Warren Buffett had his annual charity lunch today and was on CNBC for a short interview. As usual, he was asked about the current stock market situations and, as usual, he managed to sum everything up in a few folksy sentences. Here’s a direct quote from the full CNBC interview:

Warren Buffett had his annual charity lunch today and was on CNBC for a short interview. As usual, he was asked about the current stock market situations and, as usual, he managed to sum everything up in a few folksy sentences. Here’s a direct quote from the full CNBC interview:

If you had your choice between buying and holding a 30-year bond for 30 years or holding a basket of American stocks, there’s just no question, you’re going to do better owning stocks. It’s more attractive than, considerably more attractive than fixed income securities. That doesn’t meant they’re going to go up or down tomorrow, next week, or next year, but over time, a bunch of businesses that are earning high returns on capital are going to beat a bond that’s fixed at roughly 3% or 30 years. And it’s not my field of specialty, but actually they look, stock generally (American businesses), they look cheaper than, generally, real estate.

[…] That’s what you have to do in investing. I mean, you’re sitting with some cash in your pocket. You have savings, and the question is what do you do with it? You can buy a duplex next door and rent it out to people and do fine over time or buy a small piece of farmland or something of the sort or you can put it into something fixed income, bonds, or bank deposits, or whatever it may be.

My interpretation is that you have invest your money somewhere, and if you have a 30-year time horizon and you don’t plan on timing the market in and out, then stocks are still your best bet. Over the long haul, stocks will still outperform bonds and cash (at current interest rates), and he thinks real estate as well right now. Timing the market is too hard to do. Predicting returns over the next 5 years is too hard to do. If you don’t have a long enough time horizon or can’t handle the swings, you shouldn’t be in stocks.

Long-term stock investors just have to take some lumps if prices drop for a while. Keep enough money in bonds and cash so you don’t panic and have money to spend in the meantime.

[I actually have an issue with the CNBC caption “Buffett: Stocks always more attractive than bonds”. He never said that. He specifically noted that the 30-year bond was paying 3%. In the past (1970s?), Buffett has invested in Treasury bonds when the rates were really high and the stock market was overvalued. If today’s rates were 8% instead of 3%, Mr. Buffett would be rational enough to adjust his opinion.]

Series I Savings Bonds (aka “I Bonds”) are a unique investment sold directly to individuals by the US Treasury that pay out a variable interest rate linked to inflation. This post collects general reasons to own these savings bonds without going into the internal details of how they work. Please also see my related post

Series I Savings Bonds (aka “I Bonds”) are a unique investment sold directly to individuals by the US Treasury that pay out a variable interest rate linked to inflation. This post collects general reasons to own these savings bonds without going into the internal details of how they work. Please also see my related post  This is not a happy post, but it’s also the reality for a lot of people so I think it is a valid discussion. The Early Retirement forums had a thread recently titled

This is not a happy post, but it’s also the reality for a lot of people so I think it is a valid discussion. The Early Retirement forums had a thread recently titled

After my last

After my last

Chase just announced a new free stock trade program as part of a new online brokerage arm called You Invest. This means another megabank is moving more heavily into “relationship banking” where they hope you will keep your bank accounts, credit cards, brokerage accounts, and mortgage all at the same place. This is pretty significant as JP Morgan Chase is the largest US bank in terms of both market value and total customers (over 60 million).

Chase just announced a new free stock trade program as part of a new online brokerage arm called You Invest. This means another megabank is moving more heavily into “relationship banking” where they hope you will keep your bank accounts, credit cards, brokerage accounts, and mortgage all at the same place. This is pretty significant as JP Morgan Chase is the largest US bank in terms of both market value and total customers (over 60 million).

When it comes to constructing a portfolio, I used to think it was all about numbers and optimization. When you pick an asset class based on historical data, that assumes you hold through both the good times and the really bad times. It has helped me to keep gathering nuggets of knowledge over time to maintain my faith during those really bad times.

When it comes to constructing a portfolio, I used to think it was all about numbers and optimization. When you pick an asset class based on historical data, that assumes you hold through both the good times and the really bad times. It has helped me to keep gathering nuggets of knowledge over time to maintain my faith during those really bad times.

Reading children’s books to my kids has become a regular source of new wisdom. I guess that’s not surprising, if the goal is to teach kids about life. Here’s one that came across recently and keeps popping back in my head.

Reading children’s books to my kids has become a regular source of new wisdom. I guess that’s not surprising, if the goal is to teach kids about life. Here’s one that came across recently and keeps popping back in my head. Here’s a refreshingly blunt quote from Scott Galloway’s article

Here’s a refreshingly blunt quote from Scott Galloway’s article  I was surprised to read the NY Times article

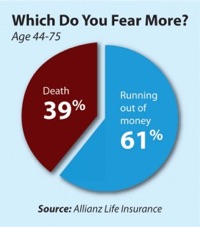

I was surprised to read the NY Times article  People don’t like talking about money. That’s why I started this site. You know what people like talking about even less? Death.

People don’t like talking about money. That’s why I started this site. You know what people like talking about even less? Death. The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)