As the last part of my ongoing Beat The Market Experiment, here’s the December 2012 update for my consumer loan portfolio. See also my $10,000 Benchmark and $10,000 Play portfolio updates for December 2012.

On 11/1/12, I deposited $10,000 split evenly between Prosper Lending and Lending Club, and went to work lending other people money and earning interest. Here’s how I’m doing it:

- 8-10% target return, net of defaults and fees. Each site provides an estimated return based on the interest rate and expected delinquency rate, but I am also using specific filters to try and maximize my return. Overall, I would say my risk profile is moderate/conservative. If I can get an 8% net return over the next 3+ years in the current interest rate environment, I’ll view the portfolio as a success.

- Minimal time commitment. I’ve done the manual loan-picking thing, and I’m over it. 400 loans at $25 a pop would take forever. Both sites allow you to save customized loan filters and use an automated investment algorithm to pick a portfolio for you.

- Loan Filters. I’m constantly tinkering with the loan filters, but you can get a good idea of what I am using by reading this best Prosper filters post and this older LendingClub filter post. Nothing too fancy, just some broad filters based on historical inefficiencies that may or may not persist.

- Loan term lengths and reinvested interest. I thought about only buying loans with 3-year terms in order to have a clean ending timeframe to this experiment, but in reality that would leave a lot of cash at the end as many people pay off their loans early. Also, higher rates are found in 5-year loans. Given the ample liquidity I found in secondary market, if I wanted to end the experiment I could just sell all my loans and cash out. (In October, I sold all of my existing loans on the secondary Folio market in a matter of days, quite easy as long as you’re willing to sell at a discount.) This way I will reinvest any additional cash into new loans maximize return.

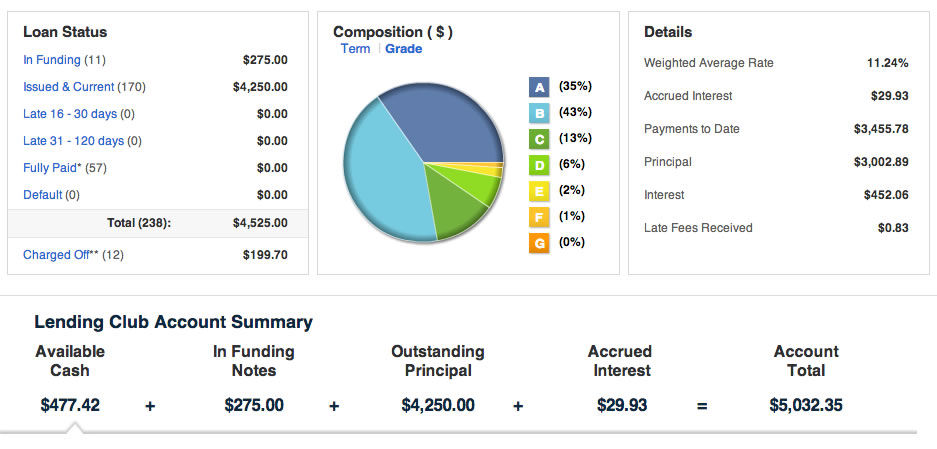

LendingClub Details

Below is a screenshot of my LendingClub account as of 12/3/12:

I have $4,250 in issued loans, and still have $750 to invest because sometimes even though you commit your money, the loan does not actually fund due to a variety of reasons. Currently, I have mostly A and B-rated loans with a weighted average rate of 11.24%. I believe the estimated rate of return after defaults is around 8%.

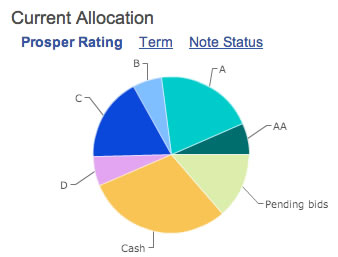

Prosper Details

Below is a screenshot of my Prosper account as of 12/3/12:

I have about $2,800 in issued loans, $700 in pending loans, and $1,500 in cash. The average loan quality is a little lower than LendingClub. I expect to be fully funded within 2 months. My average loan yield is about 14%, with an estimated rate of return around 9%. We’ll have to wait a while before I get any sense of actual return.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Interesting. If I were doing this I would probably have made loans over a three-year period, 1/3, 1/3, 1/3, just to get some diversification over time.

Nicely described.

Liquidity in secondary market (foliofn) would suddenly vanish if the economy turns south. It’s similar to subprime mortgage mess of 2008-09; only more dangerous because the loans are all unsecured.

On LC I am also observing quality of loan applications deterioring. Right now it seems to be borrower’s market and not lender’s market.

@Andy – Not a bad idea, but I think diversification over # loans is good enough. I don’t think the performance will vary over time as much as it depends on the site’s ability to properly assign an interest rate to the risk level of the applicant.

@whytax – Good point about liquidity, although I’m not sure how bad it would be. I suppose if it was really bad I’d just hold on. I think a lot of the secondary market buyers are investors from other states that aren’t allowed to invest in notes directly, so this is their only way to invest. Even in the depths of 2008/2009 there were people investing.

Great way to diversify any portfolio outside of stock, bonds and cash.

I too have started delving into Lending Club, albeit with a much smaller amount of capital. I’m really looking forward to your insights regarding this. So far it’s been a fun distraction from my normal investments, but I’m skeptical on how great of a return I’ll have. I think you’ve got it right sticking with mostly A and B rated borrowers. Those high interest rates on the lower grade ones are tempting but some of the loan applications are simply scary to read!

Jonathan,

Would you recommend Lending Club if one is saving money in a time frame of less than a year and needs access to it at the end of one year period?

The interest rate is alot better than ING direct but i am worried about the liquidity of the investment if i need the money to pay off a credit card in one year.

Just wanted to share my experience for those not started in P2P lending but contemplating. I did a little Prosper experiment about 4 years ago (therefore I have conclusions on everything). Started off with $500 then after 6 months of great success I took a $4K Prosper loan (5.5% as an AA). Things were rosy for 1 year but started turning downhill soon thereafter. I roughly made out with what I started. Here are the statistics of the 82 loans I made:

[Credit Grade]: #PIF #Discharged PIF%

AA: 7 2 78%

A: 14 9 61%

B: 16 9 64%

C: 10 8 56%

D: 2 1 67%

E: 2 0 100%

HR: 2 0 100%

I individually picked all 82 loans (yes – ouch); all were made in Dec 2007 to 2008. Here are my observations:

– When you consider that the lower grades have significantly higher %, I might be able to make the argument that I did better with those – although I haven’t done the calculations yet

– Of the 29 discharged, 14 were due to bankruptcy.

– I strongly suspect the “great recession” resulted in many of said bankruptcies. While the economy is better, there is still a significant amount of economic uncertainty what with the fiscal cliff, Europe, polarized Congress, etc.

By all means give Prosper a shot (since most of my prosper funds came from a loan, I didn’t actually front all that much money) but be warned that things could turn south quickly and you’re locked in for 3 years.

One other thing: I never found the best way to report these in taxes. To be safe I started with the painful way of each loan being an entry in my Schedule D, but it quickly turned to “Various” in (Date Acquired) 🙂

Hopefully this is informative to someone. I truly wish you the best of luck Jonathan. I’d love for you to find success which would help to heal the wounds of my slightly frustrating experience and reopen this avenue for consideration in my portfolio.

Just noticed in my previous post the tabs got lost in my table. Also just to clarify, “PIF” = “Paid in Full”, meaning I got the full amount of principal returned (although not necessarily interest, since several paid before full term).

I too am an investor in LC. I have found that you can invest too much… If you just invest in those loans that everyone else has already researched and are therefore at 90%+ funding and are only a few days away from funding you can do quite well…. even with the higher yield/higher risk loans. I am currently averaging a 19.1% return and my portfolio is mostly med/high risk on only 3 year loans…

My question is, does anybody out there have a good strategy for the money that’s just sitting there before it gets reinvested? Sometimes I find myself waiting for the scenario described above and wonder if I should temporarily withdraw the “cash available”, invest it somewhere else liquid, then reinvest it back on some sort of schedule… thoughts?

Thanks!

Has anyone noticed that Prosper charges 1% of outstanding loan balance, while LC charges 1% of each payment? This makes a big difference in your return, since quite few loans are paid off early.