American Express has partnered with the Point.me award travel tool to provide free flight searches for the airline loyalty programs that work with American Express Membership Rewards points. The special site is AmEx.Point.me, where you must log into your American Express account.

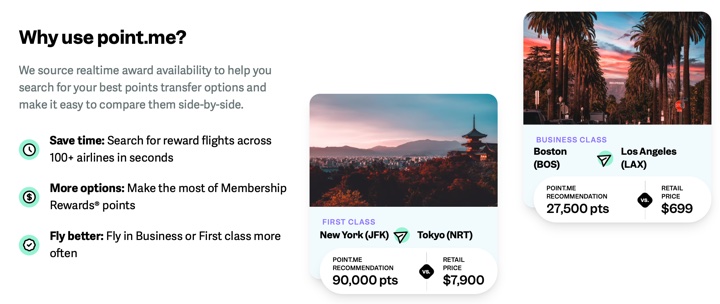

With point.me for Membership Rewards® points, eligible Card Members have access to a real time reward-flight search engine. POINT.ME makes it easy to see all of the options, and choose the flight that works best for you before transferring Membership Rewards® points to eligible airline loyalty programs through your Membership Rewards® account.

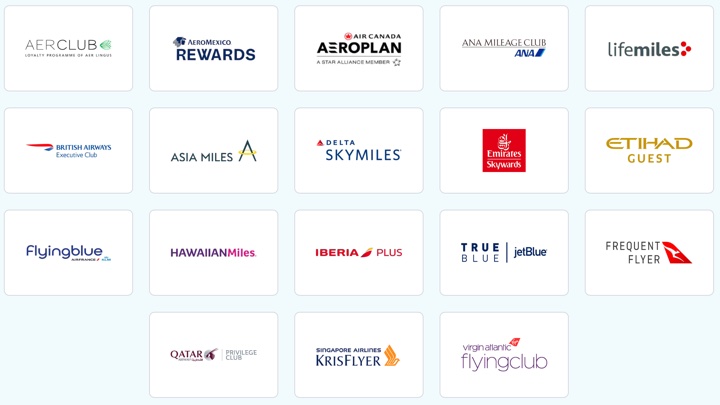

I am hopeful for this new service, as Membership Rewards has a lot of transfer partners but it can be hard to find the best flights across them all. (Bilt Rewards has also partnered with Point.me for free award searches.) The searches can take a while to finish, but hopefully it’s still better than searching manually. The full version of the Point.me website usually costs $12 a month or $129 a year for all airlines (first 3 searches free). There is also a more expensive Concierge service where a human expert will handle everything for $200/person.

Loyalty programs have been around for decades, especially in the airline industry. However, booking award travel can feel cumbersome, like you’re jumping through multiple hoops just to book a flight! This is where point.me comes in. We’re the first company to offer a tool that makes it easier to use miles and points for air travel. Not only does our tool show you flight options that are bookable using your points, we also guide you step-by-step to book the flight yourself!

Also see: Top 10 Best Credit Card Bonus Offers.

The

The

Southwest Rapid Rewards® Plus credit card

Southwest Rapid Rewards® Plus credit card Southwest Rapid Rewards® Premier card

Southwest Rapid Rewards® Premier card Southwest Rapid Rewards® Priority card

Southwest Rapid Rewards® Priority card Southwest Rapid Rewards Performance Business card

Southwest Rapid Rewards Performance Business card Southwest Rapid Rewards Premier Business card

Southwest Rapid Rewards Premier Business card

The Best Credit Card Bonus Offers – May 2024

The Best Credit Card Bonus Offers – May 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - May 2024

Best Interest Rates on Cash - May 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)