If you like hearing Warren Buffett and Charlie Munger talk at the Berkshire Hathaway (BRK) annual meeting, you should also watch or listen to Charlie Munger at the Daily Journal (DJCO) annual meeting. DJCO is his personal pet project, and I feel like he lets loose more at this meeting than at BRK. For 2019, CNBC broadcast the entire 2-hour Q&A session online. Latticework Investing generously shares a full transcript as well. I choose to listen to this over any finance-related podcast.

Here are my personal notes and highlights:

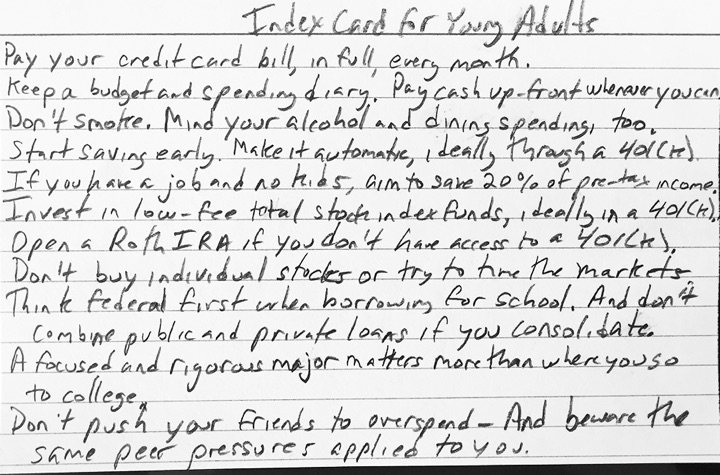

Think for yourself.

[…] my definition of being properly educated is being right when the professor is wrong. Anybody can spit back what the professor tells you. The trick is to know when he’s right and when he’s wrong. That’s the properly educated person.

Index funds have become more and more successful for a simple reason. The evidence is getting stronger over time that they provide better long-term performance due to lower costs and better tax-effeciency.

Another issue of course that’s happened in the world of stock picking, where all this money and effort goes into trying to be rational, is that we’ve had a really horrible thing happen to the investment counseling class. And that is these index funds have come along and they basically beat everybody. And not only that, the amount by which they beat everybody is roughly the amount of cost of running the operation and making the changes in investments. So you have a whole profession that is basically being paid for accomplishing practically nothing. This is very peculiar. This is not the case with bowel surgery or even the criminal defense bar in the law or something. They have a whole profession where the chosen activity they’ve selected they can’t do anything.

[…] I don’t have any solution for this problem. I do think that index investing, if everybody did it won’t work. But for another considerable period, index investing is going to work better than active stock picking where you try and know a lot.

If you are trying to beat the indexes, you need LESS diversification, not more. Wait for a few fat pitches and don’t hesitate to swing. This isn’t as widely known, but Munger’s personal portfolio is roughly 1/3rd Berkshire Hathaway stock, 1/3rd Costco stock, and 1/3rd invested in Li Lu, an investment manager based in China.

But the whole trick of the game is to have a few times when you know that something is better than average and to invest only where you have that extra knowledge. And then if you get just a few opportunities that’s enough. What the hell do you care if you own three securities and J.P. Morgan Chase owns a hundred? What’s wrong with owning a few securities?

[…] So the whole idea of diversification when you’re looking for excellence, is totally ridiculous. It doesn’t work. It gives you an impossible task.

Now at a place like Berkshire Hathaway or even the Daily Journal, we’ve done better than average. And now there’s a question, why has that happened? Why has that happened? And the answer is pretty simple. We tried to do less. We never had the illusion we could just hire a bunch of bright young people and they would know more than anybody about canned soup and aerospace and utilities and so on and so on and so on. We never had that dream. We never thought we could get really useful information on all subjects like Jim Cramer pretends to have. (laughter) We always realized that if we worked very hard we can find a few things where we were right. And that a few things were enough. And that that was a reasonable expectation.

Avoid any pitches that promise easy money from stock-picking. Penny stocks, day-trading, trends, charts. All of them.

Then if you take the modern world where people are trying to teach you how to come in and trade actively in stocks. Well I regard that as roughly equivalent to trying to induce a bunch of young people to start off on heroin. It is really stupid. And when you’re already rich to make your money by encouraging people to get rich by trading? And then there are people on the TV, another wonderful place, and they say, “I have this book that will teach you how to make 300 percent a year. All you have to do is pay for shipping and I will mail it to you!” (laughter) How likely is it that a person who suddenly found a way to make 300 percent a year would be trying to sell books on the internet to you! (laughter) It’s ridiculous.

Have modest expectations in stock market returns.

Well, my advice for a seeker of compound interest that works ideally is to reduce your expectations. Because I think it’s going to be tougher for a while. And it helps to have realistic expectations. Makes you less crazy. I think that…you know they say that common stocks from the aftermath of the Great Depression, which was the worst in the English speaking world in hundreds of years, to the present time may be an index that’s produced 10 percent. Well that’s pre-inflation. After inflation it may be 7 percent or something. And the difference between 7 and 10 in terms of its consequences are just hugely dramatic over that long period of time. And if that’s 7 in real terms, but achieved starting at a perfect period and through the greatest boom in history, starting now it could well be 3 percent or 2 percent in real terms. It’s not unthinkable you’d have 5 percent returns and 3 percent inflation or some ghastly consequences like that. The ideal way to cope with that is to say, “If that happens, I can have a happy life.”

Be very careful about who you chose to partner up with in your life.

We all know people that are out married, I mean their spouses are so much better. Think of what a good decision that was for them. And what a lucky decision. Way more important than money. A lot of them did it when they were young, they just stumbled into it. Now you don’t have to stumble into it, you can be very careful. A lot of people are wearing signs, “Danger. Danger. Do not touch.” And people just charged right ahead. (laughter) That’s a mistake. Well you can laugh but it’s still a horrible mistake.

On becoming rich.

This business of controlling the costs and living simply, that was the secret. Warren and I had tiny little bits of money. We always underspent our incomes and invested. And if you live long enough you end up rich. It’s not very complicated.

“If it’s trite it’s right.”

I think personal discipline, personal morality, good colleagues, good ideas, all the simple stuff. I’d say, if you want to carry one message from Charlie Munger it’s this, “If it’s trite it’s right.” All those old virtues, they all work.

My general idea is there’s no point in fretting too much about what you can’t fix. It’s a big mistake to fill yourself with resentments and hatreds and so on. It’s such a simple idea but so many people ruin their lives unnecessarily. Envy is such a stupid thing to have because you can’t possibly have any fun with that particular sin. Who in the hell ever had any fun in envy? What good could envy possibly do for you? And somebody is always going to be doing better than you are. It’s really stupid. So my system at life is to figure out what’s really stupid and avoid it. It doesn’t make me popular, but it prevents a lot of trouble.

I’m never really sure what to call it, but Marcus (formerly Goldman Sachs Bank) is offering a $100 bonus if you deposit $10,000+ in new funds into their online savings account within 10 days of enrollment at this special offer page. You must enroll by 11:59pm EST on 3/18/19 and maintain the new $10,000+ deposit for 90 days. They will deposit $100 into your account within 14 days, after those 90 days (got it?). Both new and existing customers are eligible, which is nice.

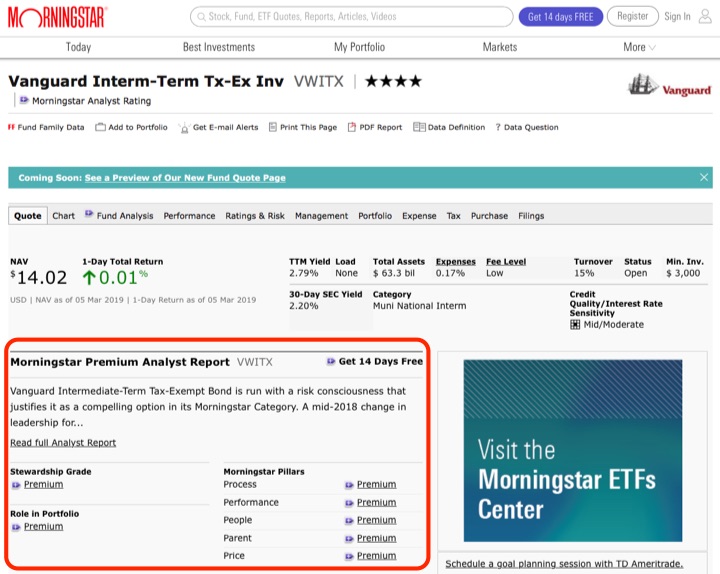

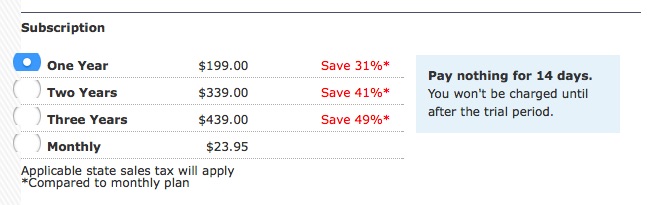

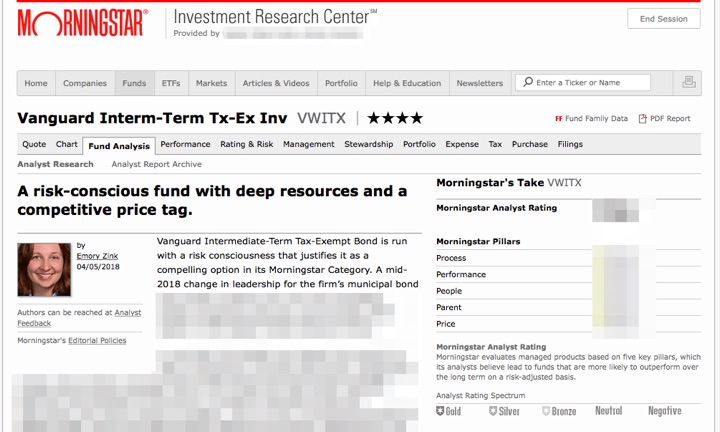

I’m never really sure what to call it, but Marcus (formerly Goldman Sachs Bank) is offering a $100 bonus if you deposit $10,000+ in new funds into their online savings account within 10 days of enrollment at this special offer page. You must enroll by 11:59pm EST on 3/18/19 and maintain the new $10,000+ deposit for 90 days. They will deposit $100 into your account within 14 days, after those 90 days (got it?). Both new and existing customers are eligible, which is nice.  Updated 2019. Let’s say you are a DIY investor and doing some research on some mutual funds. You decide to learn more about the Vanguard Intermediate-Term Tax-Exempt Fund. You pull up the Morningstar quote pages (ticker

Updated 2019. Let’s say you are a DIY investor and doing some research on some mutual funds. You decide to learn more about the Vanguard Intermediate-Term Tax-Exempt Fund. You pull up the Morningstar quote pages (ticker

Here’s my monthly roundup of the best interest rates on cash for March 2019, roughly sorted from shortest to longest maturities. Check out my

Here’s my monthly roundup of the best interest rates on cash for March 2019, roughly sorted from shortest to longest maturities. Check out my  DiscountMags.com is running their

DiscountMags.com is running their  The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)