Walmart+ membership gets you the following perks:

Walmart+ membership gets you the following perks:

- Free next-day and 2-day shipping from Walmart.com (no minimum purchase).

- Free same-day delivery of cold Groceries & more from your local Walmart ($35 minimum purchase). Where available.

- Scan & Go in-store. Use the Walmart app to scan barcodes as you shop in-store and skip the cashier line.

- Save 5 cents per gallon on fuel at over 2,000 Walmart, Murphy USA and Murphy Express fuel stations. You also get to access member pricing at Sam’s Club fuel stations.

There is a free 15-day trial, and the membership retail price is $98 per year (or $12.95 per month). Right now, there are two ways to save over 75% off that $98 annual membership:

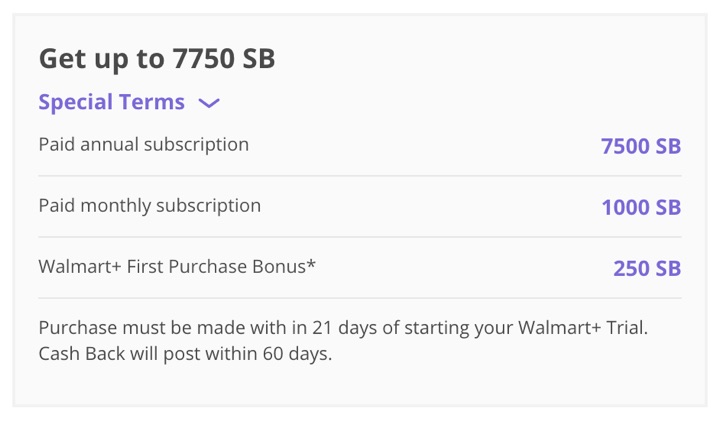

Swagbucks $75+ back. Search for “Walmart+” on the Swagbucks rewards site, and you’ll see they are offering 7,500 Swagbucks on a paid annual subscription, plus 250 Swagbucks on your first Walmart+ purchase. Purchase must be made with in 21 days of starting your Walmart+ Trial. Cash Back will post within 60 days. There is also a $10 new member bonus via Swagbucks referral link.

7,500 Swagbucks can be redeemed for at least $75 in Amazon gift cards (or similar).

MyPoints $75+ back. Search for “Walmart+” on the MyPoints rewards site, and you’ll see they are offering 12,000 points on a paid annual subscription, plus 500 Swagbucks on your first Walmart+ purchase. Purchase must be made with in 21 days of starting your Walmart+ Trial. Cash Back will post within 60 days. There is also a $10 new member bonus via MyPoints referral link.

12,000 MyPoints can be redeemed for at least $75 in Amazon gift cards (or similar).

Both Swagbucks and Mypoints are now owned by the same parent company, and I have cashed out of both without issues recently. (They also recently acquired Upromise.)

While it seems that Robinhood and Gamestop are officially the new gambling version of a multiplayer online video game (

While it seems that Robinhood and Gamestop are officially the new gambling version of a multiplayer online video game ( Did you know there was an iPhone app called

Did you know there was an iPhone app called

An uncomfortable fact of personal finance is that you don’t necessarily “pay for what you get”. When a bank offers “Free Checking”, it means “we won’t charge you a monthly fee but we’ll get our money from overdraft charges, ATM fees, and more”. For example, US banks charged their customers over

An uncomfortable fact of personal finance is that you don’t necessarily “pay for what you get”. When a bank offers “Free Checking”, it means “we won’t charge you a monthly fee but we’ll get our money from overdraft charges, ATM fees, and more”. For example, US banks charged their customers over

Alliant Credit Union, one of the top 10 largest US credit unions by assets, has teamed up with Suze Orman to promote their new

Alliant Credit Union, one of the top 10 largest US credit unions by assets, has teamed up with Suze Orman to promote their new  I know I’m a bit late on this, but after reading several media articles, here again is my curated collection of highlights and perhaps overlooked items that might be worthy of additional research.

I know I’m a bit late on this, but after reading several media articles, here again is my curated collection of highlights and perhaps overlooked items that might be worthy of additional research.

Updated for 2021. Here is the second part of my big list of free consumer reports from over 50 different reporting agencies. The first part included your

Updated for 2021. Here is the second part of my big list of free consumer reports from over 50 different reporting agencies. The first part included your  Here’s my monthly roundup of the best interest rates on cash for January 2021, roughly sorted from shortest to longest maturities. I track these rates because I keep 12 months of expenses as a cash cushion and there are many lesser-known opportunities to improve your yield while still being FDIC-insured or equivalent. Check out my

Here’s my monthly roundup of the best interest rates on cash for January 2021, roughly sorted from shortest to longest maturities. I track these rates because I keep 12 months of expenses as a cash cushion and there are many lesser-known opportunities to improve your yield while still being FDIC-insured or equivalent. Check out my  Instead of focusing only on

Instead of focusing only on

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)