As an early adopter and IPO participant of LendingClub, I was disappointed to read about their recent happenings. The major financial media outlets have been covering it closely, with summary-style articles from the NYT here and WSJ here. This is my condensed understanding of the situation.

- On Monday, May 9th, LendingClub abruptly announced in a “by the way” manner that their celebrity CEO Renaud Laplanche had resigned. (His only other alternative was to be fired.) Three other high-level executives were also fired.

- LendingClub improperly sold $22 million of loans to an institutional investor that did not meet the investor’s standards. The origination dates were changed some loans in order to make the loan meet the investor’s specifications. Other loans had other features of their disclosures altered and/or misrepresented. LendingClub later bought the loans back for full price.

- LendingClub as a company decided that it was good idea to invest in outside investment funds that own… LendingClub notes. Can you say conflict of interest? Will the fund get better access to loans? LendingClub was supposed to be the middleman, so why are they quietly taking on risk as the lender?

- For one of these funds that LendingClub invested in, then-CEO Laplanche had a personal stake which he did not disclose. Director John Mack also had a personal stake, which apparently was disclosed. So now LendingClub as company is investing in outside funds that invest in LendingClub notes and are (shhh) partially owned by their CEOs and Directors?

- On Tuesday, May 17th, an SEC filing disclosed that LendingClub received a grand jury subpoena from the U.S. Department of Justice (DOJ), which indicates they will be subject to additional investigations as well as potential lawsuits in the future.

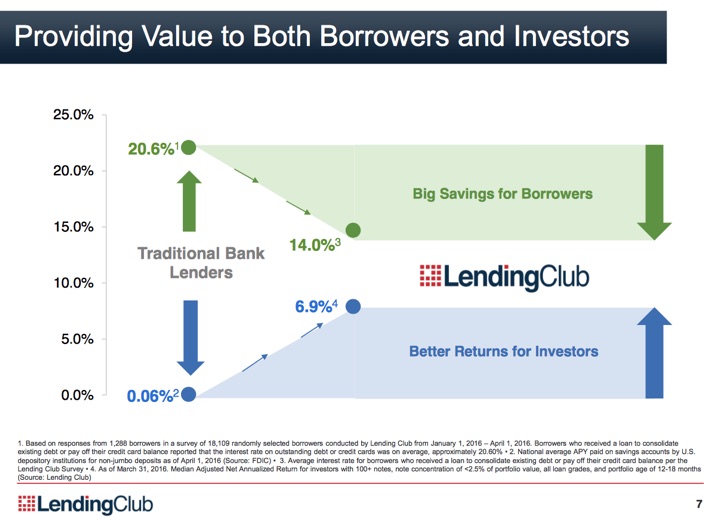

When LendingClub started out a peer-to-peer lender, the grand idea was that the spread that banks got between taking deposits and making loans would be made thinner, with the difference going to individuals, NOT Wall Street. Individual borrowers got loans at lower rates. Individual lenders got paid higher interest. An illustration from their own materials:

In opinion, LendingClub then became too aggressive in their chase to stay on top as the “industry leader”. The majority of their notes are now sold to large, institutional investors, not individuals. But this also means risk if the big investors decide to stop buying their big chunks of loans. In turn, they loosened their standards and became willing to take on additional risk by essentially buying their own loans if demand drops. You can decide if it was coincidence that they started fudging dates and other “little stuff” to keep things going.

Finally, another way that LendingClub was aggressive is that they pursued a way to allow them to sell notes in all 50 states called a “blue sky exemption”. However, by doing it this way, they could not create a “bankruptcy remote vehicle” where individual note-holders were protected in case of a LendingClub bankruptcy. This is another way where the individual investor is not their #1 concern. Here’s the official statement from the LendingClub website (emphasis mine):

When you invest in a Note, you are investing in an obligation of Lending Club. Borrowers make payments on their loans to Lending Club, and in turn, Lending Club distributes payments to investors in the Notes net of fees. If Lending Club were to go out of business, investors may not receive the full amount of payments due and to become due on the Note, or such payments may be delayed as bankruptcy or other proceedings make their way through the courts.

We have taken steps to ensure continuity to protect investors and borrowers if Lending Club were to go out of business. For example, we have executed a backup and successor servicing agreement with Portfolio Financial Servicing Company (“PFSC”). Under this agreement, PFSC stands ready to service borrower loans.

Following five business days’ prior written notice from us or from the indenture trustee for the Notes, PFSC will begin servicing the loans. If the underlying loans are determined to be part of Lending Club’s bankruptcy estate, PFSC may not be able to make payments on the Notes. If our agreement with PFSC were to be terminated, we would seek to replace PFSC with another backup servicer.

Here’s another take by Kaddhim Shubber in a FT article.

The short answer is that yes, there is a chance that if LendingClub files bankruptcy that investors individual notes may lose their principal and/or interest if other creditors claim priority over those assets. The question is determining the probability of this happening.

Why an acquisition is much more likely than bankruptcy. If I am reading their recent filings correctly, LendingClub has over $800 million in cash along with little company debt (other than the notes created to be sold to outside investors). Their company value dropped to as low as $1.5 billion this week, which means the company itself could technically be bought for $700 million. (Less than a year ago, the company was worth over $5 billion.) A mega financial institution like Wells Fargo or J.P. Morgan Chase could easily buy the entire company (and keep servicing the notes) if the value dropped further. I believe the LC platform still has real value, but if trust erodes further then it may need the backing of a bigger name. Then we’d be full-circle, the former peer-to-peer lender now owned by Wall Street. I’m not saying such an acquisition is likely, but instead something that would happen well before bankruptcy.

At the same time, unlikely is not zero. I would not put any more than 5% of my net worth into LC notes. I had great hope for LendingClub, but also never put more than a few percent of my net worth into LC notes. Here is my post on liquidating my LendingClub notes on the secondary market. I have no position in LC stock either, as I sold my shares immediately after the LendingClub IPO. I’m just watching this one from the sidelines.

The Best Credit Card Bonus Offers – August 2024

The Best Credit Card Bonus Offers – August 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - August 2024

Best Interest Rates on Cash - August 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Jonathan – Wow, this is pretty shocking. A bank would never lend funds to a third-party through an intermediary. I read the FT article and if it’s true that the loans really go from Lender —> Lending Club —> WebBank —> Borrower, I don’t know how they got away with that. As you said, at a minimum you’d think they would have set up a bankruptcy remote special purpose vehicle for the purpose of routing the loans outside of their estate in a possible bankruptcy.

If loans are flowing through Lending Club, lenders are inadvertently taking on Lending Club bankruptcy risk and should be compensated by receiving a higher interest rate for the additional risk exposure. Yet, I doubt they are.

Kind of undermines the “peer to peer” marketing catchphrase when it’s really “peer to Lending Club to WebBank to peer” lending.

I believe the industry quietly shifted from calling themselves “peer to peer lending” and switched to the new term “marketplace lending” for that reason. It is no longer truly peer to peer, although it was when it started.

Interesting. Does the bankruptcy clause apply to the borrower as well? Should we be loading up on LC loans 🙂

Don’t worry, someone will always be on the other end making sure you make those loan payments. 🙂 Since they are unsecured loans like credit cards, their only threat would be to damage your credit score, anyway.

Yeah. I was surprised by this as well.

That said… I dropped out I’d lending club after running an experiment with a few thousand dollars for a year.

Returns were good… but I really got nervous for a few reasons

1) it’s very illiquid. If you want to cash out… it takes YEARS.

2) It has high correlation but looks diverse. I saw a lot of references around A-D risk and how putting a bunch together reduces risk. That’s not quite true. It’s ALL consumer credit which is highly correlated when things go bad.

3) it’s a yield chasing target. I started seeing lots of blogs recommending it for high returns and low risk. Because CDs, bonds and stock returns suck…hey let’s push in! I just assume that makes an investment more expensive :).

4) I had no idea what would happen if something goes wrong. This is just me not understanding the investment area.

So when I combined those I had a yield chasing, illiquid investment I didn’t understand so… I passed. I suspect you’re right… a bankruptcy with huge default seems unlikely and I think the underlying idea is great… I just don’t understand it we’ll enough to be comfortable.

The secondary market for loans improves the liquidity aspect, although I’m not sure how good the sale prices are currently. But I agree it’s definitely a new asset class with a lot of unknowns about how it will react in adverse conditions.

I agree. And I think its a long term great asset class, but it’s in beta :).

The low liquidity makes me intuitively add much more riskiness. For example I think it’s way riskier than say, a vanguard emerging market small cap fund but less risky than a single small cap emerging market company. But I think too many people are treating it as closer to, say, VTI or VXUS but with WAY better returns.

So when I apply my own risk filter, even returns of 12% don’t justify a meaningful part of my portfolio and anything small enough to be safe isn’t that impacted compared to something like a small cap emerging market fund :).

I’ve only seen the “up” part of the curve and I like to see the “down” part of the cycle to get a better idea of what the volatility really is. Unknown volatility + low liquidity makes for scary scenarios.

But with fun, experimental money, that kind of stuff is fine I suppose 🙂

I’ve been happy with my performance on a whole since my other investment accounts have completely floundered the last couple years. However, this has scared me into pausing my automated investing and stopped contributing since they’re highly illiquid. If a brokerage were shady I could just sell and get the hell out but like someone mentioned, it takes so long to get out that I need to be conservative and stop all new activity to see where things go.

It’s probably a good time to invest right now with all the negative coverage.

If you want an interesting ride, buy some LC shares at under $4 and keep them for 5 years. 🙂

Actually I bought some yesterday.

I doubt they’ll survive the onslaught of lawsuits. Since they’re just the brokers an don’t have any assets I doubt they will find any buyers. (Refer to what happened to KCG)

Class action lawsuit has now been filed.

I had stopped investing in LC after 2 years. Sold all off in secondary market – choosing and keeping track of individual notes was a headache. Since it was all in taxable account it was non-trivial to correctly file.

Earlier this year LC was running a promo – if I invest $5k, I would get $500 bonus. I opened an IRA with the intention of funding 5k but hesitated since the promo sounded too good to be true. So glad I don’t have to deal with any extra headache now.