According to the stats, you probably funded your Individual Retirement Account (IRA) at the last moment this month (assuming you fund them at all). If we tend to procrastinate about saving, then we also probably put off estate planning. One of the simplest aspects of estate planning is to designate beneficiaries of your IRA.

I am not an estate-planning attorney, but here are some tidbits I picked up from various sources including a review copy of new book The Overtaxed Investor by Phil DeMuth.

Why is this important?

- The person, trust, charity, or estate that you pick as your beneficiary overrides any will. So if your sole IRA beneficiary is set up as your ex-spouse, and your will says everything goes to your current spouse, then your ex-spouse will still get your IRA (at least without a long legal battle).

- If you name an individual instead of an estate, the inheritor can space out withdrawals over their (actuarial) lifetimes, prolonging the tax-deferred growth benefits of IRAs. A trust or estate does not get this feature by default (a trust may be carefully constructed to preserve some of these characteristics).

- You may still want to pick a trust if you have sizable assets and are leaving them to young children. You can then outline rules and a trustee to manage how the money is spent. This route involves extra costs, however.

- Secondary beneficiaries can also be chosen. If no secondary beneficiaries are named, your assets may pass to your estate – exposing them to the probate process, estate expenses, and creditor claims. In many cases, people pick their spouses as primary and their children as secondary.

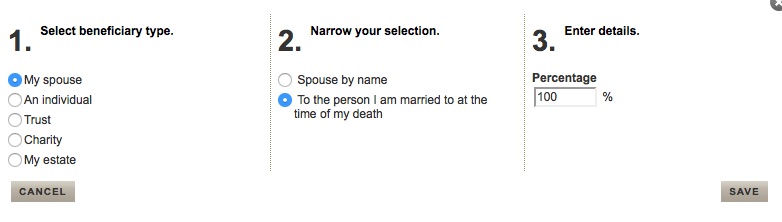

How should you do it?

- Contact your IRA custodian. I use Vanguard, and you can either fill out this paperwork kit or do it all online under Account Maintenance > Beneficiaries. They use some language to simplify the process. For example, I set my primary beneficiary as the “person I am married to at the time of my death” and my secondary beneficiary as “To my descendants who survive me, per stirpes”. I may change this later. Find out what per stirpes means and more with this Vanguard guide.

- Keep a physical copy in your personal files. Keep copes in your home safe, safety deposit box, and/or digital safe.

- Tell your beneficiaries where the form is and what is on it. Vanguard won’t contact anyone upon your death, so it is up to your beneficiaries to contact Vanguard. I suspect many other brokerages operate in a similar manner. There are millions of dollars in unclaimed IRAs every year.

Screenshots:

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

If you have multiple beneficiaries, please make sure you understand the designations Pro Rata and Per Stirpes – almost everyone has heard of Pro Rata, almost no one knows Per Stirpes (including most bankers who automatically check Pro Rata). Quick explanation: Pro Rata with multiple beneficiaries: if one of the beneficiaries dies before IRA owner, then IRA would be split between remaining living named beneficiaries at the death of the IRA owner. Per Stirpes with multiple beneficiaries: if one of the beneficiaries dies before IRA owner, then that person’s share of IRA (at owner’s death) will go to the named person’s family.

Good point, I had not heard of Per Stirpes before reading it in the mentioned book, and I like the way it works. I have chosen my secondary beneficiary designation as Per Stirpes.

Jonathan,

While I absolutely AGREE that folks should periodically review and update beneficiary designations, note that many states have revised their laws to automatically revoke beneficiary designations following divorce. In such cases, the courts use the legal fiction that the former spouse pre-deceased the account owner/decedent.

For example, my state (FL) adopted Section 732.703, Fla.Stat. in 2013, which provides in pertinent part as follows:

“A designation made by or on behalf of the decedent providing for the payment or transfer at death of an interest in an asset to or for the benefit of the decedent’s former spouse is void as of the time the decedent’s marriage was judicially dissolved or declared invalid by court order prior to the decedent’s death, if the designation was made prior to the dissolution or court order. The decedent’s interest in the asset shall pass as if the decedent’s former spouse predeceased the decedent.”

I encourage individuals to do their homework (as is a main theme of Jonathan’s site) and consult the particular laws of their home state. This quick summary is not intended to provide individualized legal advice.

Thanks for the tip. From the looks of it, too many people were forgetting to update their IRA beneficiaries and there were a lot of resulting legal fights!

I thought I had everything up to date and then looked at my newly opened Roth IRA. Oops, forgot to add the wife. Good reminder.

My dad had accounts through Vanguard. I saw one form from Vanguard that had a per stirpes designation to my children who survive me…along those lines. My dad was good at paying attention to his investments, but something happened and my brother took the Two accounts, Wellington and Admiral. I did see another correspondence letter from Vanguard confirming my brother as Primary Beneficiary 100% and Me as contingent. Vanguard sent my Dad letters in 2011,2014, that reflected the per stirpes designation and that stated that if he did not choose a secondary/contingent beneficiary and his primary beneficiaries died before him, that the funds would pass according to vanguards custodial agreement. When I spoke to Vanguard after my father passed they would not speak to me at all. It took two years for me to call again and this time they got a team on the phone to ask why i thought I was named as a primary and several more questions and then told me that my father never had a per stirpes designation. I have two children and my brother has no children. I read on Vanguards sight that if you name a primary beneficiary on one IRA account they give the other accounts to that person as well. Am I completely wrong?