The NYT Times Haggler just helped a reader who made two small claims on his homeowner’s insurance for (1) a fallen ceiling fan and (2) a stolen bike. Not only did State Farm deny both claims, but they subsequently refused to renew his insurance the next year! This is a unique circumstance, and I’ve heard of co-workers with similar problems. But of course the power of daylight again helped this lucky reader:

The NYT Times Haggler just helped a reader who made two small claims on his homeowner’s insurance for (1) a fallen ceiling fan and (2) a stolen bike. Not only did State Farm deny both claims, but they subsequently refused to renew his insurance the next year! This is a unique circumstance, and I’ve heard of co-workers with similar problems. But of course the power of daylight again helped this lucky reader:

After the Haggler’s interactions with State Farm, Mr. Joseph sent an email to the Haggler with the subject line “It worked!” A representative at the company had contacted him and, in conversation, was much more forthcoming than Ms. Risinger. Mr. Joseph learned that in New York City, the average for homeowners is one claim every 38 years.

“Two in two years,” Mr. Joseph recalled this rep telling him, “that makes us concerned.” But after digging deeper into Mr. Joseph’s claims, the company decided that it wanted to keep him as a customer.

You should never make a claim for such small things like a stolen bike or broken appliance (especially if apparently it’s not even covered). Every claim you make will be recorded in an insurance database forever. As a result, if you’re not going to make a $500 or $1,000 claim, then why would you set your deductible to $250 or $500? Set it to $2,500 or higher if you can swing it. I’ve been inching ours up over the years, and I believe it is now $10,000 and even higher for natural disaster insurance. Enjoy the lower premiums, but remember to stock up your emergency fund in return. I used to have a special rider for my wife’s engagement ring, but cancelled that as soon as the value become “non-catastrophic” for our finances.

And we’ve all learned a valuable lesson: Homeowner’s insurance is for disasters. Which means that if you’re lucky, you’ll spend money on it for years and years and never get a dime back.

Exactly. Insurance is not an investment, a maintenance plan, or a replacement for properly securing your property. Insurance is there to protect you from something truly catastrophic happening, like your entire house burning down and them putting you up in a residential hotel for months while they rebuild it (which happened to our friends).

Bottom line: If you have homeowner’s insurance, you should set your deductible as high as you can tolerate. It should be a painful number. Take your premium savings and put it towards your cash reserves.

Our partner Citi has launched yet another new card, AT&T Access More MasterCard® from Citi. This AT&T co-branded card obviously targets a niche, but read on if you will be in the market for a new GSM phone in the next year ($650 is the full price of a new iPhone 6). As such, this card took a little extra research and analysis. Be sure to read all the details before applying, so you understand how to get everything possible out of this offer.

Our partner Citi has launched yet another new card, AT&T Access More MasterCard® from Citi. This AT&T co-branded card obviously targets a niche, but read on if you will be in the market for a new GSM phone in the next year ($650 is the full price of a new iPhone 6). As such, this card took a little extra research and analysis. Be sure to read all the details before applying, so you understand how to get everything possible out of this offer.

I’m not sure exactly what details of this investment I am allowed to share, so I’ll save that part for later. It will be good for you guys to pick apart, but it doesn’t really matter for other investors as the project is already 100% funded. I’m just waiting on my first interest payment in May, and hope to be done by October. At the end of the year I will get a 1099-INT.

I’m not sure exactly what details of this investment I am allowed to share, so I’ll save that part for later. It will be good for you guys to pick apart, but it doesn’t really matter for other investors as the project is already 100% funded. I’m just waiting on my first interest payment in May, and hope to be done by October. At the end of the year I will get a 1099-INT. New inflation numbers were just

New inflation numbers were just  Navy Federal Credit Union has solid bank and loan products, including checking accounts with ATM rebates, competitive mortgage rates, and limited-time 0% balance transfer promotions.

Navy Federal Credit Union has solid bank and loan products, including checking accounts with ATM rebates, competitive mortgage rates, and limited-time 0% balance transfer promotions.

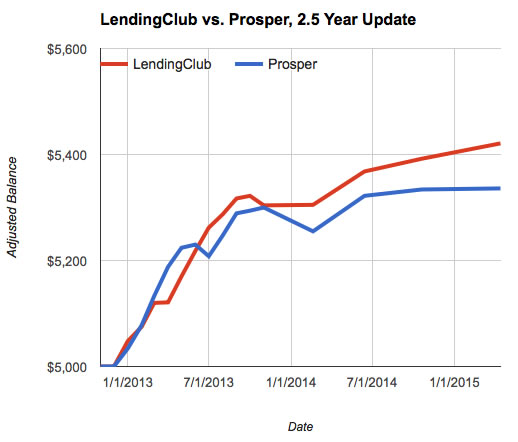

In November 2012, I invested $10,000 into person-to-person loans split evenly between

In November 2012, I invested $10,000 into person-to-person loans split evenly between

Our family keeps a year’s worth of expenses (not income) put aside in cash reserves; it provides financial insurance with the side benefits of lower stress and less concern about stock market gyrations. In my opinion, emergency funds can actually have a

Our family keeps a year’s worth of expenses (not income) put aside in cash reserves; it provides financial insurance with the side benefits of lower stress and less concern about stock market gyrations. In my opinion, emergency funds can actually have a  Updated with new coupon. As a homeowner, unfortunately there’s always a use for these… Lowe’s has a new $10 off $50 coupon available to everyone if you sign up for their promotional e-mails. You can use a secondary e-mail or simply unsubscribe after you get the coupon. Simply visit their front page at

Updated with new coupon. As a homeowner, unfortunately there’s always a use for these… Lowe’s has a new $10 off $50 coupon available to everyone if you sign up for their promotional e-mails. You can use a secondary e-mail or simply unsubscribe after you get the coupon. Simply visit their front page at

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)