Rates are rising… slowly. Marcus Bank has a 10-month promo CD paying 1.10% APY ($500 min, early withdrawal penalty is 90 days of interest). Ally Bank has a 14-month promo CD paying 1.00% APY (No min, early withdrawal penalty is 60 days of interest). If you have a short-term window, these (sadly) are competitive rates. I figure I should mention them, although you can also get 1%+ APY from a liquid savings account if you know where to look.

Personally, I’m only keeping my cash in short-term lock-ups with high effective APYs like the deposit promos recently from CIT Bank (still live) and Live Oak Bank (probably too late if you haven’t started) and Marcus Bank (already expired).

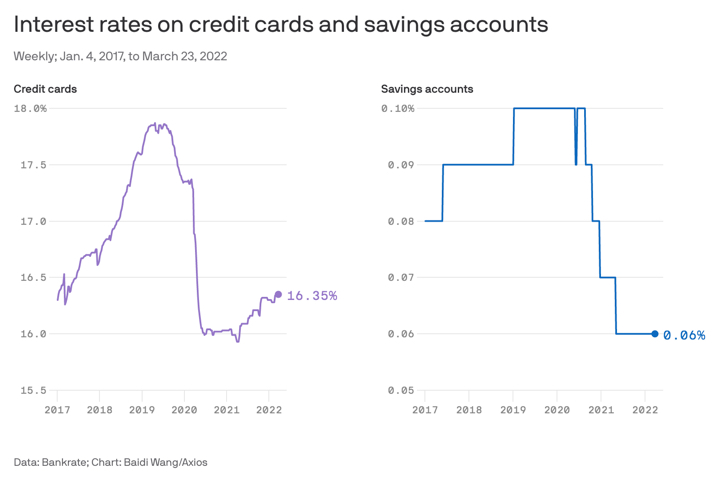

Overall, I definitely don’t on locking in any 5-year CDs due to the mix of current low rates and impending possibility of higher rates soon. Inflation numbers are still elevated. However, I also don’t expect to see significantly higher rates on savings accounts right away. Banks tend to raise their rates on credit cards first and by a lot, and savings account last and by a little. Via Axios (notice the different scales!):

After a delay of two years, my family finally used up our flight credits and stash of hotel points to travel internationally to Vancouver and Whistler, British Columbia for some snow-filled fun. I was a bit worried about how well my “budget” cellular service

After a delay of two years, my family finally used up our flight credits and stash of hotel points to travel internationally to Vancouver and Whistler, British Columbia for some snow-filled fun. I was a bit worried about how well my “budget” cellular service

Many online banking, stock trading, crypto, and fintech apps use the Plaid service to provide easy funding via your existing bank accounts. The price of this convenience is that you are providing some very sensitive data to a small, private company. They have your bank login information and can see all your transaction data. (Visa was in an agreement to acquire Plaid for over $5 billion, but it was cancelled to due

Many online banking, stock trading, crypto, and fintech apps use the Plaid service to provide easy funding via your existing bank accounts. The price of this convenience is that you are providing some very sensitive data to a small, private company. They have your bank login information and can see all your transaction data. (Visa was in an agreement to acquire Plaid for over $5 billion, but it was cancelled to due  Here’s my monthly roundup of the best interest rates on cash as of March 2022, roughly sorted from shortest to longest maturities. I look for lesser-known opportunities available to individuals while still keeping your principal FDIC-insured or equivalent. I use this information for both my cash reserves and as possible bond substitutes. Check out my

Here’s my monthly roundup of the best interest rates on cash as of March 2022, roughly sorted from shortest to longest maturities. I look for lesser-known opportunities available to individuals while still keeping your principal FDIC-insured or equivalent. I use this information for both my cash reserves and as possible bond substitutes. Check out my

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)