Reminder: BRK Annual Meeting Live Webcast starts Saturday, April 30th at 10am Eastern. Always wanted to attend the Berkshire Hathaway Shareholder Meeting? This year, anyone can watch the Buffett and Munger Q&A session live without flying to Omaha, Nebraska. I don’t know if it will be available for later repeated viewing.

Charlie and I have finally decided to enter the 21st Century. Our annual meeting this year will be webcast worldwide in its entirety. To view the meeting, simply go to https://finance.yahoo.com/brklivestream at 9 a.m. Central Daylight Time on Saturday, April 30th. The Yahoo! webcast will begin with a half hour of interviews with managers, directors and shareholders. Then, at 9:30, Charlie and I will commence answering questions.

Rest of original post:

Berkshire Hathaway (BRK) released their 2015 Letter to Shareholders [pdf] over the weekend. As always, the letter is written in a straightforward and approachable fashion. Even if you aren’t interested in BRK stock at all, reading the letter can be educational for individual investors of any experience level.

I’m sure many people smarter than me will offer their responses to this letter, but here are my notes.

Berkshire share value. As usual, the letter addresses the different ways to value BRK shares. First, there is the market value, as seen on any BRK stock quote. Second, there is the book value, which is an accounting term defined as total assets minus intangible assets and liabilities. Third, there is the intrinsic value, which is what Buffett believes is the true value. Buffett has repeatedly stated that BRK will buy back shares if the market value drops to 120% of book value.

Over time, this asymmetrical accounting treatment (with which we agree) necessarily widens the gap between intrinsic value and book value. Today, the large – and growing – unrecorded gains at our “winners” make it clear that Berkshire’s intrinsic value far exceeds its book value. That’s why we would be delighted to repurchase our shares should they sell as low as 120% of book value. At that level, purchases would instantly and meaningfully increase per-share intrinsic value for Berkshire’s continuing shareholders.

This suggests that Buffett believes BRK is worth signficantly more than 1.20x book value. As I write this, the BRK stock is roughly 1.3x book, and it has dropped as low as 1.25x book in January 2016. As a (tiny) shareholder, I also use this as a rough measure of whether the company is under- or over-valued (or out-of-fashion vs. in-fashion). My holdings are mostly meant as a future educational tool for my children. I don’t know how BRK will perform as compared to the S&P 500, but it is great example of a money-making machine.

Individual stock holdings. As BRK has moved from mostly holding parts of public companies to holding entire private companies, there is less for the individual stock picker to sift through. For example, you and I can no longer buy shares of Precision Castparts or BNSF Railroad directly. He is still confident in his “Big Four” investments of American Express, Coca-Cola, IBM and Wells Fargo:

These four investees possess excellent businesses and are run by managers who are both talented and shareholder-oriented. Their returns on tangible equity range from excellent to staggering. At Berkshire, we much prefer owning a non-controlling but substantial portion of a wonderful company to owning 100% of a so-so business. It’s better to have a partial interest in the Hope Diamond than to own all of a rhinestone.

Even though the outlooks for AmEx and IBM is not as positive as they were few years ago, Buffett must still view them also as reliable money-making machines. Reading through this and older letters are a great way to learn about important concepts like earnings growth, dividend payouts, and share buybacks.

Optimism. A good portion of the letter was devoted to optimism about the American economy.

It’s an election year, and candidates can’t stop speaking about our country’s problems (which, of course, only they can solve). As a result of this negative drumbeat, many Americans now believe that their children will not live as well as they themselves do.

That view is dead wrong: The babies being born in America today are the luckiest crop in history.

Indeed, most of today’s children are doing well. All families in my upper middle-class neighborhood regularly enjoy a living standard better than that achieved by John D. Rockefeller Sr. at the time of my birth. His unparalleled fortune couldn’t buy what we now take for granted, whether the field is – to name just a few – transportation, entertainment, communication or medical services. Rockefeller certainly had power and fame; he could not, however, live as well as my neighbors now do.

Shareholder letters from 1977 to 2015 are available free to all on the Berkshire Hathaway website. You can also purchase all of the Shareholder letters from 1965 to 2014 for only $2.99 in Amazon Kindle format. Three bucks is a very reasonable price to have an official copy forever stored in electronic format. (Updated paperback will be re-stocked in mid-April for about $20. Don’t overpay for a stale physical copy.)

The 2014 Annual Letter discussed the power of owning shares of productive businesses (and not just bonds). The 2013 Annual Letter included Buffett’s Simple Investment Advice to Wife After His Death.

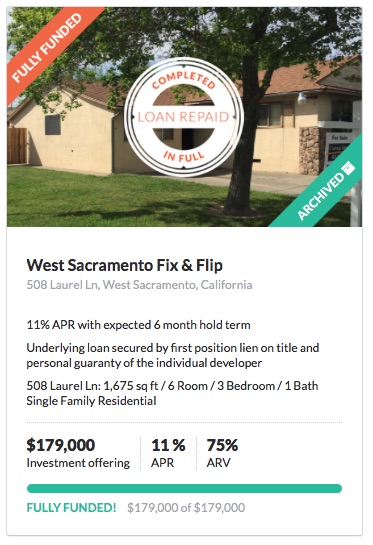

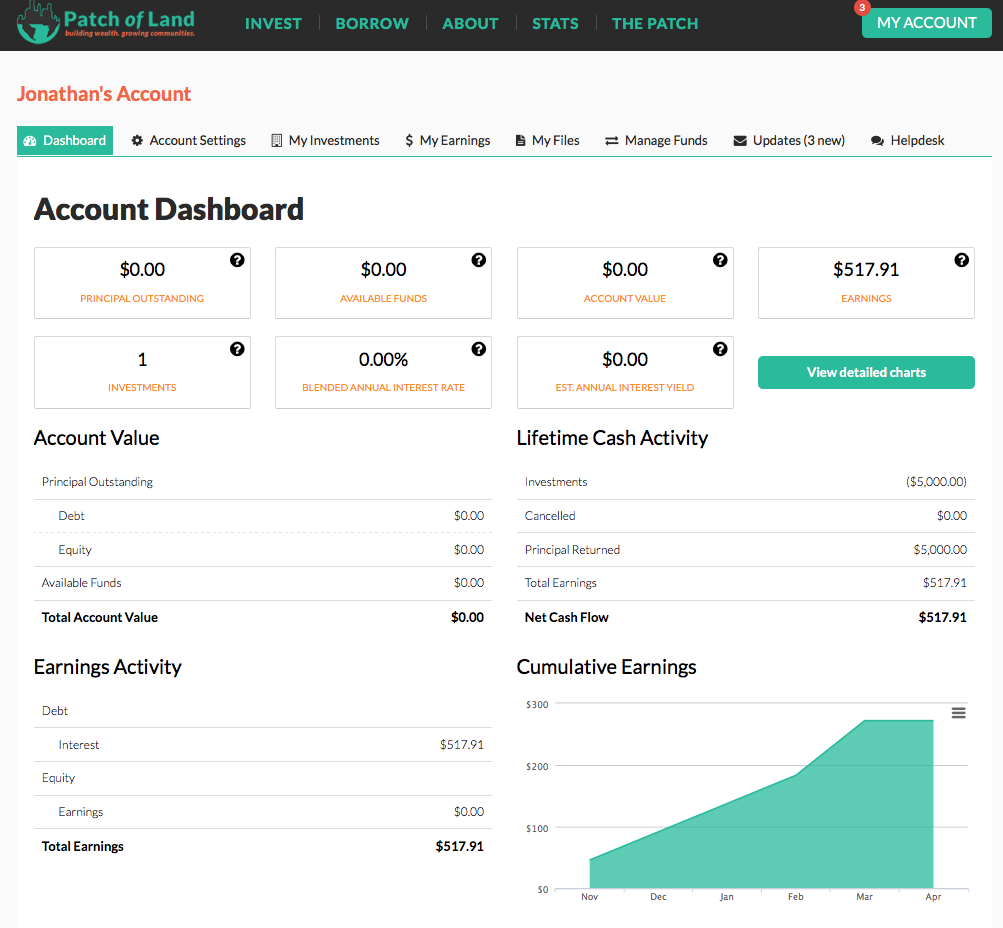

My first investment into real estate crowdfunding has completed. In April 2015, I invested $5,000 into a fix-and-flip loan at the site

My first investment into real estate crowdfunding has completed. In April 2015, I invested $5,000 into a fix-and-flip loan at the site

I like the idea of living off dividend and interest income. Who doesn’t? The problem is that you can’t just buy stocks with the absolute highest dividend yields and junk bonds with the highest interest rates without giving up something in return. There are many bad investments lurking out there for desperate retirees looking only at income. My goal is to generate reliable portfolio income by not reaching too far for yield.

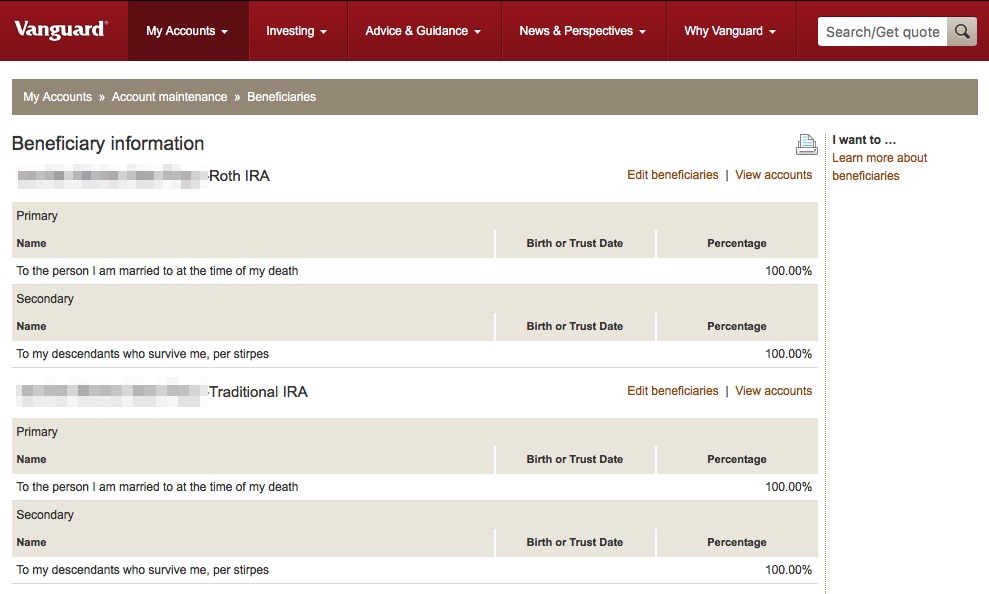

I like the idea of living off dividend and interest income. Who doesn’t? The problem is that you can’t just buy stocks with the absolute highest dividend yields and junk bonds with the highest interest rates without giving up something in return. There are many bad investments lurking out there for desperate retirees looking only at income. My goal is to generate reliable portfolio income by not reaching too far for yield. It has been a while, so here is a 2016 First Quarter update on my investment portfolio holdings. This includes tax-deferred accounts like 401ks, IRAs, and taxable brokerage holdings, but excludes things like our primary home and cash reserves (emergency fund). The purpose of this portfolio is to create enough income to cover household expenses.

It has been a while, so here is a 2016 First Quarter update on my investment portfolio holdings. This includes tax-deferred accounts like 401ks, IRAs, and taxable brokerage holdings, but excludes things like our primary home and cash reserves (emergency fund). The purpose of this portfolio is to create enough income to cover household expenses.

The Best Credit Card Bonus Offers – May 2024

The Best Credit Card Bonus Offers – May 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - May 2024

Best Interest Rates on Cash - May 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)