For the past several months, we’ve been using a crude but effective way of tracking our overall spending each month. The basic idea is that we only put the amount of money we actually want to spend into our primary checking account, and then pay all our bills out of that account. Everything else goes directly into either a high-yield savings account, an IRA/401k/403b, or a brokerage account.

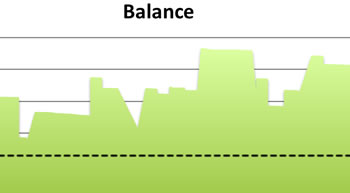

Add in an appropriate buffer balance to avoid overdraft fees, and ideally our bank balances should look something like the sinusoidal line below:

So what is a proper spending goal? I would recommend looking at your current spending levels first, and then deciding on a numerical goal of say $X,XXX per month.

Or, for us, we decided that we wanted to live on only one of our incomes (the lesser one). So only that paycheck is direct deposited into our “spending” account, minus retirement account contributions. We pretend this account is all we have, carefully watching that the balance does not go below the buffer level. (We are signed up for e-mail alerts if we do hit that barrier.)

In addition, we note the high and lowest balances for the last 30 days. This helps keep a rough trend that we are headed in the right direction. Here is an graph made from the actual daily balances of our checking account from the last few months:

Benefits

The biggest benefit is that because it is so simple, we actually do it! By keeping all our other transactions separate, it really helps us pretend that we only have a certain income. It’s a reflex that when I see the balance get low, I get nervous and start changing my spending behavior. If we eat into the buffer one month, then the next month we have to dig our way back.

Also, looking at the big picture in this way prevents the cheating that sometimes happens when we have a large unexpected expense like a plane ticket to visit sick family or a surprise car repair. It’s so easy to ignore that chunk and say that we still did okay our regular categories like “Gas” and “Groceries”. And we all have unexpected expenses, right?

Drawbacks

This system really works best for those that already have a basic idea of what they spend each month, and aren’t looking for drastic changes. It does not provide any deep analysis, such as identifying areas to cut back. We’ll have to do that separately, or use another budgeting system.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

This is what I have been doing for 10 years. It really is a great system. I call it Relative Scarcity. You create a situation of pseudo scarcity so your spending does not spiral up to meet your income. We find that we also reign in spending when the checking account gets low.

Once you are used to living in relative scarcity, you are not as concerned with real scarcity (such as a loss of one income) because it would not prompt many changes in your lifestyle.

I really enjoy your blog. Best of luck to you.

I use a similar system; the toughest part is factoring in bills which are pending, but not yet paid.

I set all of my bills are to auto-pay on the 15th and the 30th (the same day my paychecks come in); for the most part, this nets out your cash balances, so that there’s no ‘fake money’ in the form of accounts payable. I then transfer any cash over the buffer amount to savings on the 1st, after all the checks have cleared.

I do this exact approach, but use Quicken’s cash flow forecasting for this. If you schedule all of your deposits and bills you can easily forecast your cash flow. Makes it very easy to make adjustments to avoid any deficit spending in any particular month.

Chris beat me to it. I use MS Money’s cash flow to track this.

How do you account for bills that you don’t have every month such as Car Insurance (6th mth premium as example)? What amt of $’s do you currently use as a buffer.

I do the same basic thing, however, I make a few additions:

– In addition to the “actual balance” chart, I have a “rolling average” chart that’s averages a ~1 month window centered around the date for which I’m generating the average. This quite handily smooths the cyclic nature of the data and gives me a nice trend line 🙂

– I also have daily and rolling average charts that factor in my savings account, so that I can see now my cash balance as a whole is doing. This is useful because I’m trying to build up a small “I need a house downpayment” fund (I’m 27 … it’s time :\ ), and it really doesn’t matter where the money is for that.

– I extend my spreadsheet several months into the future. This allows me to see if a major purchase *now* will cause me to drop below my “buffer” in the future. I have my spreadsheet set to highlight cells in the daily balance column that fall below a couple of key levels.

Yes, this is mostly our method as well. I am less concerned what we spend on each category as long as the total does not exceed a set amount. This allows for a lot of flexibility (one month we spend a lot on dining out; we cut back on other stuff. When gas is high we cut back on other things, etc.) I much prefer this method to strict budgeting.

Before kids and dropping to one-income we lived off my paycheck entirely. My spouse’s money went to savings, retirement, investing. We actually spent less than my income in the end so every 6 months or so I would move the accumulating excess over to savings.

On one income we do things a little differently. We track everything in Quicken and transfer a set amount to savings and retirement every time I get paid. But overall the concept is the same. We live with what is in the checking account. The nice thing about Quicken is if money does feel tight or we are struggling we can pretty quickly see where any problems are or where we need to cut. We spend every penny in checking these days though. We keep a $1k buffer in a linked savings account.

I’ve been doing this for a few years, tracking it with Microsoft Money. Has worked well for my family.

My wife and I do something similar. I’m self-employed and our income can really vary throughout the year, so we have set up what we call our “slush fund” which is just a savings account. All income that comes in from anywhere goes into the slush fund. Then twice each month we take out a chunk of the slush fund for what we will need until the next withdrawal.

Everything else stays in the slush fund and it just continues to build. It’s kind of a way to pay ourselves an artificial salary and at the same time stay at least a month ahead on our bills.

It works for us! Thanks for sharing what works for you!

This is great … we’re actually planning on doing this. How did the transition period work out for you? Honestly while I want to do it, I’m a little gun shy you might say – scared of bouncing checks.

I considered moving it into a linked savings account in the same bank (immediate transfer priveleges vs. a couple of days transfer period form another bank). Even that is a bit scary for now. So far I’ve been putting everything in the same checking account, making sure that I have enough $ to pay off everything and then every 3 months, trasferring a chunk to my savings. Any advise?

My husband and I been doing this for the last 5 years with great results. I’ve heard it called “paying yourself first,” but I like “using the Force” better. 🙂

How does this method account for inflation? Stuff we buy at Home Depot, for instance costs a lot more this year than a couple of years ago. A box of lightbulbs costs almost double what it did about 3 years ago. And you know, you can’t cut back on lightbulbs!

I do this too and it works well. Plus with EFTs, you have a several day delay in getting the money from your high yield savings account. That helps cool down any spending urges.

If your spending is under control, why not pass as many dollars as possible through a credit card? You never have to worry about over-drafting, as long as your limit is high enough. That’s a much easier call to make than setting a “buffer” amount.

Granted, a few impulse buys can quickly cancel out any cash back or rewards points. If you’ve go to spend the money anyway (groceries, bills, etc), pick up some free stuff along the way.

How do you decide on the size of your buffer?

I have been doing a variation of this since 1994. I also agree that this approach is best for people that already have their finances under control, not for someone with spending issues.

Mike – the way I came up with my buffer depended on where I was in my life. Right now, my buffer is $1,000. That’s my deductible for my homeowner’s insurance. I know that I ALWAYS have that available in case I need it right away. Then I am only a day or two away from an ACH transfer for anything else that might come up.

AnakM – that’s why the buffer is there. When I first started, I went below my buffer number several times. Now, I can’t remember the last time I did. In fact, my wife and I even kicked around the idea of reducing it, but the interest earned on $1000 is not enough to override the peace of mind we get from knowing it’s there if we need it.

Good questions on the buffer. I don’t think there is any one answer. And it can be changed at any time. It all depends on your situation. For some people a $1,000 buffer is huge, while others would want a $5,000 buffer. Setting it too big runs the risk of spending too much and not really noticing it.

If you’re starting out, you could set it high to begin with, and then lower it with time.

Randy – We do put all charges we can on credit cards to earn rewards and to simplify tracking, we just pay the credit card bills from the checking account. As long as you keep an eye on irregular purchases, things have worked out for us. The big drops in our charge are credit card bills, the smaller ones are probably ATM withdrawals or smaller checks/utility bills.

rmw, divide by six.

i looking into living on one income.

wife and i both bring home $2200 a month.

mortgage ($1200), car insurance ($83), gasoline ($250), natural gas ($65), cable/internet ($60), cell phones ($75), electric ($50), food/household ($350) = $2100.

guess one of us needs a higher paying job.

I don’t have Quicken or MS Money and and don’t really care for online spending and tracking websites. I see that as a major risk of privacy breach.

I do very well with an Open Office (free) Calc spreadsheet that I start once a year and plan ahead most of my income and expenses for the year. Once you do this it’s easy to duplicate for next year and make just minor adjustments.

This is my Cash Flow.

It includes all cyclic income (salary) and expenses (bills) but also once a year payments like car insurance, excise, vacation budget, trips, etc.

I have as well savings, both in a savings account and also retirement (Roth). The only thing that I do not track are 401k contributions.

Besides cash flow planning, I built also alarms into the spreadsheet to tell me if at any point during the year I will get below the threshold, it shows me the categories that I spend and also the typical spending pattern (i.e. groceries are more often on Wednesday than on Fridays, etc).

I can see in advance when I have to reduce the contributions to the savings account so that I have the money available for car insurance or that planned trip. Also, it has a note one month in advance to start looking for insurance quotes and see if I get a better price.

My buffer is $1,000 in a savings account that is linked to the checking account. I too agree that the missed APY is totally worth the peace of mind.

I recommend that the first year you just watch what you spend and not try to make too many improvements. Once you collected the data for the year then you can make plans for the whole next year as you have a pretty good picture of all your spending.

Free pancakes at IHOP on Feb. 24 should provide an adequate buffer.

Umm Jonathan;

What are these: surprise car repair?

I mean, your car is going to break down. It’s not a matter of if, just a matter of when. Given the cost of car repairs and the fact that many people need the car to get to work, it seems reasonable that car repairs should have their own “fund”.

A car breakdown isn’t really an “emergency”, it’s more of an “eventuality”. And for people living on a median income, you can’t afford to just “buffer” a $1,500 car repair. It really needs a separate holding spot.

Hey dude, how realistic is this??

You’re making 10k+ a month and you already save most of it. I would like to see someone who is living on the edge, really needing to budget their money. This is like experience Africa on a safari.

Wow, I just found this blog and it’s great!

I’ve never actually budgeted this way, though what I’ve done in the past is to say I have to save x amount each month, and I’ll cut where I have to (eating out, movies, clothing, etc.) to meet my monthly target. This is kind of dangerous, because I have not adjusted my savings levels up for a while, nor have I made a conscious effort to do better.

Thanks again for this topic!

-FinancePhi

asda – ha, good point.

our blogger here is not in terrible financial shape.

of course, he is doing a lot to put himself in a better position than many people with equivelant (i cant spell) income…

someone living on the edge probably has 3 kids and 2 jobs… they dont have time to post to their ultra nerdy blog…. (which I enjoy reading by the way).

haha yeah asda, you’re right 🙂 But I do like this blog.

The rolling average is interesting. Some “additional” payments like homeowners association fees every Jan and car insurance skipping the 6th month can be predicted. Higher electric bills in the summer … hmmm I need to do some serious homework for this to work!

I do this too. One of the best things about ING Direct is that you can open multiple savings accounts in addition to your electronic checking account. I use the electronic checking account to pay monthly bills and contribute a set amount of my pay each month. The other nice thing about ING is that they allow a temporary $500 checking overdraft with really no fee (there is interest if you allow it to remain in the red).

I just keep everything else in my ING savings, and then for any unexpected expenses I can quickly and easily transfer the money into my checking.

@rmw – I divide the total amount I pay to my insurance company every 6 months, divide it by 6, and put that amount in a separate savings account. This way, I earn interest on it, but at the same time when the insurance payment time comes, I don’t feel like I need to find a big chunk of money somewhere.

AnakM, and those talking about “unexpected” expenses — That’s why I run my charts out as best I can 6+ months in the future; I go far enough to make sure that the next few big non-monthly expenses (car insurance, charitable donations, etc) are included on the chart. If I see that my daily balance drops below my “oh crap” zone (~$4-$500 ish) or my rolling average drops below my buffer (~$1000-$1500), I’ve got six months to either spend less or pack on as much overtime as my employer will let me (and right now, that’s basically as much as I can stand to work). As far as major unexpected expenses — my car dropping its transmission all over the road, a computer dieing, etc., I take a two pronged approach:

1) Hopefully they fall within the buffer, and after the expense, I can re-build

if not:

2) Put them on the credit card, and an ACH transfer from my high-yield account can be done before the bill is due (I’m of the “pay it off every month” mindset).

Granted, 2) is an ugly option, but the high-yield account exists only for the purpose of a house downpayment, and I’m in no hurry (I’m a singleton, so I don’t have a wife begging for a house :). Right now I’m putting ~$1000/month into that account, so most emergencies could be covered just by skipping a month’s contribution.

That being said, the “run everything through the credit card” approach provides ~1 month of delay between expense and payment, and this alone has allowed me to be able to adjust my spending & working enough to cover most emergencies I’ve faced without having to dig into my savings/stocks/whatever.

I have an extremely variable income (can be 3 times what I spend for months and 0 for months, its pretty crazy for budgeting, but averages out much better than I could do in a steady paying job) so I’ve gravitated to this kind of system of dividing my income account from my spending account over time (If I ever looked at what I make in a good week, month, or even year as what I can spend for that period, then I’m gonna be in trouble soon enough). All my income is deposited into my money market account. At the beginning of the year, I reset my buffer in my checking account to one month’s expenses. This is not a true buffer, but more of an expected average monthly low balance I hope to maintain over time. I then get the same X dollars deposited into the checking from the MM every month.

I like this because I’m not spending any time at all planning/worrying about irregualr expenses, they are all averaged in to the budget over time (there are few unexpected expenses if you’re realistic – an emergency room trip to the hospital every few years(when you have kids), a car needing serious work once a year (when you have 2), etc. are all irregular expenses in my mind, not unexpected). Some months I go below my average low, but that usually just means I had to pay some irreg/unexp expenses that month and it will balance out the next. At the end of the year I reset my buffer and start over. If there is more than the buffer still in there, I beat my budget, if there is less, I overspent. I then look at my MM, any amount it has grown to over a years’ expenses gets invested.

Open up a checking and savings account at Ally Bank. All Bank automatically transfers money from savings to checking if there is not enough money on the checking account. There is no fee for the overdraft protection. I keep only small amount in checking and keep the rest in the savings account that pays one of the highest savings rate in the nation.

I like this method, and we use it as well. The only danger is when you use a credit card to make purchases, it’s easy (especially for other family members) to cause you to exceed your “limit” for the month.