Rates are rising… slowly. Marcus Bank has a 10-month promo CD paying 1.10% APY ($500 min, early withdrawal penalty is 90 days of interest). Ally Bank has a 14-month promo CD paying 1.00% APY (No min, early withdrawal penalty is 60 days of interest). If you have a short-term window, these (sadly) are competitive rates. I figure I should mention them, although you can also get 1%+ APY from a liquid savings account if you know where to look.

Personally, I’m only keeping my cash in short-term lock-ups with high effective APYs like the deposit promos recently from CIT Bank (still live) and Live Oak Bank (probably too late if you haven’t started) and Marcus Bank (already expired).

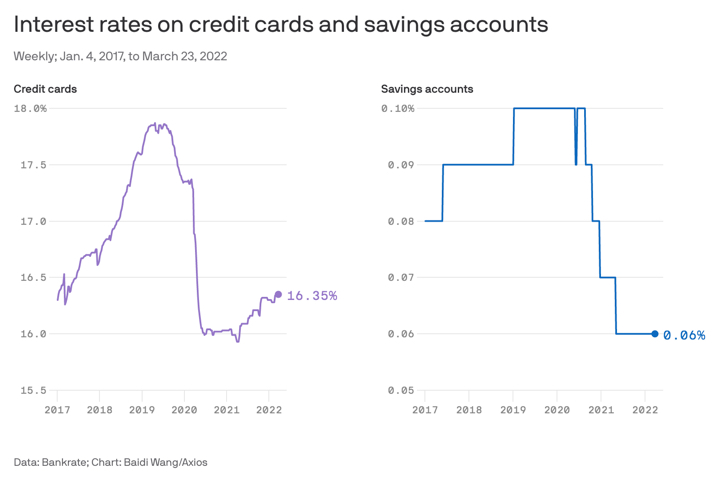

Overall, I definitely don’t on locking in any 5-year CDs due to the mix of current low rates and impending possibility of higher rates soon. Inflation numbers are still elevated. However, I also don’t expect to see significantly higher rates on savings accounts right away. Banks tend to raise their rates on credit cards first and by a lot, and savings account last and by a little. Via Axios (notice the different scales!):

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

You can buy a 1-year U.S. Treasury note yielding 1% right now; the 2-year yields 2.3%. From 2 years out to 10 years the yield curve is very flat. Once you own these you can sell them at any time, but they could go down in value if rates rise–you are only guaranteed that yield if you hold them to maturity. But the nice thing about the steepness in the near part of the yield curve is you can buy a 2-year and be reasonably sure it won’t lose value over the next 12 months unless the 1-year yield rises above that 2.3% (because in a year from now you will be holding a 1-year note).

You can buy these in increments of $1000 through Schwab with no commissions.

Good point, the US Treasury rate curve has been moving around quite a bit. I remember switching to Treasuries when the 10-year hit 3% last time, and it may happen again soon.

https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_yield_curve&field_tdr_date_value_month=202203