Update May 2023: Rate tiers are now up to 4.50% APY. You may be grandfathered from the activity requirements until 6/30/23 if you were an existing user.

Older review, last updated October 2022:

HM Bradley announced several significant changes to their product (again). I’ve updated the review completely and removed all the historical changes as it was just getting too long.

HM Bradley (HMB) is a fintech software layer on top of a partner bank’s infrastructure. They are terminating their initial relationship with Hatch Bank at the end of October 2022 and changing completely over to New York Community Bank (NYCB). Existing HMB customers will need to open up a new account at NYCB before the end of October. HMB is also changing up their interest rate structure, but is offering a special intro offer to existing HMB customers. Detailed review below.

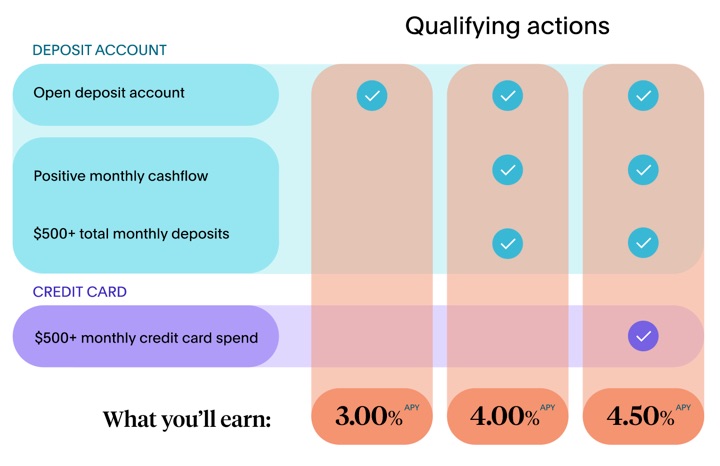

Rate tiers. Interest is earned on balances up to $250,000 with NYCB (up from $100,000 with Hatch Bank) and the rate you earn is set for the next month based on the current month’s activities. Here are the current rate tier and requirements:

- 1.00% APY. All customers who open an HMBradley Deposit Account with NYCB will be rewarded with 1.00% APY. No other requirements.

- 2.00% APY. Customers who make a direct deposit of at least $500 per month to their HMBradley Deposit Account with NYCB and maintain positive monthly cash flow (meaning that monthly deposits exceed monthly withdrawals, not including HMBradley Credit Card payments) will earn 2.00% APY in the following month.

- 3.00% APY. Customers who fulfill the 2.00% APY requirements AND also spend $500 per month on their HMBradley Credit Card will earn 3.00% APY in the following month.

Limited-time offer to switch for existing customers. HM Bradley is waiving some of the requirements for new customers that signed up to switch by 10/31/22:

Any customer who opens an HMBradley Deposit Account with New York Community Bank (NYCB) before November 1, 2022, will receive Level 2 Annual Percentage Yield (APY) until April 30, 2023.

Any customer who opens an HMBradley Deposit Account with NYCB and has an HMBradley Credit Card in good standing before November 1, 2022 will receive Level 3 APY on the balance of the HMBradley Deposit Account with NYCB until April 30, 2023.

You’ll have to start doing the requirements in April to get the higher rates in May 2023.

Requires a “real” direct deposit every month. You must receive some sort of direct deposit each month, as defined below:

For our accounts, we define direct deposits as those deposits made by the customer’s employer, a federal or state government agency, or retirement benefits administrator. These generally include payments made by corporations and other organizations. We do not consider deposits to an account that are made by an individual using online banking or other payment provider such as PayPal or Venmo as direct deposits. HMBradley shall make the final determination as to whether a deposit qualifies as a direct deposit for purposes of qualifying to earn interest.

Based on my experience, they do have a system for filtering incoming deposits, but it is not 100% accurate and your direct deposit may have to be reviewed manually. Their online account interface should clearly indicate whether you have made the required direct deposit for the current month. I had to contact them in order for them to manually check and mark the transfer as a direct deposit. Having it marked properly is required to get the top rate.

Positive monthly cash flow is based on ALL deposits and withdrawals (except HMB credit card spend). For the calculation of “positive monthly cash flow”, all deposits are considered including incoming transfers from another personal bank account. At the same time, your “spending” will also include any transfer out of your account, even if it’s just to another bank account that you own. They don’t count purchases made on your HMB credit card, which incentivizes you to use it – but conveniently they don’t care about your credit card spending habits as long as you’re using their card…

Basically, money has to keep coming into HMBradley and not go back out on a net basis every month. That’s a very unique requirement, but also hard to keep up forever. Even if you are a diligent saver, you will want to redirect some of those funds into other assets like stocks, ETFs, real estate, etc.

Credit card details. The HMBradley credit card is invite-only and partially based on their estimate of your income (which is in turn based on the size of your deposits, although you can attempt to self-report). Invitations are not guaranteed. You must opt in to their “One Click Credit” service which basically checks your TransUnion credit report so they can market stuff to you (soft inquiries). If your TransUnion credit file is frozen, they will not offer you an invite. But once you officially apply, you will have a hard inquiry.

Starting at the October 2022 monthly billing cycles, the HM Bradley credit card is basically a flat 1.5% cash back credit card with no annual fee. Prior to this, it used to be a more complicated 3/2/1% rewards card with tiered categories and a $60 annual fee (waived for first year). 2% cash back would have been nice, but now it’s just another vanilla mediocre rewards card.

Additional features. It’s still not exactly clear how other basic features will change with the new NYCB accounts. ATM rebate policy? Well, right now, they don’t even give you a debit card! This change seems a bit rushed.

Once you accept the new NYCB deposit account agreement and disclosures, we will ask you to agree to allow us to transfer your funds (including any funds in a Plan and accrued interest) from your deposit account at Hatch Bank to your new deposit account with New York Community Bank (NYCB). We will also provide you with your new account and bank routing numbers. You will want to use this information to change your direct deposit and recurring ACH transfers as soon as you can.

Unfortunately, we are unable to offer debit cards for new deposit accounts at this time. You will still be able to make ACH transfers, and we will let you know when a new debit card is available.

My thoughts. Interest rate changes are happening very quickly these days, and it is unknown how aggressively HM Bradley will keep up. If I didn’t already have an HMB account, I wouldn’t bother opening one up as the positive monthly cashflow requirement can get complicated if you save your money in different ways. I will be looking for them to raise their rates at least a bit more above the competition if I am going to keep jumping through that many hoops.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I am a bit confused.

Would you need to save a percentage from your direct deposit? Or from your pay?

Let’s say I get 1000 a week from work and am saving 75% in my 401k and 250 a week in direct deposit. I am also able to save 20% of that. Why do your 401k contributions count as you say and qualify me as a low/tier one saver?

I believe it’s probably just 20% of your direct deposit that you need to save, no?

Their savings rate is calculated based on all deposits and withdrawals into/out of the account.

I’m just saying that in general, most people are not going to both save a large percentage in their 401k and also 20% of their remaining take home pay. If you’re doing that, I would consider you a high saver! 🙂

Thanks Jonathan. Sorry for duplicate comment below. I agree that going through hoops for something that will probably be cut not worth it. Marcus, Purepoint, Simple…all cutting. Probably won’t chase these on line bank deals anymore. Seems like it’s dying.

I was lucky to open a add anytime 17 month cd at Navy in January for 2.25 with just $50 with plans to add to it after taxes were figured. Will probably just stick with that.

I am confused.

Let’s say I make 1000$ a week and save 75% of it in a 401k. My direct deposit is 250$ and I am able to save 25% of that.

That would qualify me for tier 1, correct? How do they know what I get paid. Surely it’s based off your direct deposit and not pre-tax amount? Why do you think I would be tier one/low saver. I understand this to mean 25% of your direct deposit saved. No?

So if I park, say, 25% of my bimonthly paycheck there, and then transfer up to a total of 100k,

Would that work? Could I transfer the 25% DD out monthly to maintain a balance of 100K?

Or would I have to DD the entire check?

They don’t say anything about size, they just require at least one direct deposit per month. The savings rate is determined by total deposits/withdrawals of any type.

I think you may have answered a question I have. If I made a minimal direct deposit each month, but transfer excess cash, the savings rate is based on both direct deposit and extra deposits vs withdrawals. Using it as a secondary savings account would be easy to get a >20% savings rate.

But yes, it would be more work than just getting a run-of-the-mill savings at a normal bank.

Yes, but remember that your savings account balance essentially always has to keep going up. If you take money out via transfer to external savings account, it counts as spending and thus will lower your savings rate for the next quarter.

So to be clear, for every $1000 you add to the account (whether by direct deposit or other incoming transfer), you could only use $800 of it for paying bills or external transfers out. For every $1000 that comes in, your balance at the end of the period needs to be $200 higher than before those funds came in.

Sounds like the way to game the system (err, make the most advantage of this offer) is if you have another checking account you use as a primary, but can split your direct deposit so only part of your paycheck goes into this account. Or for a dual income household, only one partner deposits their paychecks here.

Suppose you have $50k in cash you want to earn 3% on. Right now, you could open the account with just $1k, and direct $1k/mo of your paycheck into this account as a direct deposit. Closer to July 1, you could transfer more of the balance in. Then on an ongoing basis, you could transfer in $1000/mo and spend up to $800 of it, so you’re saving 20% of your $1000/mo but earning 3% on the whole $50k balance.

You can transfer more in the account at any time and earn 3% on that balance, but if you transfer a big chunk out to another account, you would lose your tier status for that quarter. In that way, it functions a little like a CD with a penalty. Although suppose you transferred out $10k of your $50k balance, that would cost you 3% for the whole quarter (or $375), where if you’re buying CDs you could buy them in $10k chunks. So this account is really designed to be your only/main savings account, and penalizes you for ever spending it. If you used this account to save up for a car, when you actually withdrew the money to pay for the car, your interest rate would plummet for that quarter.

Overall, not worth it to me.

I think you have it right. If you take out too much money during a certain quarter, you will get penalized for it the next quarter, like an interest time-out. But at least it wouldn’t be retroactive and you could just take out all/most of the money when you know a zero interest quarter is coming ahead.

Their rates just went up. 4.20% if you have their credit card and 3.60% if you don’t (but fund $500 a month). That’s pretty high APY even if you don’t have the card tbh. The APY and their plans feature are probably enough to keep me around even if they put requirements back and even if other banks up their rates.

The routing number for HMBradley for Direct Deposit is for RANCHO SANTA FE THRIFT & LOAN ASSN.

This doesnt match with the bank’s name, is that a concern?

What routing number are you using? Mine always shows up as Hatch Bank whenever I link to other banks like Ally.

Routing number is 322286188. Shows up as Hatch Bank (Head Office), 1001 W San Marcos Blvd, Ste 125, San Marcos, CA 92078 on ABA.com.

yes, I am using 322286188.

https://bank-code.net/routing-numbers/322286188-rancho-santa-fe-thrift-%26-loan-assn

ABA.com is the official site for ABA routing numbers, I would trust them with the correct updated info.

https://www.aba.com/about-us/routing-number

Rancho Santa Fe Thrift & Loan Association changed its name to Hatch Bank as of April 2019. Good to be skeptical though.

https://www.spglobal.com/marketintelligence/en/news-insights/trending/l1WvIpHLd8sIoVxOEGfoig2

Thanks, that makes sense. I will try what Brad F suggested above.

This sounds like a good deal in a declining interest rate environment, where by December it’s likely rates elsewhere will be even worse, and 1% will look quite good. If the top rate is at least 1% for Q1 2021, that’ll be even better relative to alternatives! (Grabbing the $500 bonus from Simple was my high water mark this year; how times have changed!)

If you have an Alliant CU account, it looks like you can’t link to your account. It doesn’t show up in the list of accounts. I don’t see any way to enter a routing # directly instead as is usually possible. I guess I’ll have to bounce funds through my Ally account. The FAQ provides no additional information about supplying a routing # and account # manually. It might not be possible.

They’ll supply a digital voided check, and even email your employer to help with a direct deposit, if you’d like.

This’ll be interesting.

I’m currently told: “You’re not earning interest this quarter.” I’ll have to fund and see if that changes for this quarter or not. It also says “Set up a direct deposit to be eligible for Savings Tier.” So that must be the magic required. So I’ll know by the end of this month.

Routing and account # are easily provided for direct deposit, no hunting around for it as in decades past.

Good luck!

Because of your article, I am interested in an HMBradley Bank NOW account. I sent a few questions to the bank and got the response quoted below back. I thought I would share because some of the information is different or was not in your article.

“ 1. We do not have a bill pay feature available at this time, but our development team is working on it

2. We do not have checks available

3. Inbound transfers that are originated from your HMBradley account are limited to $2,500 per day. There are no limits on transfers out of your HMBradley account. We also have no limits on incoming transfers originated from other institutions.

4. We do allow direct debits. These can be set up with your debit card, or set up with the account & routing numbers where the payment interface enables it.”

Your article says: “You can probably work around most things using the online Billpay feature.” Note that item 1 from the bank says currently no bill pay feature. However, because direct debits are allowed (item 4), then it appears that one could use a third party bill pay. For example, Bank of America allows you to specify multiple “pay from” accounts, including accounts at other banks.

Thank you for continuing to provide me with new ideas and products in your articles.

Thanks, I have updated the article to reflect that there is no online billpay. I just use it as a savings account, and have able to ACH push/pull initiated via Ally Bank with no apparent limits.

Have you withdrawn anty $$$ from the account yet? No issues?

Yes, I have withdrawn a smaller amount with no issues.

HMB also just got $18M in fresh venture capital:

https://techcrunch.com/2020/11/24/hmbradley-raises-18-25-million-planting-a-flag-as-las-entrant-into-the-challenger-bank-business/

Where’s the info about needing a high direct deposit to get the credit card? Data points on how high? I purposely have only a small DD going in since it’s a hassle to withdraw it, but it’d be worthwhile to briefly increase it on order to get up to 3.5%

Here are their terms: https://www.hmbradley.com/credit-card-terms

My only data point is that they told me my direct deposit “suggested” an income under about $36,000 which was too low to be considered for their credit card. Therefore, you would want to have a direct deposit total of probably at least $3,000 after tax to qualify for the credit card. There is no public application, you must wait until it shows up in your account, presumably after a month at least of having the minimum direct deposit.

FWIW, you have to spend at least $100/mo on the credit card in order to get the 0.5% boost.

Could you clarify the following:

1) Is it possible to transfer money into HMBradley in addition to direct deposit

2) Is the 3% interest only earned on the direct-deposited funds or on all funds(including those that you potentially transfer in via ACH)?

1) Yes

2) All funds

I had a virtual chat with this bank & said if I do the DD & deposit 100K if I would get 3% on

the whole wad. Nina said yes. Asked what about $ over 100K & she said nothing, zero.

Wishing I had opened an account 3/30/20 when they launched. Uncertain about now.

Hassle to move money & then rates drop. Never fails.

The FAQs say only $2500 a day can be added to the account. Nothing mentioned

re a wire transfer of a large sum. May return to the chat & ask.

I am also concerned about a rate drop, but they are experiencing explosive growth right now and also have lots of venture capital (see above link to article about $18m of new funding), so there is some hope that they will keep the rate attractive.

Should have opened account when you first mentioned it!

Appears I can wire in what I want.

Yes, you can also link via external bank and do ACH transfers without apparent limit.

The way I understood their email response was ACH limited to 2.5 K initially and can go up later.

I’ll take another look.

I believe that is the limit if you initiate from their end. If you initiate from an external bank, there is no limit. I have completed deposits significantly higher than $2,500.

Good to know!

Thanks so much.

When do we know what the rates will be for the next quarter? Are we sure they’ll be 3/2/1 now for Q1 of 2021?

Wait for it! The rates will drop & drop & drop. I have been chasing interest rates for years and it never fails. My hope is when HMB begins the descent, they will remain higher than others. Which I predict they will for a while & then not.

Are you saying HMB is dropping the rate 3/21? Any idea how low?

Opened and funded account the other day.

So they seem to update their rates quarterly; There’s no way to know in advance what it will be, but I don’t think it will be worse than elsewhere and quite possibly better. I’m moving more money over this week!

Yeah, my thoughts too

Doing a whole lot better in the stock market!

So obviously it’s too late to earn the top tier for Jan-March. But if I open an account, is anytime before the end of March good for the April-June quarter? If I open in March with one DD and no withdrawals would that put me in the top tier?

I don’t know, but they are easy to chat with. You can also request a phone call. They call immediately & are pleasant & helpful. I usually get someone named Meg.

I opened my account a few days ago. Let me know what she says.

Jon, why do you say the rate is 3% to 3/21? Have they indicated it will be dropped then?

I fully expect it will be soon.

I have dropped my cash savings to 250K and everything else is in stocks. I love QQQ. Up nearly 50% last year and going strong.

I wasn’t clear, I meant it is 3% guaranteed until March 2021.

Thanks!

Damn Fitness Bank dropped to .65%.

What gets me is they never notify depositors & I have to find out inadvertently

I created account but got tier 0. How do I reach to tier 3? If I do direct deposit, and save it for 3 months without any withdrawl, do I reach to tier 3 in next quarter?

“All customers that set up and receive a direct deposit at least once per calendar month will start in Savings Tier 3. You will remain in this Savings Tier until the next calendar quarter when we update the Savings Tiers for all customers. All new accounts with confirmed direct deposit will earn a tier no lower than Savings Tier 3 for the first full calendar quarter.”

Make a direct deposit and you’ll get Tier 3 right away (1% APY currently). The earliest you can get to Tier 1 (3% APY currently) if you join in February is April 1st, if you save 20% of your direct deposits.

thank you Jon

Does anyone know if you can set up a beneficiary or POD for this account?

Joint and POD are available. See the DEPOSIT ACCOUNT AGREEMENT AND DISCLOSURES at https://policies.hmbradley.com/deposit/v1.0.4/Deposit+Account+Agreement.pdf

Got it. Thank you so much abc for your post.

Update on POD. Even though it is in the agreement, I have been told by CS that they are not set up for it yet.

I wonder if CS gave me wrong information?

Has anyone out there added a POD to this account?

Just wondering because I do need a POD for my situation.

You can easily request a phone call with HMB

FYI – CS service can only be contacted thru Email or Chat.

Not the best system.

I know, but they have always called me back immediately vs. long holds.

I have chatted as well

I’ll accept this for the high interest rates

It might have been answered yet like to be clear.

if my direct deposit is $1000/month, so for 3 months = $3000.

And I transfer in $50,000 after 1st DD.

Is the 3% only for the DD Or entire balance $51,000 1st month, and $52,000 2nd month,…

It’s on the entire amount. I have close to 100K there

I wish they would let my husband open an account

But they are really being weird about it

Jenny,

How are you maximizing this account with your direct deposits and getting close to the $100k balance limit?

Are you doing minimal direct deposits (ex. less than $250)?

Are you doing any withdrawals or are you just letting the money sit there with minimal direct deposit amounts?

Frankly, I don’t care if I go over the $100k top a bit – getting that 3.5% on the first $100k is what I’m looking for…for just cash reserves not doing anything else.

You will not get the bump to 3.5% without using the CC for a minimum spend of $100 a month. This spend can be used against the 20% required savings. You need to have a minimum DD of $2500 to get the CC. I put a wad$$ into the account early on, so am rapidly approaching 100K. Not certain of future actions. If I lower the $2500 monthly DD to say $50, I’ll lose the 1/2% bump & drop to 3% on the $100K. However that half percent isn’t bad, given it’s on unlimited balances. I’m not about to fuss with numerous accounts that pay higher on low balances.

Need some clarification…

Just opened an account (6/27). The earliest I can have a direct deposit posted is around the 1st of August. What date will I start earning Tier 3 (1.00APY)?

If I understand correctly, I will not be able to earn Tier 1 (3.00APY) until the beginning of October. Is that correct?

When would be the best time to make a large deposit to at least earn 1.00APY?

Thanks for your reply’s.

I am not sure, but you can email, live chat or request a phone call.

They always call me within a few minutes, regular California banking hours.

If you get a referral you can get tier 3 starting with your first direct deposit. Let me know if you’d like a referral

Second that their chat people are very responsive and helpful

Hey Dan,

Do you still have any referrals left?

https://hmb.to/signup?code=0yBeBQa0

Thank you Dan, just got signed up!

Cliff,

Do you have any referrals?? I’m trying to start a new account . . .

Any invites available for HMBradley? Thanks.

Here is my referral link: https://hmb.to/signup?code=RUe7zGoX

Thanks for sharing!

Glad you were able to get one, sorry for the late reply.

Here’s my referral link

https://hmb.to/signup?code=6vyI0UzJ

Can someone share their referral link?

Not me, think it’s linked to my real ID which I don’t put out

Sorry!

What do you mean by your real ID?

Jenny s. is a social media kind of name

The link only has one’s first name and there is no way of figuring out anything other PII or account information from the link or after creating an account.

hmb.to/signup?code=CRTwZ3Mw

FYI, I just created my account and want to transfer money in from another bank. I saw an initial limit of $2,500. Elsewhere I see that check deposits have a limit of $2,500 per day and $10,000 per month. I asked customer support and got this helpful response:

>>>

Inbound transfers that are originated from your HMBradley account are limited to $2,500 per day (there is no monthly limit). We have no limits on incoming transfers originated from other institutions, so if you want to transfer more than $2,500 into your HMBradley account, you can always do so by originating the transfer from your other bank’s website.

Alternately, if at any point you would like to increase your transfer limit for inbound transfers on the HMBradley side, we can temporarily update that for you after your first direct deposit posts. Just contact us via email or chat on the day you would like to make the transfer, and provide the amount you would like your limit updated to. Any updates revert back to $2,500 after 1 business day.

Direct deposits do not count toward the total.

Outbound transfers that are originated from your HMBradley account are limited to $100 until the first direct deposit posts in the account. After your first direct deposit posts to your account, there is no limit on outbound transfers originated from your HMBradley account. There are also no limits on withdrawals initiated from an external account.

Thanks for sharing. I can confirm that I have linked with Ally and made several large ACH transfers in and out, with no issues at all. My direct deposit is a true payroll direct deposit.

Yeah, I have transferred big wads off money there, tens of thousands in one fell swoop, but need to tamp down DD soon, very close to 100k and looks like zero interest thereafter.

Anyone know if I can keep 3% with very low DD? Guessing the .5 from their CC will vanish without a 2.5 monthly DD?

Yes, I think you should be able to reduce your DD. I don’t see any restrictions on the size of the DD. I wouldn’t stress too much about it.. if you have $100k and then every month you deposit $1000 and withdraw $800, at the end of the year you’re at $102,400 and you’ve still gotten 3% or 3.5% interest on $100,000,

But still, they’re pretty responsive over chat or email if you want to ask them directly.

Thanks.

Does the posted interest amount each month count in conjunction with your direct deposit amount when calulating the 80% withdrawal?

atc1,

I don’t know, but I did notice that the microtransactions to confirm an external account DID count as withdrawals.

For example, if I deposited $5k and left it in.. and they deposited two small amounts that together totaled $1.00 and then withdrew them. They counted my savings rate as $5000/5001 = 99.98%.

I assume they would similarly count interest as a credit to your account, so if you start with $5k, earn $12.50 interest, deposit $100, you’d need to finish the month with $5000 + 20% ( $12.50 + $100) = $5022.50. In other words, you can withdraw up to 80% of your deposits and 80% of your interest.

My understanding is the DD amount doesn’t matter unless one wants the

Xtra 1/2 perfect from their CC to get 3.5%

I’m in Tier 1 and only have a $1 DD.

That was 1/2 PERCENT

I opened an account on Sep 10th with HMB, did a DD on Sep 15th and i am on track for Tier-1 APY for next qtr starting on Oct 1st. So if you want to quickly jump from the default tier-1 (1%) to tier-3 (3%), then open the a/c before Sep 30th and have at-least one DD.

“Based on $XXXX.XX in deposits and $YYY.YY in withdrawals your next Savings Tier would be Tier 1.

You have met your direct deposit requirement for September. Percentages update nightly. Your next tier will begin on October 1st.”

I’d love a referral, the ones above aren’t good anymore…

Referral! hmb.to/signup?code=VbqUTUpO

Thanks for sharing, Raymond 👍

Any referrals available? All of the above are no longer active.

I can provide one if you want: https://hmb.to/signup?code=2wS810y1

Any referrals available? Missed the one above

Any more referrals available? Missed the one above.

Does anyone have a referral to provide?

Thank-You in advance!

Thanks if you use my referral: https://hmb.to/signup?code=NuKJU0Mg

Thanks, Jonathan, for the initial review and now the opportunity to share the referral link here.

Thanks for generously sharing your referral link, Vladislav!

Disregard my request for a referral link – I rcvd a referral on another website!

Glad you got one, I removed your e-mail so you don’t get spam.

Ok…Now that I’m all set up with an account…what is the BEST way to maximize this account with up to $100k?

If I get the credit card and spend a minimum of $100 a month, I can get 3.5%

3.5% of $100k should be roughly $3,569 a year in interest?

The 20% savings a month/quarter seems to be the confusing part in maximizing the most amount of interest?

Should one fund this account with $95k and have a $250/month direct deposit and not pull anything out of it?

At some point, the balance with go above $100k – money over $100k won’t earn interest but that’s ok if you’re earning $3,500 a year in interest on the 1st $100k.

The issue becomes when you want to have a major withdrawal – say $10k withdrawal one time during a quarter. If I have nothing of a Direct Deposit going in ($250/month) and withdraw $10k, I’ll far exceed any savings percentage that quarter and will get dinged in interest?

Do I understand this correctly?

Has someone come up with a perfect formula to maximize this account for maximum interest payment?

I’ll go back and re-read everything but I didn’t see a full maximization plan listed (or did I)

Here is my strategy, I think I have this correct. Please correct me if not.

Add up your deposits and interest earned near the end of the quarter. Then withdraw 80% of the deposits and interest earned prior to the quarter ending in order to preserve your Tear One status. At the beginning of the next quarter, redeposit funds up to or close to the $100,000 limit. Repeat this process for each new quarter.

That is pretty much my basic strategy: The HMB interface does a pretty good job telling you exactly how many deposit have been made so far and your current savings rate. Interest counts as a new deposit. So if you want, you can sweep away up to 80% of all new deposits each quarter and still maintain the top tier. In addition, as mentioned, HMB credit card payments also reduce your balance without affecting your savings rate. This might still create a gradually increasing balance.

It’s true that with this model you can’t take out a huge chunk of money without losing tier status for one quarter (unless you have a Tier Rewind from back when they offered them for referrals). I don’t know of a way around that one, but that is one of the quirks of HMB. This is more of a bond replacement in my case, so I’m not looking to move it.

This bank and their website is somewhat of a joke…it needs a lot of work!

And here’s the best part of setting up an account – They’re asking me for a “Selfie” along with a copy of my drivers license, Passport, or other form of official ID.

So, I never sent them a “Selfie”, or copy of my drivers license, passport, etc. As a matter of fact, I contacted them via chat and questioned why they let my spouse sign up for an account but then when he added me as a spouse to the account a s a joint holder, that they required a selfie pic, etc. I also questioned them, as if they were only doing it to women – and wasn’t that kind of sexist on their part…and what were they doing with all the selfie pics of women!

Anyways, I forgot about it…..and low and behold, they added me as a joint holder on the account anyway, without the selfie, pics of id’s, etc…

Glad they did that but geez!

Thanks for the review. I signed up close to a year ago and have been really happy w/ the rates. It’s good for emergency fund storage.

Here’s a referral if anyone needs one.

https://hmb.to/signup?code=rg9hzO9X

Thank you for taking the time to share your referral and helping out some readers!

Thanks for this review and all the great content, Jonathan!

I too have been using my HMB account for about a year as a place to stash emergency funds and transfer out 80% at the end of the quarter, then transfer it back in to maximize the interest earned.

Referral code for MMB readers 🙂

https://hmb.to/signup?code=LW402myd

what kinda money amount are you talking about and transferring in at the end of the quarter and transferring back in the next month. Is this a great strategy to maximize?

I’m trying to see if anyone has come up with the best possibly strategy (hack as the kids say today) to maximize the most in interest earned on this account.

I don’t know if I should start out at $90k or even higher…and then what are the right amounts to pull out, etc…again, to maximize interest earned at either the 3% or 3.5% levels. The 3.5% strategy requires a bit more work, to get around the credit card portion of spending.

Looks like the interest rate party is over.

New rates coming and it doesn’t look good upon 1st look

Currently you can get 3% without the card, or 3.5% with it.

Starting Feb 1 2022, you can get only 1% without the card, 3% with it.

So it really only pays if you get the card.

The card is free for one year, and then $60/yr. The interest easily pays for that, assuming an average tier 1 balance of at least $3,000 and that you couldn’t get more than 1% somewhere else.

You also need $2500/mo in direct deposits and to spend $100/mo on the card. New cardholders must apply for the card by Dec 31.

Of course, more hoops to jump through makes me more likely to consider other investments. (Don’t forget the required 20% savings rate.. if you have to withdraw a chunk of money, you’re essentially earning 0 for the quarter, and that extra credit card you’re carrying isn’t worth it.)

I’m having trouble understanding their long assed email. Are they saying top tier with the cc is 3%?

Are they still saying a $100 spend per month on the cc? And $2500 DD each month with 20% saved?

Rapidly approaching 100K. What can I do then?

New additional terms next year…In order to receive 3% APY, you must have a monthly direct deposit of at least $2,500 AND have at least $100.00 in purchases during the monthly billing cycle on their credit card ($60.00 annual fee, waived the 1st yer)

I hate to commit to a new card and $100/month in spending, only for the terms to change yet again in the near future. If I knew everything else was locked in for a year, I’d do it.

But given the rapidity of changes, I think this might be the end of the line for me.

I think it’s fair to worry about future changes, but I think we should give some credit to HM Bradley for keeping the 3% APY rate for over a year and a half. That’s over 18 months without any changes at all. They will pay me over $3,000 in interest for 2021. The same balance would have only earned $500 at 0.50% APY, a difference of $2,500.

I do agree that at lower balances, the hassle of applying for and maintaining the credit card requirement may not be worth it. However, I was willing to do it for an extra 0.50% APY before, so I am still willing to do it for an extra 2% APY.

I went through a similar calculus, but wasn’t paying enough attention and missed the rewards part of the credit card. With the rewards, the 50 basis point increase was more attractive than I thought. But that’s in the past, now.

In any case, depending on income, time horizon, tax rate, and required effort, I could see an extra 200 basis points on 100k not necessarily being worth the effort. It all depends, I suppose, on what is considered worthwhile and what is considered a rounding error.

I still think, even with the card and 2500 monthly deposit, it makes sense. The question might be when a balance greater than 100k getting zero interest becomes an issue, because you’re net saving at least 20% of 2500 every month. (That’s 104,800 at year one, 109,600 year two, ect.) But with a spend greater than or equal 500 a month on the card, you can keep it right around 100k in perpetuity. (Ignoring monthly interest.)

I’m still amazed even this is possible; Is HMBradley funding this with investor money, like Uber subsidized rides in the beginning? It’s hard to believe this is profitable, yet, as a business.

Thanks, I have added some commentary at the top of the post about these 2022 changes.

“AND have a least $2,500 in monthly direct deposits for each month of the previous quarter” but makes you wonder what happens for those of us with a $100 DD every month? We’re out of luck for Q1 of next year for 3%, even with their card?

Good question, this scenario is addressed at the very bottom of the page:

Sadly, I don’t have the card. I won’t know about an offer for a month it looks like. Just enabled the new insights feature and got this: “Your credit invitations will update on January 16, 2022”

Oh well.

The Fed just committed to rate increases next year, so there will probably more opportunities in the coming year than just HMBradley. We’ll see. From the AP today:

“The Fed’s new forecast that it will raise its benchmark short-term rate three times next year is up from just one rate hike it had projected in September. The Fed’s key rate, now pinned near zero, influences many consumer and business loans, including for mortgages, credit cards and auto loans.”

Interesting, my wife has an account w/o a credit card, and it says that hers will update on December 17th.

Looks like I was too impatient. Got the offer email today anyway!

Nice 👍

Really self-destructive timing by HM Bradley, the same day as Fed clarity about rising interest rates — and the punishment to loyal customers is way too drastic. Their assumption that they’d hook customers with a bait-and-switch launch promotion (albeit, the one-year long game) was naive given the fluidity of online banking these days. I’ll just put my money elsewhere now. After all, their business model also tried to keep captive our money with a 20% withdrawal limit past a maximum amount I’d reached, so I’m itching to pull out funds that increasingly earned no interest at all from them.

By the end, I’ve made a few extra hundred bucks by going with them while they made sense; but a few hundred bucks is smaller than the value of my time needing to find and manage my account at a new high-interest bank…

With the new savings tiers promotion, i assume the 3x will not have any restriction of $100k i assume, unlike how it is currently structured. I didn’t see that anywhere mentioned. Please correct me if i am wrong.

“We do not pay interest on account balances above $100,000.”

https://www.hmbradley.com/apys

Anyone have thoughts on some strategies I am considering? I Just got approved for the credit card and can manage the 2500 monthly DD. I want to use the account to park maybe 30-40K. If I can keep the 3%, the interest will cover the CC annual fee (first 12 month waived anyway).

Assuming quarterly deposits of 7500 (2500 DD x3), should I leave it in there the full quarter then move out 80% of it to my regular hub account at Ally at end of quarter? With this method, the HMB account balance will grow at ~500/month.

I could also (I think) set up Plastiq to pay my mortgage with the HMB CC. Mortgage is about 2500, Plastiq charges a fee around 3% which would be offset by the HMB 3% cashback on biggest category. So it would be a wash in terms of CC points or cashback, but it would let me keep the HMB savings account balance pretty much flat since CC spending doesn’t count as a withdrawal. Main downside I see is it’s one more middle man, and it’s a manual process that I would need to pay my mortgage each month manually via Plastiq as opposed to the current automatic draft from my Ally account.

Any other ideas?

So interestingly, when I accepted my offer for the card, there wasn’t any “credit questions” game, which was interesting. Usually I have to go through the usual what was your address 13 years ago game. The disclosures I read included my credit score from Experian as well; Not sure if this is the actual “score” or one of those derivations that you see for free all the time. I haven’t looked to see if this was a hard pull yet, but usually I get an email if it is. ymmv

Happy holidays!

Received a game changer?? email today from HMB.

Says nothing about it if you already have the credit card with the savings account.

Waiving of requirements to qualify >> now until Dec. 31.

Seems too good to be true.

First year the credit card is free then $60 a year.

What say you??

“Now through the end of the year, we are waiving some of the typical Savings Tier Boost Promotion requirements. Simply accept your personalized Credit Invitation you may qualify for by December 31, 2021 to earn a Savings Tier Boost on the APY associated with your Savings Tier in the first quarter of 2022.

We will be waiving the following requirements for customers who accept a new HMBradley Credit Card invitation through December 31, 2021:

Receive $2,500 in direct deposits each month to your HMBradley Deposit Account; and

Spend $100 per statement cycle on the HMBradley Credit Card.

You still need to qualify for a Savings Tier to be eligible for the Savings Tier Boost Promotion in the first quarter of 2022.”

I’m interested in an HMBradley referral/invite if anyone has one to spare.

https://hmb.to/signup?code=neYDvdr7

You mention that the credit card spend does not count towards the 20% savings requirement. Is there a way to pay your credit card bill with funds from the savings account?

Yes. In fact, I just did that today for the first time. You can pay your credit card from your savings account, and it does not count as a withdrawal when calculating your savings boost. Nifty feature to get you to use your card more.

I also like that it shows you running totals of your top spending categories, and assigns 3% to your top one, and 2% to your next one. Presumably that is calculated for good at the end of the month, and then re-calculated next month?

However, a couple minor complaints I have on the credit card:

Once you’ve paid the bill, you can’t dispute a charge. Something odd I noticed in the terms of service.

You can’t change the billing date (I just asked their support and was shot down.)

Does anyone have a referral code to share? Thank you!

Using HMBradley Credit Card to pay TAX (payUSATax.com) it showed a “NON_REWARDING Category). HMBradley Rep says the payment won’t receive Reward.

Anyone aware the NON-REWARDING Category? What other payments are in such Category? (Rep there not able to clariy)

Please help, thanks.

Hi Jonnathan – Thanks for your website and posts. Helped me a great deal.

Using HMBradley Credit Card to pay TAX (payUSATax.com) it showed a “NON_REWARDING Category). HMBradley Rep says the payment won’t receive Reward.

Anyone aware the NON-REWARDING Category? What other payments are in such Category? (Rep there not able to clariy)

Please help, thanks.

From E-mail rcvd from HM Bradley today.

Thanks to the feedback we received from our credit card customers, we’ll be making some changes to our credit card agreement and rewards program.

Here’s what’s changing:

No annual fee

Beginning August 12, 2022, the HMBradley Credit Card1 will not have an annual fee. If you paid an annual fee in 2022, HMBradley will credit your credit card balance for $60. Please review the updated Credit Card Account Agreement here.

1.5% Cashback

Starting October 16, 2022, you’ll start earning a flat 1.5% cash back rewards rate on all eligible purchases.2

What’s not changing?

There are still no limits on the amount of cashback you can earn.2 And, the HMBradley Credit Card remains an amazing everyday card that puts your money to work – even when you’re spending it.

We value each of our customers, and we are so grateful for your continued support. We’re here to answer any questions you have – you can always reach out to us

This is AWESOME!!!!

I was kind of disappointed, but it makes life easier. Now I can use my Bank of America Customized Cash Rewards card all the time and not think about it, and keep using my Chase Ink card for gas and restaurants, as always.

I do wonder what’s gonna happen when a 3% savings rate is the norm; Does HMB raise rates, or will that be the end of this? Either way, it’s been a profitable ride!

It was good while it lasted…

The annual percentage yields (APYs) associated with the Savings Tiers on all deposit accounts at Hatch Bank will be 0.01% on 10/14/22. Deposit accounts at Hatch Bank will be closed after October 31, 2022. Earn up to 3.00% APY1 by opening a deposit account with our new sponsor bank, New York Community Bank (NYCB).

HMBradley is now dead. The interest rates have killed them I guess. You gotta move your money to a new deposit account with them, opening a brand new account, or it’s done. I’d just bail at this point, so many other choices.

“Hatch Bank will automatically close all deposit accounts at Hatch Bank after October 31, 2022, unless you:

Open a new HMBradley Deposit Account with NYCB, transfer your available balance to your new account, and close your deposit account at Hatch Bank, or

Close your deposit account at Hatch Bank and direct them where to send any funds on deposit by October 31, 2022.”

I smelled trouble as soon as they announced the dramatic shift to effectively extorting the opening of a new credit card, and bailed immediately. I don’t think they got sunk by interest payouts — rather, that credit card greed undermined their credibility and lost too many customers.

I’m really reading this differently.

I see 3% on up to $250K now, with different hoops.

Yeah, but I’m seeing until 1/1/23 on the 3%

You seeing the same DD & CC spend? idk

Wouldn’t it be better to just get a 2.7% with Bask Bank , rather than wasting time in another potentially short lived interest account?

I’m struggling with their email I got today. Think they are saying HMB is on life support & we have to open accounts at NYCB bank. Seems they, NYCB, are offering a promo interest rate of 2-3% until 1/23. I don’t know what lays beyond. Appears HMB will return your ??? to you, if you don’t open at NYCB & transfer .

Basically this.

Because we have no idea what is coming, why go through the hassle of opening a new account when for example Elements offers 3.25% today, and is also a new account open. Or SoFi is up to 2.5% now I believe, and they’re raising aggressively.

I’ve been planning on bailing into 4 week Treasuries as soon as rates are competitive, so I expected to move anyway soon. Just didn’t expect to get this dumped on me with 15 days to avoid losing interest income payments!

This is a fairly typical “fire sale” business arrangement where an existing company buys off a failing brand name solely for capturing new business from the customer databsae — doesn’t change the fact that HMB failed and is not offering any value to existing customers.

So the smart move is to ignore HM Bradley’s offer (which is really NYCB’s offer) and just directly apply for an account with NYCB. Another interesting quirk is that NYCB has a high-interest-rate “hidden” portal for signing up, and their mainline NYCB portal with suspiciously lower payouts.

Would you instruct HMB to send the funds to NYCB or have this bank pull the funds? I’m going to shop around to see what a bank I heard of has to offer. I’ve gotten nothing but crap from HMB over the last few years. Just yesterday chatted with 2 reps, because I was unable to transfer 80% of DD. Never straightened it out. Never mentioned bank going under.

You guys all went to the “learn more” page?

https://www.hmbradley.com/blog/a-new-chapter

HMB was never a bank. They were a layer on top of Hatch. Now they’re swapping Hatch out for NYCB, and making other changes also. I don’t see this as being as dire as everyone else.

From https://www.hmbradley.com/blog/a-new-chapter

This is what you want to know, so let’s get into it:

* Customers who open an HMBradley Deposit Account with NYCB will be rewarded with 1.00% APY just for signing up. There’s no need for a monthly direct deposit or requirement to save any deposits.

* Customers who make a direct deposit of at least $500 per month to their HMBradley Deposit Account with NYCB and maintain positive monthly cash flow (meaning that monthly deposits exceed monthly withdrawals, not including HMBradley Credit Card payments) will earn 2.00% APY in the following month.

* Customers who fulfill the requirements in the previous bullet point and also spend $500 per month on their HMBradley Credit Card will earn 3.00% APY in the following month.

So, to stay at 3% you must have direct deposit of $500/month, spend $500/month on the credit card, and have deposits greater than withdrawals (doesn’t mention any particular % req’d).

I’ve been on the fence about keeping my account since I don’t like the required CC spend. Now with that going up and other savings accounts above 2% with no hoops, I’m out.

Looks like instead of sending this blog post, they sent an alarming email instead: https://www.hmbradley.com/blog/a-new-chapter

Oops.

So they aren’t dead. But the card spend goes up: “Customers who fulfill the requirements in the previous bullet point and also spend $500 per month on their HMBradley Credit Card will earn 3.00% APY in the following month.”

Definitely bailing now.

Look at HMBradley’s history just in the past year or so. They have changed so many requirements mid-stream.

I qualified for Tier 1 (3% APY) for the 4th quarter. Now they are not honoring that either.

Be sure and wait until your earned interest gets posted (hopefully on October 1st.) before moving your money out of Hatch Bank.

Redeem your credit card rebates when available.

They screwed me bigtime and dropped my rate from 3 to 1 for no discernible reason. It was supposed to return to 3 on 10/1. So much for that. What CC rebates do you mean?

I’m seeing several big banks offering 2.25%, & a few a bit more. Will not go to NYCB. Any friend of HMB is not a friend of mine. They seriously made up shit as they went along & reversed course.

Thanks for that reminder. I just redeemed $65 of credit card cashback to my HMB deposit account and it says it’ll take up to 5 days. I certainly wouldn’t want to change that underlying account before that (or this month’s interest) hits.

Yeah, they’ve been changing things around, but I don’t see this as HMB failing. HMB is just the layer on top. I see it as Hatch Bank failing and NYCB coming in and taking their place. My experience shouldn’t change. My relationship was with HMB, not Hatch. (Except that I have to update my direct deposit bank acct info as I’ll have a new account # / routing #.)

I joined CIT bank back in Dec 2018 when they were offering over 2%. As interest rates dropped, they fell down to under 0.5% and I switched to HMB in Oct 2021. I was initially getting 3.5% and now just 3%, but it still beats the alternatives.

As for their new rate changes, I like:

Monthly updates: If you make a big withdrawal, it only lowers your rate for that month, not an entire quarter.

Simplified savings: You don’t have to save 20% of your deposits, even 0.01% will do.

The direct deposit requirement doesn’t bother me, but I don’t like the $500 monthly credit card minimum. I just switched my insurance payment over to that credit card (and it’s nice to get 3% reward on that expense) but that’s under $500 so I’ll have to use it on some other expenses each month, too (at 1-2% cashback). If I get tired of that hassle, SoFi at 2.5% (up from 2.0% a month ago) seems good.

>and it’s nice to get 3% reward on that expense

Didn’t they move away from this to a blanket 1.5% back on all purchases recently? The CC spend is the big hurdle for me, I just prefer to use my other reward cards more.

> Didn’t they move away from this to a blanket 1.5% back on all purchases recently?

No, check out their rewards terms here. It still mentions a top category of 3%. https://www.hmbradley.com/credit-card-terms

I am unfamiliar with the CC cash rewards. I assumed the 1.5% would go to the CC statement. I have been unable to log onto HBM, on multiple iPads & the laptop. With and without app. Wanted to grab 80% of the DD. Chatted with 2 customer reps, both claiming to be in training. Neither could help & one said “engineering” would email. Nothing

I am trying to see how to make a comment here and rather than replying. Can someone please help? Thanks. I have this new thing with HMB all figured out now.

I am not thrilled by the CC spend either. I get 5% back on cards linked to Walmart, Lowes and Amazon. But the 3% total interest on my >100K makes it very worthwhile to use their CC.

I believe the credit card cash back rebate has been reduced to a flat 1.5%.

Do you guys know how much the NYCB DD would be? Are the higher interest rates capped at 100K?

The new direct deposit required is just $500/mo. The cap was raised to $250k.

See details at https://www.hmbradley.com/blog/a-new-chapter

Ok, will try new post here. I found good info at the HMB URL, far superior to the confusing email they sent today. I will be making the transfer to NYCB. Appears it will be a simple process from their site, HMB. Biggest advantage for me is the ability to earn 3% on > 100K. I have been > for several months. No problem with the $500 DD. Not 100% yet, but appears I could withdraw $499 which I may not. Terrible year on Wall Street. Remaining requirement is a $500 CC spend. So, 1% to open the account. 2% if DD added. 3% with CC spend. Not bad. And rate lowered on monthly rate vs quarterly.

Hi jenny,

Have you considered Elements Financial CU? 3.25% guaranteed 12 months and no DD or spending required

No, never heard of them, but will def take a look. Thanks

I believe the credit card cash back rebate has been reduced to a flat 1.5%.

Yes, they confirmed that in a chat a few weeks back. But that was HMB. Is NYCB doing the same?

Have you seen dollarsavingsbank at 3.01%…no hoops that I see.

Apparently you mean https://www.dollarsavingsdirect.com, a division of Emigrant Bank. Interesting.

The main “catch” with DollarSavingsDirect is that they don’t allow ACH transfers to be initiated by outside banks, at all. You can only transfer to linked banks in their internal system and within their set limits (which they can of course change). That is a no go for me. Especially when I can get 3.25% guaranteed for a year from Elements Financial if I really wanted to open another account right now.

https://www.mymoneyblog.com/elements-financial-savings-promo.html

But Elements has crazy low ACH limit. This doesn’t seem to be much of an improvement. I asked the question two ways, and their support said their ACH limits apply to transfers initiated either from Elements or at another bank.

Hmm… that’s in conflict with what I’ve read about Elements. My understanding is that Elements has low limits for internally-initiated transfer (as do many places), but no limits on externally-initiated ACH transfers.

I asked:

“Hi,

To clarify, this is the case even if I got into (for example) US Bank and schedule an ACH transfer to an account at Elements, without ever logging into or otherwise interacting with my Elements account?

Thanks!”

They said: “Yes, we will reject the ACH if it is over the limit. ”

Maybe what I asked is not the correct way to phrase this. I can’t say. And I found nothing in their FAQ that makes any distinction between initiated at Elements and initiated outside Elements with regards to ACH limits, which is why I originally emailed them.

I appreciate the data point and I don’t doubt that a rep did say that, but I am still skeptical because I’ve read lots of posts from forums and comments from sites like DepositAccount and DoctorofCredit including the ones from past years (they’ve done this 1 year guarantee thing before) and none of them indicated a block of external ACH (while they did confirm the DollarSavingsDirect blocks). It just seems like if they did really block external ACH there would be more ongoing reports as Elements CU has been around for a while.

I just opened an Elements Helium acct this afternoon and initiated a large transfer from Ally. I’ll let you know later this week if it goes through.

As promised…

10/3 opened Elements acct

10/3 initiated 60k transfer from Ally to Elements (using Ally website) – Ally states will take 3 days.

10/4 Ally shows request being processed.

10/6 Transfer arrives in Elements account.

ACH initiated from Elements has very low limit. Had to initiate from Bask

Thanks for sharing, glad to have more confirmation that externally-initiated transfers are allowed.

Jonathan, are you transferring from HMB to NYCB?

Yes, already done. Simple process, took 2 minutes. HMB has paid me over $6,000 in interest (100k at 3% APY for 2 years when interest rates were much much lower) as was promised, so I’ll give them them a chance and see what happens.

I was fully prepared to make the transfer from HBM to NYCB, especially since Jonathan did it, but now my buddy sent an email about 6 month T Bills currently paying 3.78% and expected to rise. I know nothing about bonds, other than the I Bonds capped at 10K that are paying tremendous interest rates now. I got two, one for myself and another for the husband. Guess I have to hold off on the bank transfer and look into these bonds. Certainly no need to use the 102K parked at HBM anytime soon.

Actually it is Dollar Savings Direct.

Thanks for the updated post, Jonathan! The $500 credit card spend at 1.5% is a bit annoying… at 3% for one category it was easier to swallow.

Though to look at the full picture:

The decreased credit card reward of 1.5% compared to a 3% reward from HMB or where you might get elsewhere) costs you $90/yr on $500/mo spending.

The increased return on savings of 3% vs 2.5% at SoFi would save you $90/yr on $18,000 account balance…. for greater account balances, you still end up ahead by jumping through these hoops.

*Neglecting taxes… I believe bank interest is taxed, but credit card rewards are not.

I think I’m with you.. since I have an existing account, I’ll keep it through the end of the year. (As I understand it, they’re waving the $500 monthly spend for current customers for the next few months?) After that, I’ll re-evaluate.

I see that CIT is back up to 2.7%. I dropped them when they went down to 0.45%.

I’m doing the same as you.

I switched to NYCB, for now – NYCB is offering us (credit card holders), 3% interest on our savings through Jan 31, 2023…and on top of that, 3% interest up to $250k (vs. $100k before)…and with NOTHING to do until then, no credit card spend, no direct deposit, no savings tiers, etc…Nothing for 4 months of 3% interest, up to $250k.

So, not only am I staying with HM Bradley, and switching to NYCB…I’m adding more money in to take advantage of the additional higher limit earning 3%.

I’m following here and also Reddit, looking for other future options…but for now, I’m good!

Bottom Line, if your sitting on the fence, make the switch…you have nothing really to lose other than interest on your HM Bradley/Hatch Bank account that dropped this weekend to .01%.

Note: some on Reddit are upset there’s not an immediate Debit card for switching…frankly, I would NOT tied a debit card with this account – as you do not get the same protections with a debit card that you do with a credit card. HM Bradley is not an everyday bank for me…it’s only a place for somewhat liquid money to earn as much as possible without being risked in the stock market.

RE:

“Customers who open an HMBradley Deposit Account with NYCB by October 31, 2022 may be eligible to earn either 3.00% or 2.00% APY until January 31, 2023. The direct deposit, positive cash flow, and credit card spend requirements, as applicable, are waived for these customers through December 31, 2022.”

Why are folks saying you’ll earn 3% APY through the end of January, 2023 without jumping through hoops?

Because, if you don’t do anything (jump through hoops), you’ll earn 3% interest thought Jan 31, 2023 according to their write up —-> https://www.hmbradley.com/blog/a-new-chapter

“We are working hard to make this transition as seamless as possible. Customers who open an HMBradley Deposit Account with NYCB by October 31, 2022 may be eligible to earn either 3.00% or 2.00% APY until January 31, 2023. The direct deposit, positive cash flow, and credit card spend requirements, as applicable, are waived for these customers through December 31, 2022.”

The Hoop jumping does start in January to be eligible for continued 3.00% interest in February 2023.

“In order to qualify for one of the higher APYs in February 2023 and thereafter, the direct deposit, positive cash flow, and the credit card spend requirements, as applicable, must be met in January 2023.”

But, if you don’t do any hoop jumping (ex. spend $500 on the credit card in Jan or set up Direct Deposits), you’ll still earn 3.00% interest through Jan 31, 2023. Come Feb, you’ll be looking for a new bank or setting up those hoops jumps in Jan to keep earning the higher interest rates.

I’ve been with HM Bradley for a while, but moving to Elements Financial, which pays 3.25% for the first year with no hoops or 4% for the first year (up to $20k) on a rewards checking account with hoops.

I guess the seed money started to run dry for HM Bradley.

SoFi just hit 3% with direct deposit. No other hoops. I think HMBradley is done if they don’t raise their rates soon. I’m probably going to move over from LFCU for next month, as they’re stuck at 2.02% for the rest of the year. Previously that was a decent rate.

Ah, I just rcvd 3% interest (on up to $250k) at HM Bradley (using New York Community Bank) for the month of Oct. In addition, I will receive this 3% rate for Nov, Dec, and Jan without having to do a thing.

What 2.02% are you talking about??? Not HM Bradley/NYCB…

With the Fed raising interest rates again…I would hope that other banks & FinTech’s will soon be upping their deposit rates (hopefully above 3%) in the next few weeks/months. If they do, and HM Bradley is still at 3%, I’ll consider moving my accounts. I’ll park my liquid cash reserves at any financial institution that pays the highest rates with the least amount of hoops to jump. As of right now, there are NO hoops to jump through at HM Bradely, if you moved your money to their NYCB product.

Now, come Jan (into Feb), there will be additional hoops to jump through (as indicated in the updated terms( but they should be easy to meet for most.

CF,

SoFi has much easier hoops to jump through (just direct deposit) than HMB after January. Currently they’re both at 3%. Actually, CapitalOne’s “360 Performance” account is also at 3% with no DD required. So unless HMB raises their rate, I see no reason to jump through their hoops after January. They’ve got a few months to get more competitive.

The 2.02% he referenced was at LFCU.

… and there you go. HMBradley is now offering 4% if you jump through their hoops.

I imagine other banks will step up their rates too.. or I’ll have to decide if it’s worth the hoops for the extra 1% over SoFi.

Yep, and Just like that…the hoops have been raised and lit on fire (4% requires $500 spend on the credit card monthly).

So on $250,000…

@ 3% – monthly interest = $626.00

@ 4% – monthly interest = $834.34

————–

$208.34 additional monthly interest

Additional details from looking at my HM Bradley account today:

——————————————————————————

Current APY (1)

4.00% APY (1)

———-

“APY (1) for December 2022

4.00% APY (1)

The direct deposit, positive cash flow, and credit card spend requirements are waived for this account through December 31, 2022.”

“(1)APY means Annual Percentage Yield. Terms and conditions apply; see NYCB Deposit Account Terms and Current APYs and NYCB Deposit Account Promotion for details”

—————————————————————————————–

From: https://www.hmbradley.com/new-NYCB-account-promo-september-2022

“These Promotions for HMBradley Deposit Accounts with NYCB are effective from September 29, 2022, through March 31, 2023.

Any customer who opens an HMBradley Deposit Account with New York Community Bank (NYCB) before November 1, 2022, will receive Level 2 Annual Percentage Yield (APY) until April 30, 2023. This promotional interest will be paid on the balance of the HMBradley Deposit Account with NYCB and will accrue and be credited to the deposit account according to the Deposit Account Agreement and Disclosures. No minimum balance is required to obtain this promotional APY. Interest rates and APYs may change any time after the account is opened. Interest is paid on account balances up to $250,000. Any fees may reduce the APY earned on the account. A minimum deposit of $100 is required to open an account. The qualifying direct deposit and positive cash flow requirements are waived through March 31, 2023. Terms and conditions apply; see HMBradley Deposit Account with NYCB Terms and Current APYs for more details.

Any customer who opens an HMBradley Deposit Account with NYCB and has an HMBradley Credit Card in good standing before November 1, 2022 will receive Level 3 APY on the balance of the HMBradley Deposit Account with NYCB until April 30, 2023. This promotional interest will accrue and be credited to the deposit account according to the Deposit Account Agreement and Disclosures. No minimum balance is required to obtain this promotional APY. Interest rates and APYs may change any time after the account is opened. Interest is paid on account balances up to $250,000. Any fees may reduce the APY earned on the account. A minimum deposit of $100 is required to open an account. The qualifying direct deposit, positive cash flow, and minimum credit card spend requirements are waived through March 31, 2023. Terms and conditions apply; see HMBradley Deposit Account with NYCB Terms and Current APYs for more details.”

———————————————————————————

From: https://www.hmbradley.com/APYs-NYCB

“Customers with HMBradley Deposit Accounts opened with New York Community Bank (NYCB) are eligible to earn the following annual percentage yields (APYs) in accordance with the Deposit Account Agreement & Disclosures.

APYs accurate as of 11/04/2022:

Level 1

2.00% APY

Customers who open an HMBradley Deposit Account with NYCB will earn 2.00% APY.

Level 2

3.00% APY

Customers who make a qualifying direct deposit of at least $500 per month to their NYCB deposit account and also maintain positive monthly cash flow (meaning that monthly deposits exceed monthly withdrawals, not including HMBradley Credit Card payments) will earn 3.00% APY in the following month.

Level 3

4.00% APY

Customers who make a qualifying direct deposit of at least $500 per month to their NYCB deposit account, maintain positive monthly cash flow (meaning that monthly deposits exceed monthly withdrawals, not including HMBradley Credit Card payments), and also spend $500 per month on their HMBradley Credit Card will earn 4.00% APY in the following month.

Interest rates and APYs may change any time after the account is opened. We do not pay interest on account balances above $250,000. Any fees may reduce the APY earned on the account. A minimum deposit of $100 is required to open an account.”

——————————————————————–

So, in reading through this…it “appears” that some of us may be getting 4% interest through April 30th without jumping through any flaming hoops (ex. $500 min spend on credit card), if you happen to have also been a Credit Card customer.

Is anyone else reading that from the info posted above/below (note: I’ve added *** around key points)?

“Any customer who opens an HMBradley Deposit Account with NYCB and has an HMBradley Credit Card in good standing before November 1, 2022 will receive Level 3 APY on the balance of the HMBradley Deposit Account with NYCB until *** April 30, 2023 ***. This promotional interest will accrue and be credited to the deposit account according to the Deposit Account Agreement and Disclosures. No minimum balance is required to obtain this promotional APY. Interest rates and APYs may change any time after the account is opened. Interest is paid on account balances up to $250,000. Any fees may reduce the APY earned on the account. A minimum deposit of $100 is required to open an account. **** The qualifying direct deposit, positive cash flow, and minimum credit card spend requirements are waived through March 31, 2023 .**** Terms and conditions apply; see HMBradley Deposit Account with NYCB Terms and Current APYs for more details.”

Thanks, I was actually just looking for that notice about it being extended through Q1 2023 last night for past customers, but I couldn’t find the email. It wasn’t interesting when it was only a top rate of 3%, but 4% is worth keeping in mind for those that already have the credit card.

You’re right… I’m currently getting 4% through at least Dec 31. It’d be nice if that extends through Mar 31 but I can’t count on that. Guess I’ll just leave my money parked there until January 1, at least.

If you got it through 12/31, it does look like you’ll get it through the end of April per CF Frost’s link. You’ll have to start doing the requirements in April to get the higher rates in May.

“Any customer who opens an HMBradley Deposit Account with New York Community Bank (NYCB) before November 1, 2022, will receive Level 2 Annual Percentage Yield (APY) until April 30, 2023.”

“Any customer who opens an HMBradley Deposit Account with NYCB and has an HMBradley Credit Card in good standing before November 1, 2022 will receive Level 3 APY on the balance of the HMBradley Deposit Account with NYCB until April 30, 2023.”

Maybe Jonathan could add this to this post…

I love it!!

https://userimg-bee.customeriomail.com/images/client-env-89662/4-APY_header-v2.png

A Valentines Day Update from HM Bradley!!! New Rate —> 4.20% APY

“It’s true: our highest interest rates just increased.

This Valentine’s Day, we’re sweetening the deal the best way we know how – by giving you an even better return on your money.

The rate increase took effect today, which means customers at our highest APY level (like you!) have already gone from earning 4.00% APY to earning 4.20%.1 (We’ve said it before, but it really does pay to use our products together! ?)”

“Our middle APY level got even sweeter, too

For customers who aren’t quite ready to go all in with HMBradley, our second-highest APY level now lets you earn 3.60% APY (that’s 60x the national average).2

———-

Do I need to start meeting requirements to obtain the higher interest rate?

Nope! If you opened your deposit account before February 1, 2023, the monthly deposit, positive cash flow, and credit card spend requirements are still waived for you through March 31, 2023.3 We simply wanted to let you know that the interest rate associated with your current APY level has increased!”

https://userimg-assets.customeriomail.com/images/client-env-89662/1676320384045_Frame%202073_01GS67P93WCYY4A7CQ0BQZ270T.png

Thanks, I was hoping for 5%…

I’d rather invest in short term T Bills (current paying more) than HMB

These people don’t know what they’re doing and make it up as they go along. Amateurs.

My year plus with them is enough to last a lifetime

Good Point. 5% would def. keep people from removing their money.

I wonder how many have pulled their money to chase 5% (Ex. Primis) at other banks.

I’m hoping someone soon breaches the 6% level – if so, I will probably move my remaining money out of HM Bradley. I recently moved $60k out of HM Bradely to fund four Chase accounts, to earn the recent $900 bonus promo they were running. Figured the money would be better over there for the next three months.

I’m surprised HMB is still even alive. I moved all my money into 4-week T-Bills at the end of last year. I don’t spend enough to hit the CC minimum, so I was out anyway in April. Tempted to open that 5% bank account from the interest rate roundup today, but rate chasing starts to become exhausting after awhile.

I’m not aware of many other banks that allow you to earn a higher rate of interest on up to $250k (My self-imposed limit, per account, to stay within FDIC coverage).

Primis bank also does NOT have cap on the total amount of money that one can earn. At their current rate of 5.03 APY on up to $250k, earning $1,025 is a nice return on idle cash.

True. For myself, I’d be chasing about 45 basis points versus 4-week T-Bills on a much smaller balance, so I’m not sure it’s worth the time. I guess we’ll see. Plus T-Bills are state and local tax free.

I noted that you wrote above: ” At these rates, I feel HMBradley is too much effort, and I don’t use them anymore. You can easily find a better rate elsewhere as of February 2023.”

Other than Primis bank, where are you seeing somewhere else to put up to $250k – if you’re grandfathered in like most of us, we’re getting 4.2% w/HMB through the end of April on up to $250k? I see more rate increases coming from the Fed and I think that will lead to us seeing 6% somewhere – that’s what I’m waiting for…and I’ll leave HMB (unless they keep surprising us with their own rate increases).

$250K FDIC will be increased by $250k for each added beneficiary

I got that $900 from Chase too. And 1K from Merrill for transferring over a TD brokerage account and $200 each for opening 4 Bank of America credit cards. Best I’ve done in a long time. Been churning too many years & places are telling me no.

Bada Bing, Bada Boom!!

New Announcement from HM Bradley!!!

“You’ve been patient as we rebuilt our back-end so that we can deliver features you expect and features you haven’t thought of yet. We are very, very close to announcing the launch of Routines and want to give you every reason to test it out.

That’s why we’ve extended the Deposit Account Promotions through June 30th, 2023. That means you’ll continue to earn 4.20%1 on your deposits, with the monthly deposit, positive cash flow, and credit card spend requirements waived through June 1, 2023.”

Woo Hoo…

I’ve left my idle cash here for now due to not having to jump through hoops at other banks – and 4.2% is nice to have for now – although, 4.2% is also no longer top-dog compared to other rates out there to chase.

I’m hoping HM Bradley will raise their rates soon…as I foresee others publishing 5%+ or even 6%+ rates in the near future!!! If I see 5.5% or higher, I may be gone from HM Bradley but for now (or until June), I’ll stick with them!

For @jonathan – Another image file to update in the thread!!

https://userimg-assets.customeriomail.com/images/client-env-89662/1677518161701_Frame%201260_01GT9XZHSS9PNK1HKQF0G04Y42.png

Definitely good news for existing customers. 🙂

Looks like some of us past HATCH Bank customers may be getting a letter in the mail very soon about a breach that Hatch bank had. I was checking my USPS Informed Delivery e-mail and see that I have a letter arriving today from Hatchbank c/o CyberScout (a credit monitoring company).

https://techcrunch.com/2023/03/02/hatch-bank-breach-fortra-goanywhere-exploit/

https://www.jdsupra.com/legalnews/hatch-bank-announces-third-party-data-4733497/

What’s interesting is that the story reports that hackers had access to Hatch’s data on Jan 30 and 31 and when Hatch was notified, they patched their systems.

I believe all of our accounts were closed late last year with the move over the NYCB?? Goes to prove that even after your account(s) are closed somewhere – the company who previously had access to your PII still has to protect it and if they don’t, your PII can be exposed in a digital hack of info.

More Free Credit Monitoring!!! Woo Hoo!!!

Interesting Article was posted on American Banker.com about HM Bradley, including the fallout with Hatch.

https://www.americanbanker.com/news/will-more-neobanks-like-hmbradley-seek-larger-sponsor-banks

Free to subscribe and read one article a day.

Will more neobanks like HMBradley seek larger sponsor banks?

By Miriam Cross – March 09, 2023, 12:47 p.m. EST