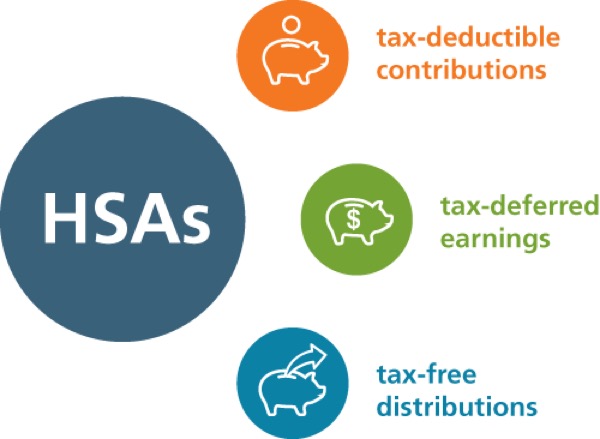

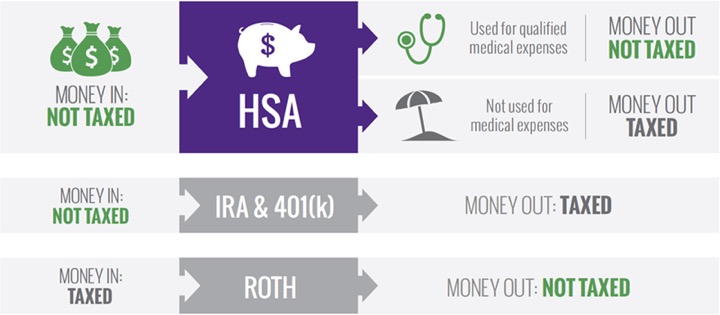

Updated for 2022. It’s open enrollment season, and there is better than a 50/50 chance that you will enroll in a high-deductible health plan. That means that you are also eligible to contribute to a Health Savings Account (HSA), which has triple-tax-free benefits: tax-deductible contributions, tax-free earnings growth, and tax-free withdrawals when used for qualified medical expenses (image source). This makes them better than even Traditional and Roth IRAs (image source).

Are you an HSA spender or HSA investor? As a spender, you contribute to the HSA, grab the tax-deduction, and then treat it like a piggy bank and spend it down whenever you have a qualified healthcare expense. You don’t have that annoying “use-it-or-lose-it” feature of Flexible Spending Accounts (FSA), and most offer FDIC insurance on your cash.

As an investor, you are trying to maximize the tax benefits of HSAs by contributing as much as possible, investing in growth assets like stocks, and then avoiding withdrawals until retirement. If you have the financial means, you would max out the contribution limits ($3,850 for individual and $7,300 for family coverage in 2022, slightly more if age 55+) and then pay for your healthcare expenses out-of-pocket instead of withdrawing from the HSA. You should keep a “forever” digital PDF copy of all your healthcare expenses. Technically, you can still withdraw the amounts of all those expenses tax-free at any time in the future, even decades later.

You can pick your own HSA provider, and some are much worse than others! Morningstar has updated their 2022 Health Savings Account landscape report (e-mail required). After reading through the entire thing, my take is that you really only need to consider the two best HSA plans: Fidelity HSA and Lively HSA.

Similar to IRAs, you don’t need to use the default provider that your employer recommends. As long as you are covered by an HSA-eligible health plan on the first of the month, you can open an account with any provider. From the Lively site:

My health insurance or employer is offering an HSA. Do I need to go with the option they provide?

No. Because an HSA is an individual account, you are free to choose whichever HSA provider you want to work with (e.g., Lively).

Source: “Publication 969 (2018), Health Savings Accounts and Other Tax-Favored Health Plans.”

In addition, you can transfer the balance in an existing HSA to another HSA provider at any time, even if no longer covered by an HSA-eligible health plan.

Fidelity and Lively HSA for spenders. Both have the least fees and a safe place for your cash. Others HSAs have maintenance fees, minimum balance requirements, and more “annoyance” fees.

- No minimum balances.

- No maintenance fees.

- No paper statement fees.

- No account closing fee.

- FDIC-insured cash balances.

Fidelity offers the best potential interest rate on cash via the Fidelity® Government Cash Reserves money market fund (FDRXX) as a core position, which currently pays more than their FDIC cash sweep option. Note that this money market fund is very conservative but is not FDIC-insured.

Fidelity and Lively HSA for investors. Both feature a low-cost way to invest your contributions for long-term growth:

- No minimum balance required in spending account in order to invest.

- Offers access to all core asset classes.

- Offers free self-directed access to ETFs, individual stocks, bonds, and mutual funds.

- Offers “guided portfolios” for automated investing.

Fidelity quietly offers the institutional shares of their Fidelity Freedom Index “target date” mutual fund line-up with a very low expense ratio of ~0.08%. It’s a bit confusing as you must choose the self-directed “Fidelity HSA” option to access this auto-pilot fund. The self-directed option has no annual fee and also includes access to ETFs, individual stocks, bonds, and mutual funds. Be aware that the Fidelity HSA sign-up page may try to steer you towards the different “Fidelity Go HSA” for guided investing, but that robo-advisor charges an annual advisory fee of 0.35% per year for balances of $25,000 and above (no advisory fee while your balance is under $25,000).

Lively also has similar “guided portfolio” robo-advisor option that charges a 0.50% annual advisory fee. Morningstar dinged Lively for this, but Lively also offers a self-directed brokerage window with Schwab. That means you can invest in any ETF with zero commissions at Schwab including building your own DIY portfolio using index ETFs, mutual funds, individuals stocks, or individual bonds. (Previously TD Ameritrade, but Schwab bought TD Ameritrade.) The Schwab brokerage option has no annual fee with a $3,000 minimum balance, otherwise if you are under $3,000 it costs $24 a year. If you already have your own financial advisor connected to Schwab, you can allow them to manage your HSA as well.

A simple Vanguard ETF portfolio might be 50% US Stocks (VTI), 30% International Stocks (VXUS), 20% US Bonds (BND). The total weighted expense ratio of such a portfolio would be less than 0.05% annually and fully customizable for the DIY investor. Both accounts can cost basically nothing above the expense ratio of the cheapest ETFs you can find – you really can’t ask for more than that!

Fidelity and Lively have the least amount of extra and/or hidden fees:

How do Fidelity and Lively make money then? Your employer has to pay a fee to HSA providers. It’s still much cheaper for them than your old full-price health insurance premium, of course.

Bottom line. Both Fidelity HSA and Lively HSA are excellent options for your Health Savings Account funds. If you want auto-pilot investing, the cheapest option is the Fidelity Freedom Index Institutional shares. Alternatively, Lively is an independent HSA provider with a modern feel and a good history of customer-friendly fee practices and service. DIY investors can use the Lively/Schwab brokerage window to invest in a mix of Vanguard or other index ETFs.

(Disclosures: I am not an affiliate of Fidelity, although I would if they had such a program. I am an affiliate of Lively and may receive a commission if you open an account through my link. Thanks for your support of this site.)

Tuesday, November 29th is Giving Tuesday 2022, an international day about giving support through charities and nonprofits by donating money or volunteering your time. In case you aren’t inundated with mailings already, this time of year is a big deal for charities, with 40% of donations occurring in the last six weeks of the year. Here are some ways you can “double your impact” with a matching donation.

Tuesday, November 29th is Giving Tuesday 2022, an international day about giving support through charities and nonprofits by donating money or volunteering your time. In case you aren’t inundated with mailings already, this time of year is a big deal for charities, with 40% of donations occurring in the last six weeks of the year. Here are some ways you can “double your impact” with a matching donation. Hope you had a nice Thanksgiving weekend! Enjoyed a little break before the holiday chaos begins. Here are a few low-hanging fruit that caught my eye as I jump back in. Must visit

Hope you had a nice Thanksgiving weekend! Enjoyed a little break before the holiday chaos begins. Here are a few low-hanging fruit that caught my eye as I jump back in. Must visit

Here’s a reader question that I found interesting regarding “low-tech” retirees:

Here’s a reader question that I found interesting regarding “low-tech” retirees:

Retirement income planning would be so much easier if you could buy a known amount of guaranteed lifetime income that automatically adjusted for inflation. However, the reality is that not a single insurance company in the entire world is willing to take on that long-term inflation risk. The only possibility left is to ladder inflation-linked bonds (TIPS) so that each year you would cash out some bonds and interest to create your own DIY inflation-adjusted income.

Retirement income planning would be so much easier if you could buy a known amount of guaranteed lifetime income that automatically adjusted for inflation. However, the reality is that not a single insurance company in the entire world is willing to take on that long-term inflation risk. The only possibility left is to ladder inflation-linked bonds (TIPS) so that each year you would cash out some bonds and interest to create your own DIY inflation-adjusted income.  The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)