The big financial news over the weekend was the failure of both Silicon Valley Bank and Signature Bank. They failed, the FDIC took over and fulfilled its duties, and then the uninsured business owners convinced the Fed to backstop everything (aka “bail them out”).

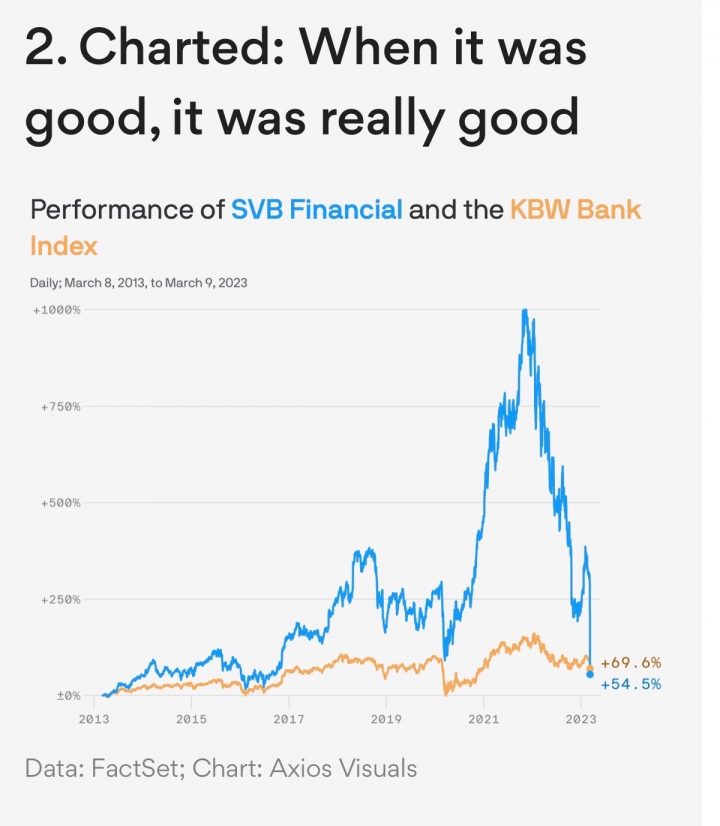

As a simple individual investor trying to keep his family assets safe, my first takeaway was simply that you can’t expect to see a bank failure coming. Silicon Valley Bank was the cool kid for a long time. Here’s a chart from Avios of its stock price vs. an index tracking bank stocks overall:

Most of Silicon Valley Bank’s deposits were from start-up businesses, but individual households had accounts with them as well. I don’t mean to pick on DepositAccounts, but they are a respected site and they gave Silicon Valley Bank a Health Grade of A:

How is the average investor supposed to do any better? This is why I don’t care about health grades for banks from anyone. I don’t need to examine their investment portfolio, underwriting standards, or stock price. As a depositor, either they have FDIC insurance, or they don’t.

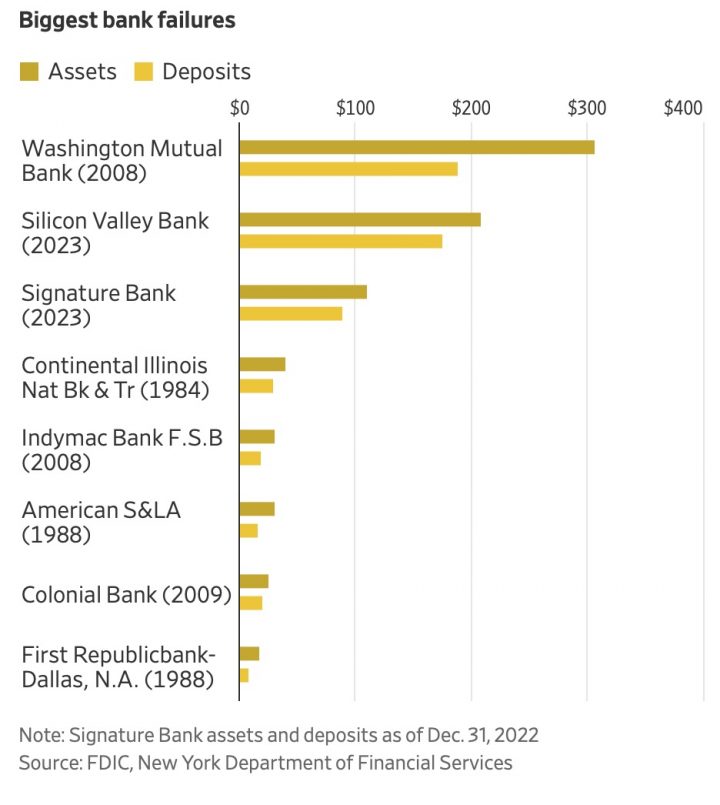

Big name banks can fail even if their assets are greater than their deposits. Silicon Valley Bank and Signature Bank are now the second and third largest bank failures ever (even inflation-adjusted), and only behind to Washington Mutual during the financial crisis. From WSJ:

I wonder how the list will look in a year?

As an individual, there is no reason to exceed the FDIC insurance limits.. FDIC insurance provides great peace of mind. Don’t waste it.

Got anywhere close to $250,000 in a single bank account? Know that the FDIC insurance coverage limit applies per depositor, per insured depository institution for each account ownership category. You may actually achieve more than $250,000 of total coverage at a single bank, depending on how you have titled your accounts. Here are the official online calculators:

NCUA Electronic Share Insurance Calculator (ESIC)

FDIC Electronic Deposit Insurance Estimator (EDIE)

Everyone loves a 100% money-back guarantee. A popular option on insurance policies is the “Return of Premium” rider. Let’s say you buy a $1,000,000 term life insurance for 30 years at $1,000 a year. At the end of 30 years, if you’re still alive, the insurance policy will no longer pay you the $1,000,000 if you die, but it will return all the premium you paid ($30,000). In your mind, you could think of it as “no risk” because you’ll get your $30,000 back no matter what!

Everyone loves a 100% money-back guarantee. A popular option on insurance policies is the “Return of Premium” rider. Let’s say you buy a $1,000,000 term life insurance for 30 years at $1,000 a year. At the end of 30 years, if you’re still alive, the insurance policy will no longer pay you the $1,000,000 if you die, but it will return all the premium you paid ($30,000). In your mind, you could think of it as “no risk” because you’ll get your $30,000 back no matter what!

Data breaches are scary fact of life these days. If you have a Mastercard, did you know that they offer a

Data breaches are scary fact of life these days. If you have a Mastercard, did you know that they offer a  My current commute/workout/kid taxi listening is old Berkshire Hathaway shareholder meetings after finding them in

My current commute/workout/kid taxi listening is old Berkshire Hathaway shareholder meetings after finding them in

Updated for 2021. Here is the second part of my big list of free consumer reports from over 50 different reporting agencies. The first part included your

Updated for 2021. Here is the second part of my big list of free consumer reports from over 50 different reporting agencies. The first part included your  Many of us are driving less these days. Nearly all of the major auto insurers are providing some sort of refund – this

Many of us are driving less these days. Nearly all of the major auto insurers are providing some sort of refund – this

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)