The Bank of America Customized Cash Rewards Credit Card is the “3-2-1” cash back rewards credit card in the Bank of America line-up. If you’re a Preferred Rewards client, you can increase that bonus by up to 75%. For such “relationship” customers, the bonus can change this card from good to great. Here are the highlights:

- $200 cash rewards bonus after $1,000 in purchases in the first 90 days.

- Earn 1% cash back on every purchase, 2% at grocery stores and wholesale clubs, and 3% on your choice category up to the first $2,500 in combined grocery/wholesale club/choice category purchases each quarter

- Cardholders will be able to choose their 3% cash back category from one of these 6 options: gas, online shopping, dining, travel, drug stores, or home improvement and furnishings. Before it was only gas. You can change your category once each calendar month in-app or online. Do nothing and it will stay the same.

- 0% Introductory APR offer. See link for details.

- Get a 10% customer bonus every time you redeem your cash back into a Bank of America® checking or savings account

- If you’re a Preferred Rewards client, you can increase that bonus to 25% – 75%. See details below.

- No annual fee.

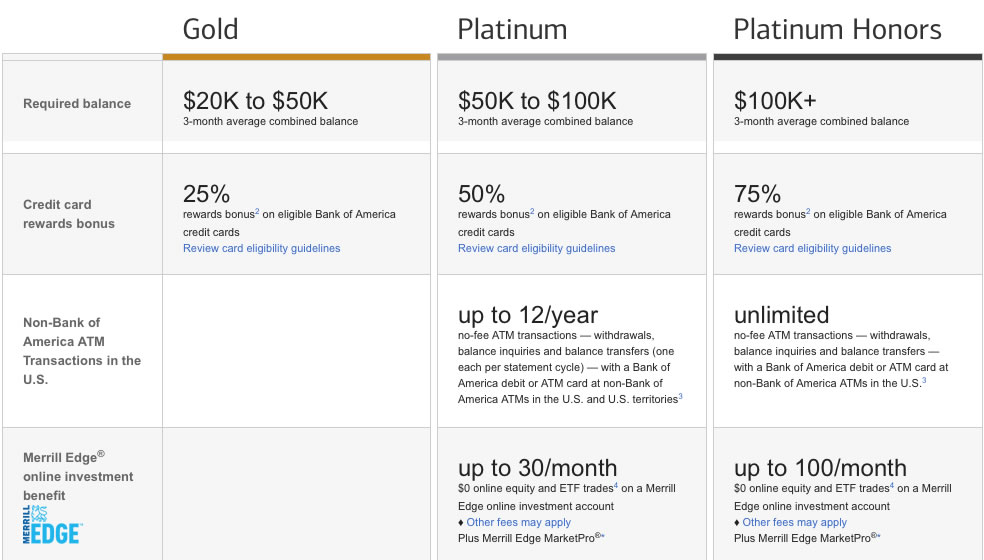

Preferred Rewards bonus. The Preferred Rewards program is designed to rewards clients with multiple account and higher assets located at Bank of America banking, Merrill Edge online brokerage, and Merrill Lynch investment accounts. Here is a partial table taken from their comparison chart (click to enlarge):

Let’s consider the options. Bank of America’s interest rates on cash accounts tend to be lower than highest-available outside banks (read: nearly zero), so moving cash over to qualify may result in earning less interest on your cash deposits. Merrill Lynch advisory accounts also usually come with management fees. The sweet spot is therefore the Merrill Edge self-directed brokerage, where you can move over your existing brokerage assets like stocks, mutual funds, and ETFs held elsewhere (Vanguard, Fidelity, Schwab, etc).

In the past, moving over to Merrill Edge at the Platinum and Platinum Plus levels also led to 30 to 100 free online stock trades every month. Fast forward to now, and nearly all major online brokers offer commission-free trades anyway.

Personally, I moved over $100k of brokerage assets from Vanguard to Merrill Edge to qualify for Platinum Honors. You should ask Merrill Edge if they will cover any ACAT transfer fees involved. I realize not everyone will have this level of assets to move around, but if you do then it is worth considering. Keep in mind that it will take a while for your “3-month average combined balance” to reach the $100k level and officially qualify for Platinum Honors. You might become Gold first, then Platinum, and so on. After that, the 25%-75% rewards bonus on credit card rewards kick in. Once you reach a certain tier, BofA guarantees that you will stay there for a year no matter what, even if your balance fluctuates.

Note that the terms state “The Preferred Rewards bonus will replace the customer bonus”, which means that you will lose the 10% customer bonus when you qualify for the 25% to 50% bonus.

Cash Back Rewards after Preferred Rewards bonus:

Recall that the basic structure is “1/2/3”; you get 1% cash back on every purchase, 2% at grocery stores and wholesale clubs and 3% on choice category for the first $2,500 in combined grocery/wholesale club/gas purchases each quarter (1/2/3). Here’s how the bonuses work out:

- Platinum Honors: 1.75% cash back on every purchase, 3.5% at grocery stores and wholesale clubs, and 5.25% on choice category for the first $2,500 in combined grocery/wholesale club/gas purchases each quarter.

- Platinum: 1.5% cash back on every purchase, 3% at grocery stores and wholesale clubs, and 4.5% on choice category for the first $2,500 in combined grocery/wholesale club/gas purchases each quarter.

- Gold: 1.25% cash back on every purchase, 2.5% at grocery stores and wholesale clubs, and 3.75% on choice category for the first $2,500 in combined grocery/wholesale club/gas purchases each quarter.

Note that the terms state “The Preferred Rewards bonus will replace the customer bonus you may already receive with the card.”, which means that you will lose the 10% bonus for redeeming your cash back into a Bank of America® checking or savings account.

I like the idea of getting up to 3.5% cash back at Costco, Sam’s Club, and BJs wholesale clubs. Costco only takes Visa, so make sure the application shows a Visa. If you have a Mastercard, you could try and call them and request to switch to a Visa version of the card instead of a Mastercard.

I also like the idea of getting up to 5.25% cash back on “online shopping” assuming that includes Amazon, although Amazon’s own card already offers 5% back.

This is finally a case where bundling services actually worked out for me. Bank of America has managed to convince me to go from only having a checking account with them to now also having a Merrill Edge brokerage account and a Bank of America credit card.

Not all Bank of America consumer credit cards qualify for Preferred Rewards. Other cards of interest that do qualify are:

- Bank of America Travel Rewards Card

- Bank of America Premium Rewards Card

- Bank of America Unlimited Cash Rewards Card

Bottom line. The Bank of America Cash Rewards Credit Card is an “okay” cash back rewards card with a 1/2/3 structure, but turns into an “excellent” rewards card if you can take full advantage of their Preferred Rewards program. If you transfer $100,000 of existing brokerage assets over to Merrill Edge, you can qualify for the highest Platinum Honors tier. This won’t be a good option for everyone, but something to be aware of if you can swing it.

A friend of ours told us about the Colorado Ski Passport that lets 5th and graders from any state ski for free at several Colorado resorts, and I thought that was a great concept to promote this fun outdoor activity. If you can get even a single free lift ticket (and possibly even a free lesson with rentals), that can be a big savings these days. This led me to more digging and I found that several other states have similar programs.

A friend of ours told us about the Colorado Ski Passport that lets 5th and graders from any state ski for free at several Colorado resorts, and I thought that was a great concept to promote this fun outdoor activity. If you can get even a single free lift ticket (and possibly even a free lesson with rentals), that can be a big savings these days. This led me to more digging and I found that several other states have similar programs. Expedia has a new coupon code THANKYOU which will get you $30 off $40+ in experiences booked through

Expedia has a new coupon code THANKYOU which will get you $30 off $40+ in experiences booked through

One of the newer work perks that we took advantage of this year was the Dependent Care Flexible Spending Account (DCFSA). This is separate from the Health Care Flexible Spending Account (HCFSA) and the Health Savings Account (HSA). However, they do work in a similar way in that you can pay for eligible expenses with pre-tax money and thus save money by being exempt from income taxes on that amount. For example, we were able to pay for $5,000 in preschool expenses using your DCFSA in 2018. At a a 30% marginal total tax rate (see below), that was a $1,500 savings.

One of the newer work perks that we took advantage of this year was the Dependent Care Flexible Spending Account (DCFSA). This is separate from the Health Care Flexible Spending Account (HCFSA) and the Health Savings Account (HSA). However, they do work in a similar way in that you can pay for eligible expenses with pre-tax money and thus save money by being exempt from income taxes on that amount. For example, we were able to pay for $5,000 in preschool expenses using your DCFSA in 2018. At a a 30% marginal total tax rate (see below), that was a $1,500 savings.  Here’s my monthly roundup of the best interest rates on cash for December 2018, roughly sorted from shortest to longest maturities. Check out my

Here’s my monthly roundup of the best interest rates on cash for December 2018, roughly sorted from shortest to longest maturities. Check out my

If you like to send out holiday greeting cards, I thought I’d throw out a quick tip that Mrs. MMB uses each year to save a bit of money.

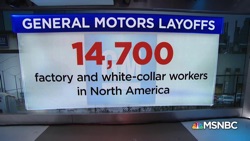

If you like to send out holiday greeting cards, I thought I’d throw out a quick tip that Mrs. MMB uses each year to save a bit of money. I found myself thinking a lot today about General Motors

I found myself thinking a lot today about General Motors  Tuesday, November 27th is Giving Tuesday 2018. This time of year is huge for charities, with 40% of donations occurring in the last six weeks of the year. Here are some ways you can “double your impact” with a matching donation.

Tuesday, November 27th is Giving Tuesday 2018. This time of year is huge for charities, with 40% of donations occurring in the last six weeks of the year. Here are some ways you can “double your impact” with a matching donation. The Best Credit Card Bonus Offers – May 2024

The Best Credit Card Bonus Offers – May 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - May 2024

Best Interest Rates on Cash - May 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)