Bonuses for my Emigrant Direct Signup Promotion went out today for those that sent me their final form in December. Emigrant Direct offers a savings account paying 5.05% APY with no minimum balance. If you’re interested, be sure to get another $10-$20 out of it.

Archives for February 2007

February 2007 Financial Status / Net Worth Update

Posted on February 5, 2007 // 22 Comments

About My Credit Card Debt

Newer readers may be alarmed by my high levels of credit card debt. In short, I’m borrowing money for free and keeping it in safe investments while earning me interest. Along with other things, this helps me earn extra side income of thousands of dollars a year. Recently I put up a detailed series of posts on this 0% game. So please, don’t worry!

Summary

While we are still recovering from the hit when we converted our Traditional IRA to a Roth IRA, this month was one of our strongest yet. First, the stock market continued upwards and our portfolio followed passively. Second, my wife got a healthy bonus from her job in January. Third, I renewed some advertising contracts on this site. Fourth, we had less unexpected expenses stemming from personal events than in previous months.

We are now at $42,992 in net cash and $50,335 in total non-retirement assets. Our mid-term goal of $100,000 for a house-downpayment is still in reach, especially with recent developments… The job search is going well and it looks like one of us (hint: not me) will be getting a big raise soon. This has been in the works actually for a while, but we had a few worried moments here and there. Now all the pressure is on me!

You can see all my previous net worth updates here.

Our Savings Rate Is (Still) Negative: Should We Worry?

Posted on February 4, 2007 // 27 Comments

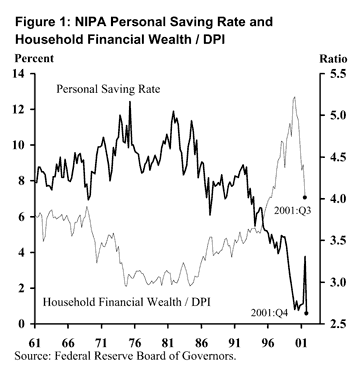

A few days ago, the US Department of Commerce released1 that the nation’s savings rate for 2006 was negative 1%. This means as a whole we spent more than we earned after-taxes, again. (It was also negative for 2005). Much is being made about how this is the lowest savings rate since the Great Depression, when there was a negative 1.5 percent rate in 1933. Should we be worried? Is the sky falling?

What’s the recent trend?

I wonder what the margin of error is on this data. Looking at this graph, it seems like perhaps something happened about a year and a half ago? But then I found it goes back a lot further than that. This chart starts from the 1960s2:

To help better understand the numbers, you have to go into the definitions a little bit. The personal savings rate ignores the capital gains in our investments like stocks and bonds, and also tangible assets like cars and real estate. In fact, our overall net worth is not doing that bad and actually increased over last year. The graph above tracks this by dividing household total wealth by disposable personal income (DPI). There are a few ways the experts try to explain this:

[Read more…]

Free Samples From Wal-Mart

Posted on February 3, 2007 // 2 Comments

Manufacturers often give away free samples of their new products that will soon be on Wal-mart shelves. Even if you don’t shop there, you can sign up for those free samples here.

Currently available:

– Dove shampoo for color-treated hair

– Digestive Advantage for lactose intolerance

– Sunsilk shampoo

– Viactiv calcium and vitamin supplements

My favorites are the free razors. You know how they add a blade every few months. (Next up… the Gillette Ocho!) For some reason I’ve been seeing a lot of free shampoo recently. Did anyone else get a big box of Pantene from MySurvey?

Are Online Savings Accounts Becoming A Commodity?

Posted on February 3, 2007 // 32 Comments

As online savings accounts get more and more popular, I get the feeling that they are becoming a mature product, almost a commodity. Sure, there will still be the occasional promotions, but for the most part all of the banks now are hovering around the same interest rate (currently ~5% APY). I believe that the banks simply don’t have the ability to go that much higher and remain profitable.

Exhibit A: E-Loan Savings, which burst on the scene with a 5.5% APY rate, is now back down to 5.25% after only a few months. GMAC Bank is down to 5% APY. Both are tightly connected with streamlined internet mortgage lenders. If they can’t go higher, who can?

Exhibit B: HSBC Direct is currently offering a nice 6% APY rate on new money, but it’s temporary and will revert back to 5.05% in May.

Once every account starts paying around the same rate, they’ll will have to start competing more on customer service and convenience. People want easy online transfers between their accounts, ATM access, and a reliable and user-friendly website. Most people also value the ability to stay with their current bank.

Exhibit C: I am increasingly using my Washington Mutual 5% APY savings account (my review) because I can deposit checks and withdraw cash directly to and from the account from a local ATM, and also initiate external online transfers. If I need to write a check or make a bill payment, I just move over some money instantly to their free checking account (with 1 free overdraft as a backup). In the meantime, all but a few hundred dollars are always earning 5%.

I expect other banks with a large physical presence to follow suit, but notice that they will be only targeting internet-savvy folks who are aware of all the options! Checking accounts paying zero interest are their bread and butter, and they don’t want to make it easy on everyone to switch. WaMu’s account is only available online. (Even for their own employees! I asked.) Citibank has their e-Savings Account paying 4.75% APY, which also must be opened online. Bank of America recently rolled out an online-only 5-month CD paying 4.50% APY ($5,000 min).

Starting Your Own Portfolio Out With Limited Funds

Posted on February 3, 2007 // 3 Comments

All of these suggested portfolios were developed by smart people who did their homework. But none of them are the same! This is because every single one also made compromises based on their interpretation of current research, simplicity, availability of suitable investments, costs, and also to some measure their overall predictions of the future. We have to do the same thing on our end.

For example, many people are starting with smaller amounts. Some of these model portfolios have 8 funds or more! Just by the fund minimums alone, you’d be looking at a minimum balance of $24,000 or so. And even then, you’d be looking a various low balance and maintenance fees. So what do you to minimize fees? Here are a few ideas:

1) Buy an all-in-one fund, and split it up later. Since many fund companies have all-in-one target-dated funds, you can simply buy one of these until you have enough to split into other funds. Here are some specific fund suggestions, starting at only $50 per month. The fund’s asset allocation may not be exactly what you want, but it will be well-diversified, and still much better than other high-cost alternatives. Here’s what the Vanguard Target 2045 Fund looks like:

I built up about $50,000 in Vanguard Target funds (VTIVX and VTTHX) before splitting it up into 8 funds last year. Since they were held in IRAs/401ks, I didn’t have to worry about any tax consequences. This choice is my favorite because it’s the most simple – just buy the same fund for a few years!

[Read more…]

Model Portfolio #6: Merriman’s FundAdvice Ultimate Buy and Hold

Posted on February 2, 2007 // 31 Comments

(This is the sixth in my series of Model Portfolio Comparisons.)

Paul Merriman also runs his own money management firm. He also writes at FundAdvice.com, which has a lot of interesting articles about investing in no-load mutual funds, with and without market timing. Here is the breakdown of their “Vanguard balanced buy-and-hold portfolio”.

Asset Allocation For 60% Stocks/40% Bonds

6% S&P 500

6% US Large Value

6% US Small

6% US Small Value

6% REIT

12% International Developed (Pacific + Europe)

12% Int’l Value

6% Emerging Markets

20% Intermediate Term Bonds

12% Short Term Bonds

8% Inflation-Protected Securities (TIPS)

They have other suggested buy-and-hold portfolios for different brokerages, which vary slightly but are still very similar. I find it interesting that the stock portion is perfectly 50/50 domestic/international.

IRS Calculator To Help Determine Sales Tax Deduction

Posted on February 1, 2007 // 1 Comment

If you itemize deductions and live in a state with sales tax, give the IRS Sales Tax Deduction Calculator a spin.

Taxpayers who itemize deductions on Schedule A of the Form 1040 in 2006 have the option of deducting the amount of state and local sales taxes paid instead of deducting their state and local income taxes paid. Taxpayers cannot take a deduction for both sales and income taxes.

Residents of states with no income tax should definitely look into this. If you have made some large purchases this past year, it may also be worth the effort to dig up those receipts. Via Consumerist.

Model Portfolio #5: A Random Walk Down Wall Street

Posted on February 1, 2007 // 7 Comments

(This is the fifth in my series of Model Portfolio Comparisons.)

First written in 1973, Burton Malkiel’s A Random Walk Down Wall Street (my review) has become an investing classic, pioneering the controversial idea that stock prices are random and thus a monkey throwing darts would be just accurate as any stock-picker. Below is a recommended asset allocation from the book for an investor in their “mid-twenties”.

Bold Investor Model Portfolio

Asset Allocation for suggested 75% Stocks/25% Bonds ratio

43% Total US Stock Market

22% Total International Stock Market

10% REIT

20% Treasuries/TIPS/High-Quality Corporate Bonds

5% Cash

This breakdown looks very similar to the basic “Early Saver” portfolio from All About Asset Allocation. See the rest of the model portfolios for example mutual funds and ETFs for each asset classes.

As you age, the recommended percentage of stocks goes down to 65% at age 40 and 40% in late retirement. It is interesting to note that while Malkiel consistently recommends real estate as part of your portfolio, REITs were not explicitly included in the recommended portfolios until recently. I noticed this when comparing my personal copy (published in 1996) to the most recent edition. I’m guessing the growing availability of index funds that track REITs is the reason behind this.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)