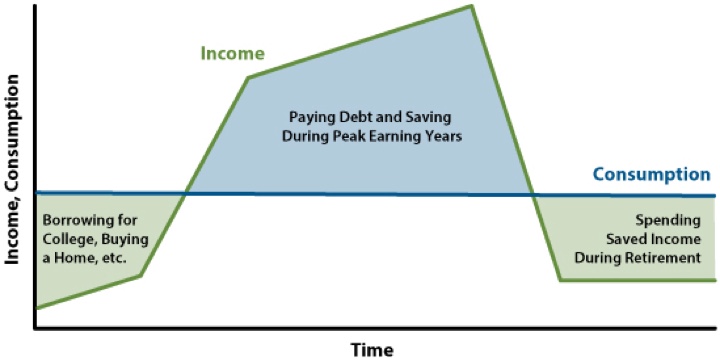

The idea of “consumption smoothing” tries to balance how our income changes over time with our spending needs. In theory, it may be ideal to go into debt when you are really young, save heavily when you are middle-aged, and spend it down when you are old (source):

The book Die With Zero (my review) reminds us that when we are young, we tend to have little money but lots of health. When we are old, we tend to have lots of time and much less health. So we should spend most of our money during our younger “best years” instead of when we are old. Here is a graphic from the book:

I enthusiastically support the idea of creating a specific bucket list of items designed for each stage of your life. However, I don’t like the title “Die with Zero” because it suggests that your time at the end is not valuable. A young, healthy person might think – why bother saving too much when you’re too old to enjoy it? Well, I would say that you start to appreciate the bottom layers of Maslow’s Hierarchy of Needs when you see them missing in someone’s life. (image credit)

We help take care of an older relative, and she has recently gotten to the stage where she can no longer safely live independently. According to the Katz Index of Independence, here are the basic activities of daily living (ADLs):

- Bathing and showering: the ability to bathe self and maintain dental, hair, and nail hygiene.

- Continence: having complete control of bowels and bladder.

- Dressing: the ability to select appropriate clothes and outerwear, and to dress self independently

- Mobility: being able to walk or transfer from one place to another, specifically in and out of a bed or chair.

- Feeding (excluding meal preparation): the ability to get food from plate to mouth, and to chew and swallow.

- Toileting: the ability to get on and off the toilet and clean self without assistance.

You may be 100% there mentally and only be struggling with one of these things, but that’s enough that you can’t live independently. The next level of “instrumental” activities of daily living includes things like cleaning, laundry, paying the bills, managing medication, cooking, shopping, communicating via telephone/computer, or transportation.

According to AARP, nearly 80% of adults age 65 and older want to remain in their current residence as long as possible. Seniors vastly prefer “aging in place” to facility care, and why wouldn’t they? The standard of care in an average nursing home is simply not that great. You live on their schedule, ignored most of the time. They are only required to give two baths a week. There are no national laws or regulations for staff to resident ratios. You may face a ratio of 15 residents to 1 nurse aid or worse. Medicaid pays for 6 in 10 nursing home residents. In 2021, a single Medicaid user must have under $2,382 per month in income and less than $2,000 in countable assets to qualify financially. Truly having “zero” near the end is not fun.

However, if you have the financial means, you can hire your own personal home health aide. This 1:1 ratio gives you your freedom back. You get to live in your own house. You wake up and live on your own schedule. You get to choose the food that you eat. You bath every day. You have someone to drive you wherever you want. You can still do your own shopping. You can have lunch with your friends. You can go to social events (memories! experiences!). This can get expensive at $15 to $30 an hour (often less overnight), but I’ve discovered that 1-on-1 help is the “luxury good” that the wealthy buy at this stage of their lives.

One of the findings of behavioral psychology is that above a certain level of income (maybe $80k a year in 2021?), you don’t get that much happier. At a certain point, you have your needs met and you feel safe and relatively comfortable. Above that, it’s mostly a nicer house, fancier car, more expensive restaurants, etc. Earning more doesn’t give you a more loving family and group of friends. When you get older, I’ve now seen how extra money can get you back to that level of satisfied comfort if you have health issues. The difference that I see in happiness levels was surprising to me. It just reminds me that the freedom to spend our time how we wish is the true goal.

Upgrading from the “economy” to “business class” lifestyle in your 40s is nice, but so is upgrading from a nursing home to 1-on-1 personal attention in your 70s and 80s. The very wealthy can afford both. But for the rest of us, it’s something to think about. Maximize pleasure when you are younger, or minimize suffering when you are older?

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

As an older reader, my wife and I are both 65+, I can attest that you may surprise yourself with how fit and active you can be at what you may now consider to be a horrifically old age. My 66 year old wife ran a full marathon this year and won the grand masters trophy. We both run three times a week at 5:30 in the morning with a group that has people from age 39 all the way to some in their 70’s. Two of the 70+ runners are in the top three in terms of how fast they can click off a five miler. My wife and I both compete very well on tennis teams of age 40 and over even though we are playing against people twenty years younger than us. If you do aerobic and strength training from your twenties for the rest of your life you may well surprise yourself when you get to my age. It takes a lot of hard work and a good bit of luck to avoid age related chronic illness and injury, but 60-70-80 aren’t what they used to be. We even have a 90 year old tennis player in this rural area who still hits a good game.

Yes, I’ve known 70+ folks who still windsurf and ski and play tennis regularly (and beat me too!). Those friends are my role models. 🙂

I am more about avoiding discomfort, than maximizing pleasure. I’m fine missing a bit of fun now, to try to make sure I am as comfortable as I can be later in life.

I agree in that I want to make sure that I have a base level of comfort and security for me and my family. I wouldn’t want to risk that tomorrow for a luxury today.

I have to say, I am always impressed with the quality of comments you get on your blog. Kudos to you for running an informative, educational and thoughtful blog.

Thanks! I agree that I have been fortunate to have gained many thoughtful, wise, and intelligent readers over the years.

Hey there, I just found your site. I agree with some of the other comments, your blog is informative and interesting, will find time to read through the rest of posts.

Anyway coming back, I just finished reading Die With Zero as well, and in the midst of digesting and summarizing it. I also run a simple and raw blog and may write something about this book in the future.

I agree with most of your points, especially things like tone deaf from your previous review post. However, when it comes to what you described in this post, I felt that you have missed his point slightly.

If I put myself into his shoe, I feel that his main point is being a lot of mindful about your current till future earnings, and plan your current and future spending in a way that you don’t suffer much of your life living under relative poverty (at least when compared to other stages of your life). It is really eye opening at least to me.

To me, the key word is being mindful. And you are asking exactly the right question to be mindful of spending at old age. But isn’t it the same thing that he was sharing in his book: Everybody’s situation is different and everybody has to ask this question of “how much do I need to spend in my old age?”

So coming back, I feel that the easy follow up to your points is that, plan all these spending in. Still aim to die with zero, but you also need to plan for the amount of money you need just before you die. Die with zero, but live with “one year worth of spending money” one year before dying. If it takes a lot of money to pay for this elder care, then you have to plan it in. And it also means that your “consumption smoothing” may not work as well. And naturally this means that you might not be earning enough today to actually meet this requirement, and maybe that means you need to be more aggressive in your investment? Or maybe there is a better way to plan for elder care?

I can go on and on, and there is no clear answer from any of these questions, but this is the true value that I see from this book: challenge our thinking that we just need to worry about how much we earn and spend now.

Of course we still don’t know when we will actually die but it’s worth the exercise to think about it.