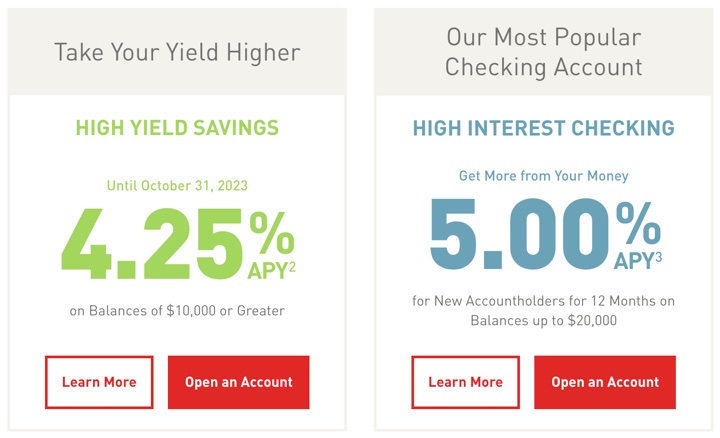

New promos with rate guarantees. Elements Financial Credit Union has a new rate of 4.25% APY on their High-Yield Savings on balances of $10,000+ (different from their Helium Savings). The promo rate is guaranteed until October 31, 2023. (Technically, it lasts until the 1st of the 12 month after you initial month, so actually between 11 and 12 months.)

There is also a promo rate of 5.00% APY on their High Interest Checking account, only valid on balances up to $20,000. Also for new accountholders only, with the promo APY fixed for 12 months from account opening date. Requires 15 qualifying transactions (such as using your debit card) every statement cycle. No monthly fee with electronic statements.

Note that their definition of qualifying transactions is also less strict than others. The following are qualifying transactions: Debit card purchases, checks, bill payments, ATM withdrawals and ACH withdrawals.

Per DepositAccounts, anyone can join with one-time $5 membership in Tru Direction, a not-for-profit organization dedicated to improving financial literacy. However, I couldn’t find anything about this on their membership page, other than Elements will provide you with $5:

Open an Elements checking or savings account or apply for a loan or credit card. During the application process, we will open you an Elements savings account (that’s the part that makes your membership official). We’ll even put $5 in to get you started — no need to transfer funds from an existing account!

I’m not sure how I feel about this one. 5.00% APY on $20k is a nice number ($1,000 a year in interest), but I don’t like having to remember the hoops for an entire year. They don’t seem to treat their existing customers nearly as well as new ones. Some of you may have signed up back in September 2022 when they offered a guaranteed 3.25% APY for a year on their Helium Savings. Right now, that account would only pay 1.00% APY once the promo ends.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

These are still attractive interest rates.

What do you mean by “with PARTIAL withdrawals and add-on deposits allowed.” I checked Helium’s website but see nothing about only allowing partial withdrawals. Thanks!

Usually if you have a CD, you can break it before maturity but often you have to take the whole amount. So if you bought a $10,000 CD, you’d have to withdraw the whole thing with added interest minus whatever penalty. Simply having a guaranteed rate on a savings account is much more flexible (but usually savings account don’t guarantee their rates).

“This is an interesting combination because this is a liquid savings account where you can still add or take money out whenever you want, but still enjoy a floor rate of 3.25% APY for a year”

So this is not subject to regulation D six transaction limit monthly? I can’t tell if the regulation D suspension was ever rescinded?

Thanks!

re six transaction limit monthly, I remember it was “suspended” when Pandemic started.

I am curios also if Elements has the restriction still?

Depositaccounts.com has them rated at B+ with a Capitalization rating of C-. Shoud that be of any concern?

Also, what’s there limits for withdrawals?

Account appear a bit more interesting given the changes to HMBradley announced today. Better rate with less hoops. Thoughts?

So the limits here are a cause for concern:

“Is there a limit to the amount I can transfer using Bank to Bank Transfers in Online Banking?

Yes, the per transaction limit for bank-to-bank transfers is typically $5,000, with a maximum of $10,000 per day, and $50,000 per month.

For the first 31 days after you open your first account with Elements, the limits are $1,000 per transaction, with a maximum of $2,000 per day, and up to $10,000 per month.”

It isn’t clear what their inbound limits might be, money pushed from another bank, or what the limits might be for funds pulled into another bank out of Elements via ACH initiated on the receiving end.

SoFi has an insanely high monthly limit, so I might just consolidate my savings and checking all in a single place and just be done with it. Rate chasing is a hassle.

Wow. Confirmed via email; They reject inbound ACH that exceeds limits from another bank.

So this is a definite no go. I can’t have my money held hostage.

“Hello,

Yes, we will reject the ACH if it is over the limit. “

2. Is there a limit if initiated from Elements?

1. What is the inbound ACH limit?

So if you push from another bank $20K they will reject? Really? Why would a bank reject new money deposits?

I didn’t realize this was even a thing, but yes. I transferred money from Alliant into Juno a few years ago, over the limit; Rejected with ACH rejection fee from Alliant. (The Juno limit on their side was like 2,500; apparently regardless of where it is initiated.)

Was very irate. I always look into ACH limits now.

Interesting! I always knew banks have limits but in regards to pushing out from that bank not upon being a recipient of money coming in. I had an issue with a bank once, so I pushed money in from Ally ( great bank) . When I needed the money I pulled it out from Ally and had no issue. As long as the transaction was initiated from the bank with higher limits.

Btw, rarely do I pay for fee after I complain about it and/or escalate to a higher level. I always get “ as a one time courtesy we will wave the fee”?

Btw, rarely do I pay for fee after I complain about it and/or escalate to a higher level. I always get “ as a one time courtesy we will wave the fee”?

I signed up for Helium account at Elements and got external banks set up for transfers. Now that I am going to transfer money, I see the rate is only 1% and not 3.25%

You have to reach a balance of $2,500 before you get the higher 3.25% rate for new customers.

This promo is over 🙁

Thanks for the heads up.

I just got set up with these accounts. I normally wouldn’t bother but the 12 month guarantee really made this enticing. Customer service was helpful in raising electronic check deposit limits to get me started-I was transparent with them about how much I wanted to deposit and they obliged.

It’s also helpful that the credit union has co-op branches and atms near me so if I do need to use a brick and mortar branch, I can.

I feel like I did my homework here before making this move and I’m hopeful my experience with Elements will remain good.