Yesterday, I looked back at extending the Maslow Hierarchy of Needs to Personal Finance. The basic idea of the triangle or pyramid is that lower needs must be satisfied before the higher needs can be addressed. For example, one must first obtain food and water before worrying about protecting my property. In terms of personal finance, you need to cover your food and shelter bills before worrying about homeowner’s insurance premiums.

Now let’s explore how investment professionals have extended this concept to portfolio investing. Again, the bottom level is the most important and forms the “base” of a solid portfolio. After that, you can move on the next concern. You can see that there is debate even amongst experts as to relative importance.

Here’s Christine Benz of Morningstar in How Do Your Financial Priorities Stack Up With Our Pyramid?

Here’s Morgan Housel of Fool.com in The Hierarchy of Investor Needs:

Here’s Cullen Roche of Pragmatic Capitalism in Thoughts on the Hierarchy of Investor Needs:

The four common factors are:

- Security Selection

- Tax Efficiency

- Investor Behavior

- Asset Allocation

Two out of the three proposed pyramids above have Investor Behavior as the most important. I can see how this factor has the greatest impact on real-world returns, but it is also the hardest to really quantify ahead of time. You can write down on a piece of paper “I will not panic during the next crisis but will do XX instead” but that doesn’t mean you’ll actually do it (though it will probably help on average). In addition, it is also intertwined with asset allocation since the less your portfolio value drops in a bear market, the more likely you’ll stick with your plan. Meanwhile, you can quantify fees and transaction costs quite easily.

I think this debate makes for interesting conversation for investing geeks like myself, but in the end a good investor would address all of these factors. For example, I would never put off examining fees just because it is at the top of such a pyramid.

Back in 2014, Google bought Word Lens, a neat app that translated a few languages in real time using your smartphone’s camera. The live translation feature has been integrated into the Google Translate app (

Back in 2014, Google bought Word Lens, a neat app that translated a few languages in real time using your smartphone’s camera. The live translation feature has been integrated into the Google Translate app (

While standing in line at the Costco pharmacy, I found myself in a discussion with another Costco member who apparently saves over a thousand dollars a year on her meds by buying them there instead of her neighborhood CVS. (I also got an earful about the Medicare Part D “

While standing in line at the Costco pharmacy, I found myself in a discussion with another Costco member who apparently saves over a thousand dollars a year on her meds by buying them there instead of her neighborhood CVS. (I also got an earful about the Medicare Part D “

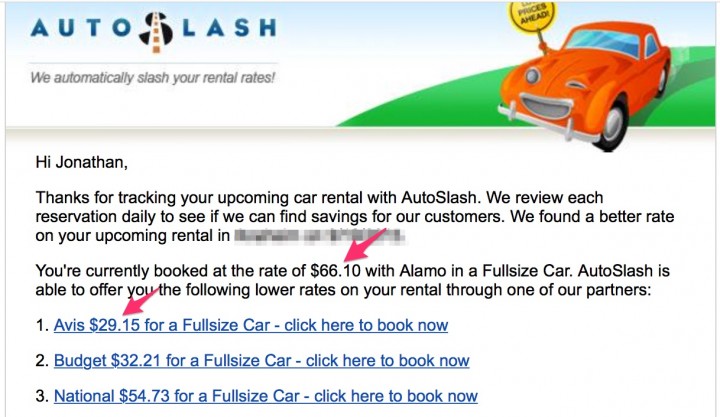

Here’s a quick tip that I’ve been using regularly this summer for saving money on car rentals.

Here’s a quick tip that I’ve been using regularly this summer for saving money on car rentals.

Updated. Buying a house is always an exciting yet terrifying time. Deciding on how much we can “afford” is often limited by how much someone will lend us. Mortgage lenders use income size, income stability, credit score, down payment size, and other factors before approving a loan. Let’s explore the idea of a “rule of thumb” to greatly simplify such a complicated matter. The most common way to express affordability is as a multiple of your household or individual annual income.

Updated. Buying a house is always an exciting yet terrifying time. Deciding on how much we can “afford” is often limited by how much someone will lend us. Mortgage lenders use income size, income stability, credit score, down payment size, and other factors before approving a loan. Let’s explore the idea of a “rule of thumb” to greatly simplify such a complicated matter. The most common way to express affordability is as a multiple of your household or individual annual income. Gold is an asset class that is part commodity, part currency, and part insurance policy. As I write this, gold prices are at a 5-year low. I own a little physical gold for cultural reasons, but I don’t consider it part of my asset allocation and I place it in the “

Gold is an asset class that is part commodity, part currency, and part insurance policy. As I write this, gold prices are at a 5-year low. I own a little physical gold for cultural reasons, but I don’t consider it part of my asset allocation and I place it in the “

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)