Over time, more and more people are seeing the benefits of investing in stocks and bonds through low-cost index funds. Here is a chart from Morningstar showing the overall flow of assets out of actively-managed and into passively-managed US equity funds over the last 15 years.

For a while, people wondered if low-cost digital advisors that managed a portfolio of index funds for a modest fee would take over. The picture looks a little different today.

Wealthfront was one of the early digital-only startups, promising to manage a diversified portfolio of low-cost ETFs for you for a modest 0.25% of assets, even if you had as little as $500 to invest. They tried a few different things over the years, including changing up their model portfolios, trying to add a in-house risk-parity fund, and even recently adding crypto and individual stock options. Their final move came this week, when they announced they would be sold to UBS for $1.4 billion. This wasn’t exactly a huge exit, given the huge amount of venture capital they had burned through over the years. As usual with such acquisitions, they promise both “nothing will change” and “things will only get better”.

In hindsight, I am relieved that I didn’t let Wealthfront handle my assets. They clearly had no firm guiding principles, tweaking their portfolios with each new trend. Based on the reporting, it looks like they sold their customers to the highest bidder, as UBS is not exactly known for low-cost passive investing. This play is widely seen a way for UBS to obtain young investors that will one day be rich (read: one day will generate lots of wealth management fees). See UBS Buys Wealthfront for $1.4 Billion to Reach Rich Young Americans and Why a Bank for the Super Rich Is Taking Aim at the Younger Merely Rich.

Is this move what is best for Wealthfront’s customers? Or what was best for Wealthfront’s investors? Mark the date. I will be checking to see what Wealthfront clients own in 5 and 10 years, if that is still possible. Keep in mind that any portfolio changes usually result in taxable events.

Funds flowed into index funds for a simple reason: they performed better and made folks more money. Index funds performed better primarily due to low costs and low turnover (low tax costs). However, it doesn’t appear that Wealthfront could operate successfully independently while offering low costs. One way or another, the new owners are going to try and extract more money per client either via portfolio changes or higher fee products.

Unfortunately, I worry that even Vanguard, in its pursuit of growth, is gradually going down the same path as many large nonprofits. Many “nonprofits” are huge bureaucracies that chase money as eagerly as any corporation – more money means bigger salaries to management, more political power, and greater career advancement. (Side note: I thought that Vanguard got away with their huge Target Date fund capital gains distribution with little media attention, but now see: Massachusetts investigating sales of target date funds to retail investors after word of surprise tax bills.)

I don’t write much about robo-advisors any more. They showed promise initially, but apparently the business model just isn’t working.

Here’s my (late) quarterly update on the income produced by my “

Here’s my (late) quarterly update on the income produced by my “

Here’s my (late) quarterly update on my current investment holdings, as of 1/23/22, including our 401k/403b/IRAs and taxable brokerage accounts but excluding a side portfolio of self-directed investments. Following the concept of

Here’s my (late) quarterly update on my current investment holdings, as of 1/23/22, including our 401k/403b/IRAs and taxable brokerage accounts but excluding a side portfolio of self-directed investments. Following the concept of

Instead of focusing on the current hot thing, how about stepping back and taking the longer view? How would a steady investor have done over the last decade? Most successful savers invest money each year over a long period of time.

Instead of focusing on the current hot thing, how about stepping back and taking the longer view? How would a steady investor have done over the last decade? Most successful savers invest money each year over a long period of time.

Here’s my monthly roundup of the best interest rates on cash as of January 2022, roughly sorted from shortest to longest maturities. Significant changes since last month: 7.12% Savings I Bonds annual purchase limit reset for 2022, new 2% APY LFCU checking, few other minor rate changes. I plan on buying I Bonds in late January. You could choose to wait until mid-April to see the next rate, but you’d likely be earning less interest in the meantime.

Here’s my monthly roundup of the best interest rates on cash as of January 2022, roughly sorted from shortest to longest maturities. Significant changes since last month: 7.12% Savings I Bonds annual purchase limit reset for 2022, new 2% APY LFCU checking, few other minor rate changes. I plan on buying I Bonds in late January. You could choose to wait until mid-April to see the next rate, but you’d likely be earning less interest in the meantime. The GMO quarterly letter is on my recurring “must read” list, and the 2021 Q3 letter

The GMO quarterly letter is on my recurring “must read” list, and the 2021 Q3 letter

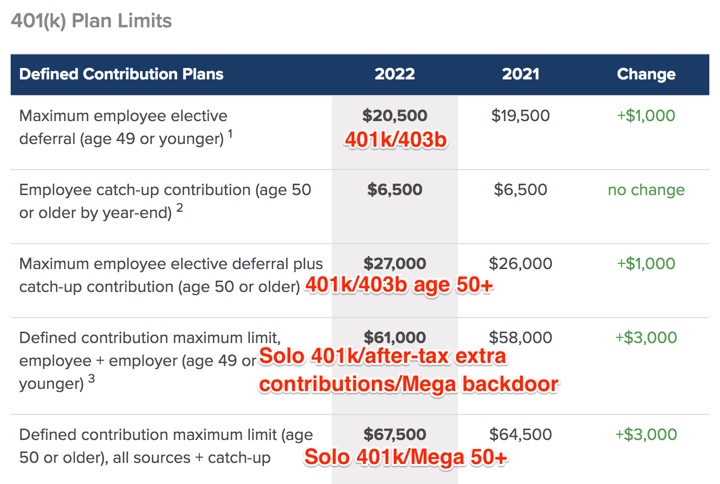

The beginning of the year is a good time to check on the new annual contribution limits to the various available retirement accounts. Our income has been quite variable these last few years, so I regularly adjust the paycheck deferral percentages based on expected income for the year. This

The beginning of the year is a good time to check on the new annual contribution limits to the various available retirement accounts. Our income has been quite variable these last few years, so I regularly adjust the paycheck deferral percentages based on expected income for the year. This

2021 is finally in the books! Most of my portfolio is in low-cost index funds across various asset classes, which I purposefully ignore most of the time as I believe the proper time horizon is at least several years long. However, I do check in once a year. Per Morningstar, here are the annual returns for select asset classes as benchmarked by popular ETFs after market close 12/31/21.

2021 is finally in the books! Most of my portfolio is in low-cost index funds across various asset classes, which I purposefully ignore most of the time as I believe the proper time horizon is at least several years long. However, I do check in once a year. Per Morningstar, here are the annual returns for select asset classes as benchmarked by popular ETFs after market close 12/31/21.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)