I ran across a BusinessWeek article today about retirement plans in 2008 from top 401(k) provider Fidelity Investments. It stated that although the average retirement account balance fell a whopping 27% to $50,200 last year, people actually contributed slightly more in 2008 than in 2007.

This quote also caught my eye:

Are investors making a lot of changes within their retirement accounts?

Some 60% of plans administered by Fidelity in 2008 utilized a lifecycle fund as a default investment option, that’s up from 38% in 2007. What happens in a time of short-term volatility is that investors in these funds are not switching. Only 1% lifecycle fund investors made a change compared to the overall average to 6.1%.

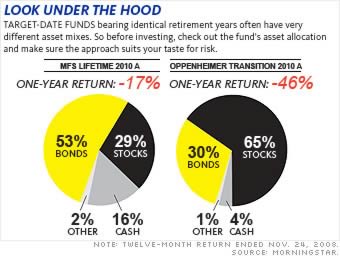

Makes sense overall. Investors in these types of funds want all-in-one simplicity. However, almost every company these days offer a lifecycle retirement fund. And most 401(k) investors can only invest in the one that happens to be in their plan. Check out this Money magazine example of the possible extremes out there for a mutual fund designed for a worker retiring in 2010:

On the aggressive side, the Oppenheimer Transition 2010 Fund (OTTAX) has 65% in stocks for someone on the verge of retirement, resulting in a 46% loss in 2008. On the conservative end, this AP article has an even better example – The DWS Target 2010 Fund (KRFAX) only has 18.1% in stocks and only had a 3.6% loss in 2008. The rest was in cash and bonds. (Of course, it also had a fat front-end load and is closed to new investors.)

That is some pretty stark contrast. Do you know what is inside your target-date fund? Dig up the ticker symbol, plug it into Morningstar, and scroll down to “asset allocation”.

What about the big boys like Vanguard?

Even the most highly-rated mutual fund companies don’t agree on the asset allocation for each time horizon. See how Vanguard, Fidelity, and T. Rowe Price differ in their target-date retirement funds.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

This is a great and timely post.

Asset allocation, whether you buy it in the form of a target date fund or create it yourself in your retirement account, is one of, if not the, single greatest contributor to your performance, according to Yale Chief Investment Officer David Swensen. Because of this fact, you should have an up to date view of your accounts to see how your asset allocation has changed as a result of the market turbulence.

Today we launched the most robust asset allocation view of your investments at Cake Financial- for free. Simply connect your retirement and brokerage accounts, click on the “Portfolio” tab and you can see your a summary and detailed view of all of your investments.

It is better than anything you can get at your brokerage firm and you can see across all of your accounts. Check it out and let me know how it works for you.

i did a comparison recently (2 wks ago?) between TRP and Vanguard retirement funds and now they are within 5% of eachother with respect to allocation in equity vs. fixed-income. i don’t know if that happened due to rebalancing (Vanguard may be overweight in stocks due to the decline in the market) but it is a distinct difference from when i first compared them back in early 2008. The point being that the asset allocation within these funds fluctuates slightly within a range thereby making it difficult to pin down the “exact” differences in the portfolios.

How did a 65% stock portfolio lose 46% in 2008?!?!

By comparison, a portfolio 100% in either Vanguard 500 fund or Total Stock Market Fund would have lost about 37% in 2008.

Not trying to push Vanguard or anything, but their Target 2015 fund which is approximately 65% stock only lost 24% on the year.

Did the Oppenheimer fund put that 65% of soon-to-be-retirees’ money in the riskiest of equity subclasses?

Here is a question on expense ratios for Target Date funds. Using Fidelity Freedom 2040 as an example, the expense ratio for the fund is 0.78%. But then it holds as part of it (being a fund of funds) the Fidelity Small Cap Growth fund (amongst others). The Small Cap Growth has an expense ratio of 1.11%. So my question is, isn’t the composite expense ratio for the 2040 fund significantly higher than the 0.78%?? Don’t the expense ratios for all of the underlying funds need to be taken into account?

Been wondering about this for a while so any insights are appreciated…

Good post. This is a good example of buyer beware!!!!!!

I don’t know if it is becuase these funds are “marketed” with a target date or what, but people seem to gravitate to the date not the asset allocation.

If I follow the numbers I should be in Vanguard 2030 but with 80/20 AA to rich for my blood. I am in an earlier Target Fund.

Information is good but knowledge is power.

Medgar

Andy,

my understanding is that since the asset allocation between invested funds in these umbrella “Target Retirement” funds is not equal, the proportionate expense ratios will also not be equal. Put another way, 1.11% for a fund that makes up <15% of the overall portfolio does not have the impact that 0.5% of a fund that is 50-60% of the portfolio. I believe those are all taken into account into the overall expense ratio of the Target fund.

Oppenheimer had HORRIBLE performance in their bond funds. So while you’d expect that 30% in bonds would offset losses in the stock market in this case their bonds performed as bad or worse than the equities.

Their core bond fund lost 35% YTD for 2008 and their “champion” income was down a massive 78%. Compared to a bond index which would be UP 5% or other bond funds that are down only 4-5% YTD. It appears there was horrible mismanagment of their bond funds..

21% off the Oppenheimer 2010 fund is made up of the Oppenheimer Core Bond fund and 3% is made of the champion income bond fund. So the really bad bond fund performance really drug down the performance of the Oppenheimer 2010 fund even more. The bonds should have helped offset the bad stock market performance but they didn’t help at all.

Wow, thanks for the comments guys. I’m 24 but am looking at opening up a 401k or IRA and would love some insight that I can’t find on my own.

Do you think now’s a good time to open a retirement account? I read an article on another website that talks about how my generation has absolute bargains when opening a retirement fund in this environment, but I think the market will go and stay much lower before it gets better.

Andy 11:00am –

I called Fidelity and asked the same question on expense ratios. I have access to the Pyramis Life Cylce funds and I am in the 2030 version of that choice. Fidelity needs to train their people better. The first three people I spoke to could not answer the question.

I finally got an answer and YES the underlying funds expense ratios must be taken into account. So the LOW expense you see for the Pyramis Lifecycle 2030 fund is not truly showing the costs. You need to drill in to the funds and look at each expense ratio.

Another rip off in my opinion. My plan this year is to only contribute to get the max match from my company, and invest the rest in non-retirement brokerage accounts where I can choose my own low cost investments.

My target date fund is available through my 401(k) at work. I only have one “brand” available, but different dates

So I can’t pick between Oppenheimer, vs another. I can only pick Fidelity because that is what is offered in m,y 401(k)

The ‘Target’ retirement funds generally DO NOT charge an expense ratio OVER AND ABOVE the expense ratios of the individual funds underlying the diversified portfolio mix. More specifically, the estimated expense ratio of ‘Target’ funds is generally based on a ‘composite’ (i.e., weighted average) of the expense ratios of the underlying funds.

The dramatic differences in allocations within different target retirement funds intended for the same time horizon investors makes the point that these funds are poorly designed overall. You would be better off from asset allocation and cost aspects to select a proper combination of index funds and ETF’s and stick with them until you retire. May I suggest you look at some of the couch potato portfolios, particularly the ten speed portfolio which includes a variety of generally non-correlated asset categories.

financePhi, yes if you’re 24 then now is a great time to start a retirement account. Starting saving for retirement EARLY is one of the best things you can do.

Jim,

Thanks for the reply. I think the consensus is that if you are in it for the long run, things will eventually find their way up.

@financePhi: Do you think now’s a good time to open a retirement account?

Is today a good day to start working out?

Is today a good day to start learning the guitar?

Is today a good day to start volunteering?

yes…yes…yes…

But let’s put this all in context.

You are your #1 retirement asset.

And let’s call a spade a spade. You probably don’t want to retire, you probably want to achieve “financial independence”. Most people don’t want to stop adding value to the world, they want to stop being tied to one job they don’t always like.

…my generation has absolute bargains when opening a retirement fund in this environment…

You can be financially independent without ever owning a stock certificate. On the other hand, you could own a handful of US stocks and earn 15% / year for the next decade and still have less purchasing power than you did when you started. Heck the government is “printing” 10% of the GDP this year, the average “retirement” fund is bleeding purchasing power.

Even if the markets have “bottomed” and you make 20% on your stocks in the next two years, you could still have less real purchasing power.

So before you jump on the 401(k) train, start by focusing on your goals and asking the right questions:

Your goal: is financial independence and quality of life.

Does a “retirement fund” help you achieve those goals?

Is the “retirement fund” the correct place to start?

How’s your education?

You’re currently 24, do you have a post-secondary degree?

Are you working towards related professional certifications?

How much money and time have you invested in your career?

What’s your current professional development plan?

Do you have marketable skills outside of your primary source of income?

What other sources of income are you building?

Are you adequately insured?

Do you have positive cash flow after covering your “quality of life expenses”?

When do you want to achieve this financial independence?

What quality of life do you want then? What about now?

Why did I just ask you like 20 questions?

Because the answer to your question “is this a good time”, depends entirely on the answer to the rest of these questions above (and probably a few more). Anyone pretending to answer your question without these other answers is just full of BS.