Good financial advice is hard to come by. There are so many variables, such that you have to find the balance between providing enough information, and making things digestible enough that peoples’ eyes don’t glaze over.

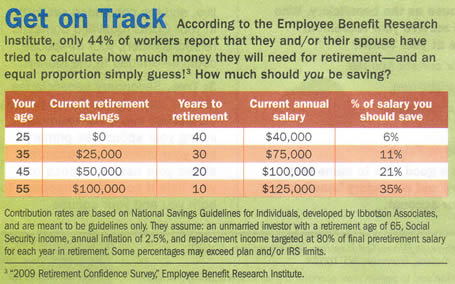

Check out this advice column found in the newsletter that comes in my 401k statement each month. Can you spot what’s missing?

There is no mention of what investment vehicle you should be sticking your money in, or even how much they estimate your future returns to be. Is it 100% stocks? 50% stocks/50% bonds? Orange juice futures? 6% returns? 12% returns? Who knows. Is this pre-tax or post-tax? Is it all in tax-sheltered accounts? Is my annual income supposed to rise as sharply as the chart seems to imply? I selfishly hope so!

Yet, I feel like this is what a large percentage of workers want to read. One impossibly simple chart that defines your retirement needs. So someone gives it to them. Maybe it gives them a general idea of where to start. But is a vague, possibly wrong answer better than guessing? I feel another poll coming on…

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Cosnider the source.

Hopefully, when you need advice, youhave someone in your circle of contacts that you can trust.

The chart references a study titled “National Savings Guidelines for Individuals.” Actually, the study is apparently titled “National Savings Rate Guidelines for Individuals,” but if you google either title you will immediately get the full study which contains all the assumptions.

Relating to this topic, I have been wondering lately if “generic” financial advice about lifecycle (varying with different ages in life)asset allocations is good to follow.

I read a lot in books such as Malkiel’s Random Walk Down Wall-Street and What Wall Street Doesn’t Want You To Know by Swedroe, and this type of information is included.

What’s everyone’s take on this?

It is interesting to see that it is suggested to save a smaller percentage of your salary early on and then increase it. That would appear to be counter to the law of compounding interest. When someone is young (25) they are not likely to have kids or a mortgage, they should put away much more than 6%, that money will grow much much faster over 40 years. It should be suggested to put away much more early on, and then re-assess.

Another thing that is missing is the “final goal”! What amount are you saving towards in this hypothetical? $1,000,000? That would seem a bit off considering that in 40 years that will not be enough. Also, will you retire at 65? Now the retirement age is 67, and will likely be increased to 70, so that should be accounted. How long will you live for? another 30+ years? How will you draw that money down?

Something is better than nothing, but in this case, it is just not well thought out.

OJs future does not look good…just some free advice.

Anything is better than nothing. All the people saving nothing are going to end up having to be supported by those who were responsible. And that’s not fair.

Hi Jonathan,

Can you do a review of the BAC merrill edge service where they are providing 30 free trade/month when you have 25K in assets in banking with them. i am thinking of transfer for sometime, but cant make a decision. i ve emergency reserve savings in Dollarsavings direct account earning 1.30%. see what do u think?

I look at it like this: I’ll give you basic, generic advice. If that advice interests you enough, you will ask me questions that will lead to me giving you more details. Part of it has to be on the person who needs the help.

I love the chart above. I looked at it and was able to make an immediate estimate for myself. Is it right on? Likely not. But I found it valuable. The harm would only be if I look, have a good idea of what to do, and then acting on it ruins me or puts me far worse off than if I had never seen it.

Thinking of a standard bell graph for the audience being communicated to, if you give advice for the 60% that makes up the center, you will in general be making a positive influence.

Most people don’t save for retirement at all… so any propaganda like this that can convince them to start is a step in the right direction!

I’ll bet that your 401(k) issuer simply had space to fill in its newsletter, and you’re the only person who bothered to read it. The unmotivated masses might glance at the chart, but they’ll think nothing beyond “Yeah, I need to save more”, a thought that will remain unacted upon like “Yeah, I should drink less” or “Yeah, I could lose a few pounds.”

I think this sort of generic advice does do more good than harm.

Telling people that they need to save for retirement is good advice. The exact amounts may not be the most accurate, but at least it gets people on a productive path.

And this advice is free, so at least you aren’t paying some self-proclaimed financial guru untold amounts of money for potentially damaging advice.

“It doesn’t matter, we’re all doomed anyway” – LOL

I chose “something is better than nothing” for reasons already stated by other posters.

I think it is valuable to encourage people to save for retirement. Saving is the most important thing; getting a good rate with low risk is a secondary question.

my guess would be by the age of 30 you should have at least $100,000 saved by 40 you should have close to $500,000 by 50 you should have close to $750,000 60 you should have over $1,000,000.

im not an expert but this seems reasonable.

I would think the initial intention of this type of breakdown is to spark interest. At that point it would be up to the viewer to decide weather or not they want to know more. I agree with some of the other comments here about anything that brings to light the need to start saving ASAP is a step in the right direction.

Great Article. Thanks for the info. Does anyone know where I can find a blank “Generic Personal Financial Statement” to fill out?