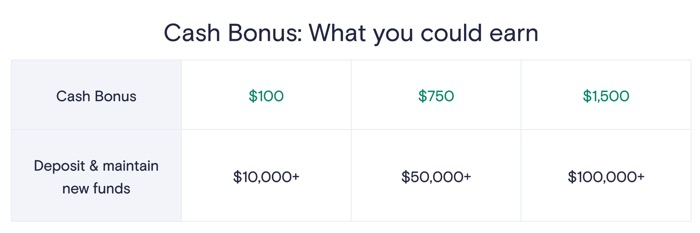

Updated offer for 2026. May sure you enroll first! Marcus by Goldman Sachs is offering a up to a $1,500 deposit bonus (starting at $100 bonus on $10,000 in new funds) into their online savings account within 10 calendar days of enrollment at this special offer page. Valid for both new and existing customers. You must enroll first by 3/11/26 and maintain the new funds for 90 days (after the end of the 10-day funding period, so possibly up to 100 days total). You then get the bonus after another 14 days. No offer or promo code required. They have done a similar promotion in past years (and it’s nice that you can keep doing it). Here are the tiers:

After enrolling, you must deposit $10,000 or more in new funds from an external account into your Account within 10 calendar days of enrollment (the “Funding Period”). The Account balance plus a minimum of $10,000 in new funds (the “Required Dollar Amount”) must be maintained in your Account for 90 consecutive days from the end of the Funding Period. The Account balance is based on the starting current balance reflected on your account at 12 am ET the day you enroll. Once the Funding Period has ended, your Account balance may not drop below the Required Dollar Amount at any point until after the 90 consecutive days have passed. You may make multiple deposits within the Funding Period to reach the Required Dollar Amount. Internal transfers do not count for purposes of this Offer.

Important disclosures: Enroll your Online Savings Account in the Offer, then deposit (within 10 calendar days of enrollment) and maintain at least $10,000 (for $100 bonus), $50,000 (for $750 bonus), or $100,000 (for $1,500 bonus) of New Funds, plus your balances in your enrolled account and across all Marcus accounts as of 6:00 pm ET on 1/27/26, for 90 days after the 10-day Funding Period. Withdrawals made by you or a joint owner while enrolled, including CD maturities to non-Marcus accounts or CD early withdrawals, may result in a lower bonus or losing eligibility, depending on your balances.

New customer referral offer. If you don’t have a Marcus account yet, if you open with a Marcus referral link from an existing customer, you will a small 0.25% bonus (it keeps shrinking!). That’s my referral link, thanks if you use it! I’d open and get the referral offer first, and then later enroll in this $100 offer as an existing customer.

New customer referral offer. If you don’t have a Marcus account yet, if you open with a Marcus referral link from an existing customer, you will a small 0.25% bonus (it keeps shrinking!). That’s my referral link, thanks if you use it! I’d open and get the referral offer first, and then later enroll in this $100 offer as an existing customer.

Bonus math. Here’s how it works out for each tier:

- $100 is a 1% bonus on $10,000 if you keep it there for 90 days, which makes it the equivalent of ~4% APY annualized.

- $750 is a 1.5% bonus on $50,000 if you keep it there for 90 days, which makes it the equivalent of ~6% APY annualized.

- $1,500 is a 1.5% bonus on $100,000 if you keep it there for 90 days, which makes it the equivalent of ~6% APY annualized.

The bonus is on top of the standard interest rate, currently 3.65% APY as of 1/29/2026. Compare with my latest update of best interest rates. I have gotten a similar Marcus bonus in the past with no issues. Make sure you enroll at the link above first before transferring in your new funds.

Checked and updated for 2026. Since these are available every 12 months, it is a good idea to check these near or around the same time each year. A lot of companies make their money by collecting and selling data – your personal data. It can be critical to know what they are telling prospective lenders, landlords, even employers about you. Under the FCRA and/or FACT Act, many consumer reporting agencies (CRAs) are now legally required to send you a free copy of your report every 12 months, as well as provide a way to dispute incorrect information.

Checked and updated for 2026. Since these are available every 12 months, it is a good idea to check these near or around the same time each year. A lot of companies make their money by collecting and selling data – your personal data. It can be critical to know what they are telling prospective lenders, landlords, even employers about you. Under the FCRA and/or FACT Act, many consumer reporting agencies (CRAs) are now legally required to send you a free copy of your report every 12 months, as well as provide a way to dispute incorrect information.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)