Mosaic is a new crowdfunding start-up allows investors to invest in clean energy projects with as little as $25. A solar power farm needs financing to get built. They sell the energy produced to customers like major utilities and then pay investors back. Mosaic takes a cut. Mosaic has recently been more projects since their debut (and sellout) earlier this year.

Below is a screenshot of an actual project with a 12-year horizon with expected 5.5% yield that is currently in funding – the one I was looking at yesterday already funded! If you live in California, you’re likely to be familiar with PG&E which made a 20-year agreement to purchase power from this project. On the production end, Panasonic is guaranteeing a minimum power production level for 12 years (or else they cover the difference). I’m not sure what the interest rates on these types of project would be on the open market, but right now Yahoo Finance shows the average yield on a AAA-rated 10-year corporate bond to be 3.60%.

I’ve written about my

I’ve written about my

Right now, freshmen are moving into dorms all around the country and parents are scrambling to pay the bills. I’ve written about how many students

Right now, freshmen are moving into dorms all around the country and parents are scrambling to pay the bills. I’ve written about how many students  Here are a few new proposed class action settlements that may affect you. They both involve popular food products that marketed themselves as “All Natural” and ran into some controversy:

Here are a few new proposed class action settlements that may affect you. They both involve popular food products that marketed themselves as “All Natural” and ran into some controversy: Yesterday, I posted a

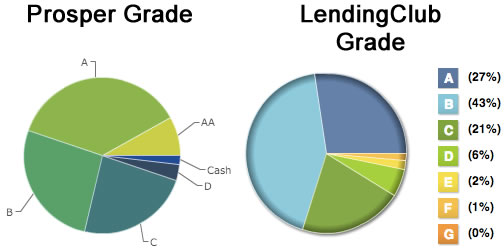

Yesterday, I posted a  I invested $10,000 into person-to-person loans in November 2012, split evenly between

I invested $10,000 into person-to-person loans in November 2012, split evenly between

I’ve written about how recent fee disclosure requirements for 401(k) retirement plans have brought a spotlight on

I’ve written about how recent fee disclosure requirements for 401(k) retirement plans have brought a spotlight on

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)