Reading Warren Buffett’s Annual Letter always reminds me that stocks are not just some numbers that bop up and down, but are shares of real businesses with land, factories, knowledge, and hard-working people. This helps reassure me that the value of those companies taken together will never go to zero, and will eventually rebound and grow over the long term. At the same time, once you stop working and start selling shares, the prospect of going to zero is real. If you combine a prolonged bear market and forced withdrawals at depressed prices, you risk permanently impairing your portfolio.

Reading Warren Buffett’s Annual Letter always reminds me that stocks are not just some numbers that bop up and down, but are shares of real businesses with land, factories, knowledge, and hard-working people. This helps reassure me that the value of those companies taken together will never go to zero, and will eventually rebound and grow over the long term. At the same time, once you stop working and start selling shares, the prospect of going to zero is real. If you combine a prolonged bear market and forced withdrawals at depressed prices, you risk permanently impairing your portfolio.

According to a Merrill Lynch survey of wealthy families with $5+ million (not just people on the street!), 39% of them thought you could spend 6% or more from your portfolio indefinitely. The reality is closer to 3%.

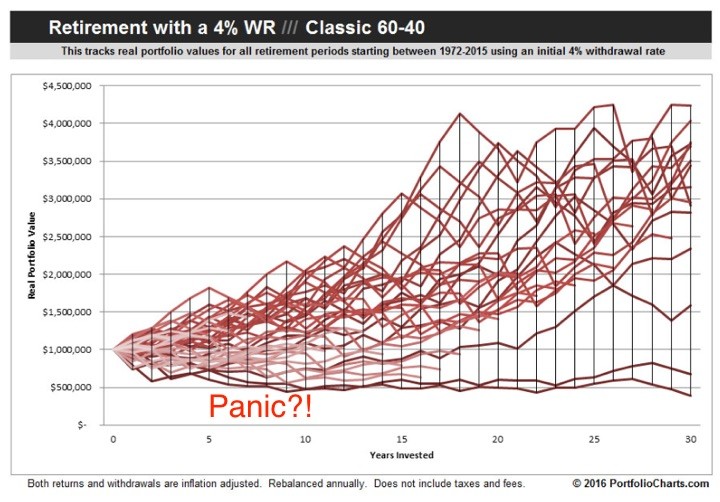

When you see the term safe withdrawal rate, it almost always refers to how much money you can safely withdraw from an investment portfolio each year without running out of money. Usually, this number is set during the first year, and is adjusted annually for inflation. The key phrase is “without running out of money”. You could start out with a $800,000 dollars, but as long as you end with at least $1 and never drop below zero, you’re considered “safe”. In the real world, having your portfolio nosedive while you’re still relatively young may cause you to panic prematurely.

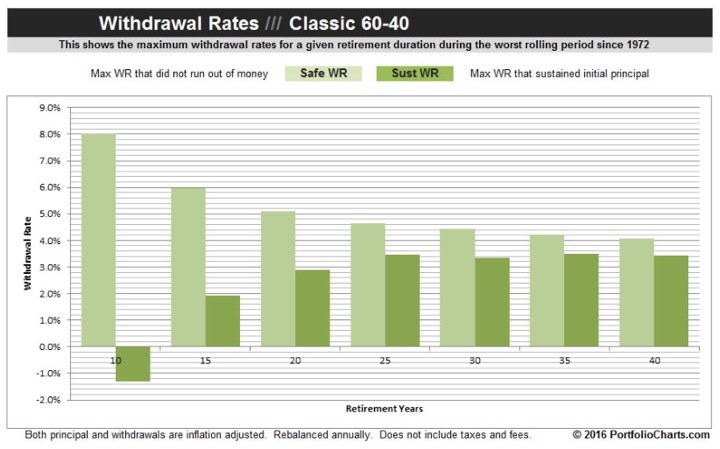

Since I last mentioned PortfolioCharts.com, the creator Tyler has released a new tool called the Withdrawal Rates Calculator. It is quite cool, at least for an asset allocation geek like myself. You can enter your own custom asset allocation, and it will show both the historical safe withdrawal rate and the sustainable withdrawal rate. As defined there, a sustainable withdrawal rate is one where you must end the period with your initial principal amount, for example you must both start and end with $800,000 dollars.

Here are the results for the Classic 60/40 portfolio:

60% Total US Stock Market

40% Total US Bond Market

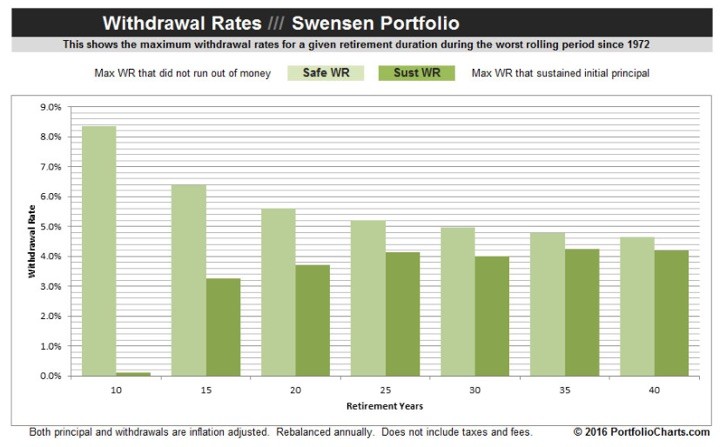

Here are the results for the Swensen Portfolio, on which my portfolio is loosely based:

30% Total US Stock Market

15% International Developed

5% Emerging Markets

15% 5 Year US Treasuries

15% US TIPS

20% US REIT

For the Classic 60/40 portfolio, the rough numbers for a 40-year period are 4% for Safe WR and 3.4% for Sustainable WR. For the Swensen portfolio, the rough numbers for a 40-year period are 4.6% for Safe WR and 4.2% for Sustainable WR. If you were to focus on the sustainable numbers, that’s a surprising result of 24% higher withdrawals with the Swensen portfolio (and other asset allocations do even better!)

Can you depend on these historical differences to persist into the future? I would be careful about looking at things too finely, as correlations are always shifting. However, I do prefer using the sustainable withdrawal rate number for my own early retirement planning, and I am thankful to have this tool to tinker with.

(You may also be interested to know that a 100% US stock portfolio, despite its higher historical average returns, has a slightly lower 30-year sustainable withdrawal rate that either of the options above.)

The Best Credit Card Bonus Offers – August 2024

The Best Credit Card Bonus Offers – August 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - August 2024

Best Interest Rates on Cash - August 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

So, which allocation had the highest sustainable withdrawal rate?

From my browsing, Tyler made his own custom asset allocation called the Golden Butterfly which has a very high backtested sustainable withdrawal rate:

http://portfoliocharts.com/portfolio/golden-butterfly/

The danger with such Permanent Portfolio-style portfolios is that you really must trust in the power of low correlations over time. With gold and long-term treasuries, there will be very long periods of underperformance relative to stocks and short-term bonds. When these asset classes are quite unpopular for a decade, you must keep your head down and stay committed to the plan.

A very healthy dose of Small Value, in my quick experiments… I had 40 year sustainable withdrawals up around 7%.

Anytime I look at historical data and projections of any kind, I remind myself that past performance is no guarantee for future results.

The nature of total returns is that they are lumpy, inconsistent, and their amount and timing varies greatly. This is why I focus on the income portion, since it is a more stable portion of the TR. And the price component of total returns is more volatile than the change in fundamentals suggests – which could make it tough to live off your nest egg if things do not turn out your way like they did in 1966 – 1982 or 2000 – 2014.

The forward results will be somewhat dependent on the valuation at time of investment. For Example, Bonds have had a great run in the past, but are not expected to do more than 2% – 3%/year over the past decade. Stocks do look better than bonds today, because they have a higher dividend yield than the 10 year Treasury, and an earnings yield of something like 5%. ( dividends and earnings would likely grow over time too)

On the other hand, if we become the next Japan, a 2% – 3% return would be awesome. Perhaps this is where having noncorrelated assets ( stocks and bonds) could strengthen a portfolio.

Very good points!

I’ve always kept the 4% rule in the back of my mind, but I’ve never really been comfortable with it either.

If you look back historically, too many times, you see periods of massive selloff. If you happen to run into one of those periods early in your withdrawal period, you may never recover.

I am more comfortable with the income approach. Although I would recommend buying dividend stocks and bonds individually rather than buying through a fund.

Jonathan – does it makes sense to create the Swensen portfolio in pre-retirement years? It seems like a perfect retirement portfolio. Are you being too conservative by creating this portfolio now for yourself?

Good article overall. Thank you.

I don’t think a 70% stock portfolio is necessarily “too” conservative for anyone, depending on that person’s specific situation and needs.

Got it. I miscalculated the equity portion. Great article!

Thanks for sharing, I hadn’t seen this tool before. I like the comparison between sustainable withdrawal and safe withdrawal, and it’s interesting to see that the gap is narrowed drastically with a longer time horizon.

I’ve always been fascinated by PortfolioCharts, amazing tools, FREE, and now even better with the addition of “Withdrawal Rates”! As others have said, my concern is using past performance. Given today’s CAPE ratios, I think a more conservative view is prudent. I’ll be retiring early in 1-2 years (at age 54-55), I’m using 3% as an assumed withdrawal rate in my cash flow model. I’ll monitor annually and adjust. One point to stress, ANY withdrawal strategy should be revisited annually, based on actual market performance in the preceeding year. I’ll plan on revisiting the PortfolioChart tool annually. Thanks for making us aware!

Does anybody know much about social security benefits. I was told that a retiring spouse cannot get more than 1/2 of the total benefit than the larger amount from the other spouse. Ex: if one spouse gets $2500/month the other will max out at $1250/month. Is this correct?