Update 11/30/23: At some point after publishing this post, PenFed changed the terms of this offer. It used to say:

Can I share/forward this offer to a friend or family member?

Yes, this offer is open to everyone. Maximum bonus received is $750 per member.

But, now it says:

This exclusive Bonus Offer is only available for the original recipient of the email and cannot be shared or made eligible beyond the original recipient.

Not a customer-friendly move, PenFed, to pull such a bait-and-switch!

Original post:

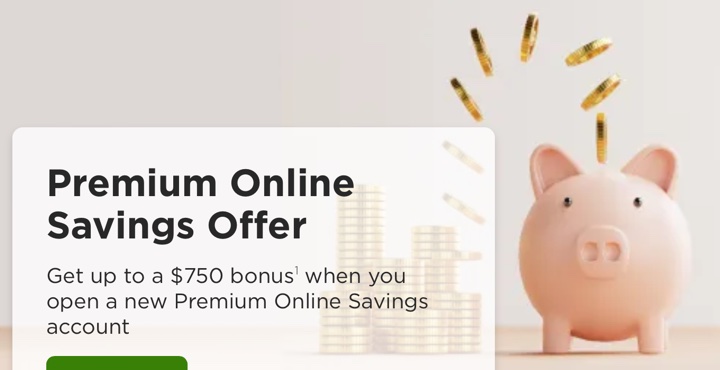

Pentagon Federal Credit Union (PenFed) is offering a up to $750 deposit bonus when you add new funds to their Premium Online Savings account. You get $150 for every $10,000 of new deposits, up to $750 for $50,000 in new deposits. Must deposit new money by 12/30/2023 and maintain that level until 4/30/2024 (four months). There are two different offer links, one for those opening a new account and those adding new funds to an existing account:

- Offer link for new Premium Online Savings Accounts

- Offer link for existing Premium Online Savings Accounts (must still add new money)

From the offer FAQs and fine print:

What is considered new money?

New money is funds deposited from an external account into your new Premium Online Savings account. The funds must be new funds to PenFed.Can I share/forward this offer to a friend or family member?

Yes, this offer is open to everyone. Maximum bonus received is $750 per member.Can I open multiple Premium Online Savings accounts and receive a bonus for each?

No, this offer is limited to one bonus and one new Premium Online Savings account per member.Your account must stay open and be in good standing when bonus is credited to your account. Please allow up to 60 days for the Bonus to appear in your account.

Here are the highlights of the PenFed Premium Online Savings account:

- 3.00% APY as of 11/29/23.

- No monthly fees, no minimum balance requirement.

- Anyone can join PenFed via partner organization. You’ll have to keep $5 in a Share savings account, in addition to opening a separate Premium Online Savings account.

Napkin math. If you deposit towards the end of the 30-day funding period, your technical minimal holding period is 4 months (~120 days). If you meet one of the tiers exactly (such $10k or $50k), then the bonus works out to an additional 4.50% annualized yield. If you assume the current 3.00% APY, that adds up to a total effective interest of roughly 7.50% APY annualized for 4 months.

In absolute terms: If, for example, you deposit $50,000 right before December 30th, 2023 and keep it until April 30th, 2024, you’ll end up with $750 bonus + $500 in interest (from the 3% APY) = $1,250 at the end of the 4-month period.

PenFed no longer does a hard credit pull on new membership applications, so anyone should be able to join without having to pay any fees, other than a $5 deposit into Share Savings (only refundable when you close your membership). They also have interesting certificate rates from time to and time, and right now I see them advertising 5.35% APY on 15- and 18-month certificates (as of 11/29/23). If you’re in the market, also take a look at their interest rates on car loans and mortgages.

I already have a PenFed membership, so I hope to time things properly so that this can be another drop in my 2023 IRA challenge bucket (maybe count as 2024?).

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)