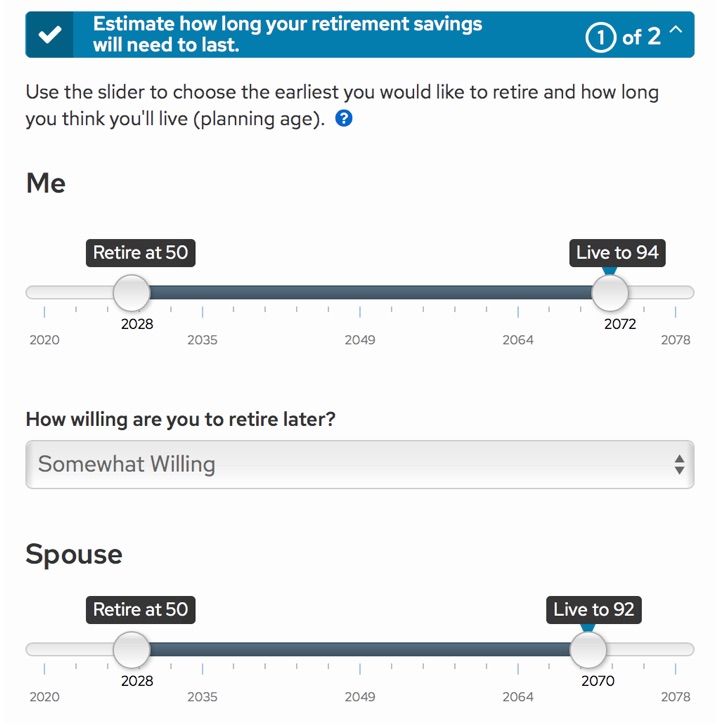

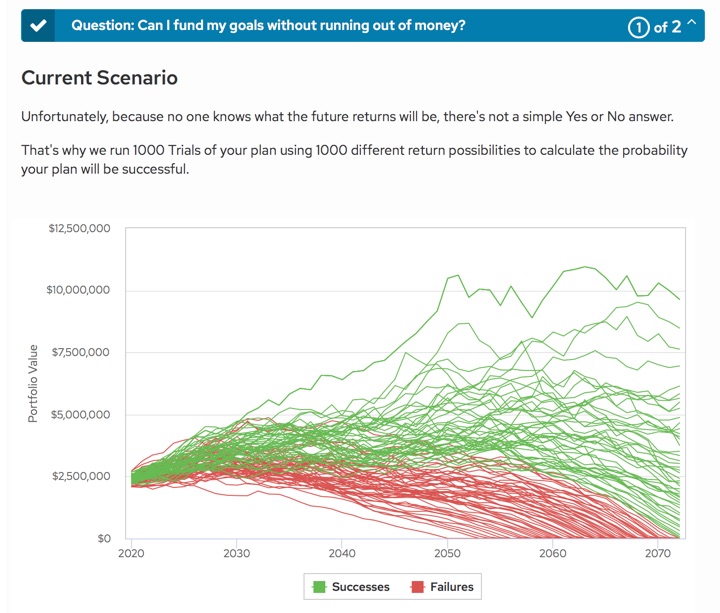

Schwab has rolled out a new digital financial planning tool called

Schwab has rolled out a new digital financial planning tool called

Interest rates on liquid savings accounts keep dropping, making bank bonuses more attractive on a relative basis. Opening new accounts are more hassle, so I usually want at least double the interest rates I could get by doing nothing. This

Interest rates on liquid savings accounts keep dropping, making bank bonuses more attractive on a relative basis. Opening new accounts are more hassle, so I usually want at least double the interest rates I could get by doing nothing. This

Financial institutions increasingly want all of your money under one roof. Brokerage firms and robo-advisors are adding savings accounts and debit cards. Banks want to let you trade stocks. If you have built up some sizeable assets, you can make extra money when they decide to pay you to move over your assets. Try them out, see if you like them, and move again if you need to.

Financial institutions increasingly want all of your money under one roof. Brokerage firms and robo-advisors are adding savings accounts and debit cards. Banks want to let you trade stocks. If you have built up some sizeable assets, you can make extra money when they decide to pay you to move over your assets. Try them out, see if you like them, and move again if you need to.

The CFA Institute Research Foundation publishes some short finance ebooks on Amazon Kindle that qualify as continuing education credits for Chartered Financial Analysts (CFAs), a type of investment professional certification.

The CFA Institute Research Foundation publishes some short finance ebooks on Amazon Kindle that qualify as continuing education credits for Chartered Financial Analysts (CFAs), a type of investment professional certification.  During these stressful times, many of us are doing a lot more shopping online (unfortunately for local retailers). The competition to get you to spend as much as possible has evolved to take full advantage of all of our psychological weaknesses. This Wired article discusses

During these stressful times, many of us are doing a lot more shopping online (unfortunately for local retailers). The competition to get you to spend as much as possible has evolved to take full advantage of all of our psychological weaknesses. This Wired article discusses

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)