In November 2012, I invested $10,000 into person-to-person loans split evenly between Prosper Lending and Lending Club, both out of curiosity and for a chance at higher returns from a new asset class. After diligently reinvesting my earned interest into new loans, I stopped my after one year (see previous updates here) and started just collecting the interest and waiting see how my final numbers would turn out at the end of the 3-year terms.

In November 2012, I invested $10,000 into person-to-person loans split evenly between Prosper Lending and Lending Club, both out of curiosity and for a chance at higher returns from a new asset class. After diligently reinvesting my earned interest into new loans, I stopped my after one year (see previous updates here) and started just collecting the interest and waiting see how my final numbers would turn out at the end of the 3-year terms.

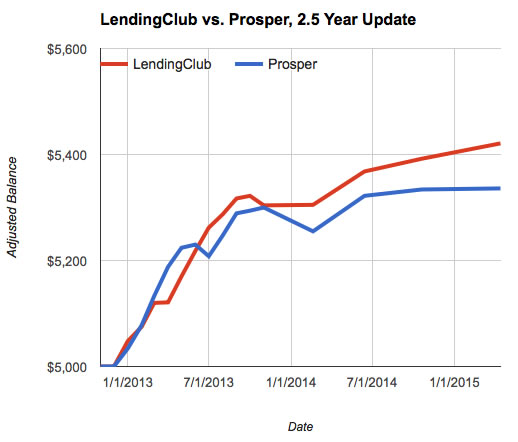

My last update was 6 months ago, so here’s what things look like after roughly two and a half years. This will be my last update before final liquidation of my portfolio (see recap below).

$5,000 LendingClub Portfolio. As of April 14, 2015, the LendingClub portfolio had 129 current and active loans remaining with a principal value of $1,003 (1 in grace period). 96 loans were paid off early and 29 were charged-off . 1 loan is between 31-120 days late and 2 are in default, which I will assume to be unrecoverable ($37.07 in principal). $417.94 in uninvested cash is left in the account, and I also withdrew $4,000 previously (payments and interest). Total adjusted balance is $5,421.

$5,000 Prosper Portfolio. My Prosper portfolio now has 110 current and active loans with a principal value of $1,404. 114 loans were paid off early, 42 charged-off. 1 loans are between 1-30 days late ($22). 3 are over 30 days late, which I am going to write off completely (~$18). $410.26 in uninvested cash is left in the account, and I also withdrew $3,500 previously (payments and interest). Total adjusted balance is $5,336.

Experiment Recap and Conclusions

- P2P lending has successfully gone mainstream. The fact that institutional investors are buying a significant portion of Prosper and LendingClub loan inventory would seem to prove that the concept is viable. This WSJ article says 66% of Prosper loans in 2014 had been sold to institutional investors. What started out as the Wild West of unsecured loans is now accepted by Wall Street. LendingClub had a successful IPO in December 2014 (which they generously let their lenders participate in).

- LendingClub reports my adjusted* annualized returns as 4.30% annualized. Prosper reports my annualized returns as 4.10% annualized. These returns are certainly above that of a savings account or bank CD, but not as good as many other asset classes over the same period. Considering the weighted average interest rate on those loans was 12% for LendingClub and 14% on Prosper, I saw a lot of defaults. (*Adjusted means you assume all loans 30+ days late will be total losses.)

- My reported returns consistently deteriorated as my loans aged. 10 months ago Prosper said my returns were 5.76%. 14 months ago Prosper said my returns were 7.55%. LendingClub reported my unadjusted annualized return 6 months ago as as 5.27%. 10 months ago, it was 5.94%. The lesson here is that your returns will continue to vary and likely deteriorate as your loans age, so don’t assume your returns will always stay the same as they are in the beginning. Also, your returns will look higher if you keep reinvesting into new loans.

- I am not a good loan picker. But will you be better? My returns are below average when compared to the advertised historical numbers. Certainly, I have seen reported numbers from other people who have done much better. Who knows, you may be the next P2P Bond King! 🙂 But I took my shot, diversified into over 400 loans, and here are my honest results. Not everyone who gets bad returns is willing to share about them.

- For small-time individual investors, dealing with unfamiliar forms at tax time can be tedious and time-consuming. Dealing with the tax forms each year isn’t impossible, but it isn’t fun either. If I were to invest all over again, I would definitely do it within an IRA to avoid tax headaches. To save more time, I would also buy at least 100 loans x $25, which also happens to be the $2,500 minimum for free auto-investment at LendingClub (no minimum at Prosper).

- I plan on liquidating the rest of my portfolio by the end of 2015. In June 2014, I still had $5,493 of principal in active loans in both LendingClub and Prosper. (The rest was idle cash, mostly withdrawn.) Now, roughly 10 months later, I only have $2,407 in principal and my total balance grew by a measly $67. $67 dollars! After filing my 2014 tax returns, I decided it was not worth the headache of dealing with the 1099s involved with these little loans. Thus, I plan on selling my remaining notes on the secondary market, probably soon but definitely by year-end. I might try again in the future inside an IRA, but for now I choose simplicity.

- LendingClub vs. Prosper relative performance. I tried my best to invest at both websites with the same criteria and overall risk preference. As noted, my LendingClub reported returns (4.3%) are a bit higher than my Prosper reported returns (4.1%). This is also supported by my own balance updates, although I wouldn’t put too much importance on the absolute numbers as I stopped reinvesting into new loans after the first year. Here’s an updated chart:

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Thank you for your efforts on this. Glad you made some money in the process 🙂

Did you sign in every day to reinvest the excess cash and rejected loans? It’s not supposed to be “completely” passive….

I go back and forth on LendingClub. As far as I can tell using my own calculations, I generally am getting 7-8% return. I do not really trust the returns they report, though I believe their calculations have become more accurate over the past year. I’m mostly satisfied with my return, but the account it a PITA overall. I have to login several times a week to list late notes, and often spend time to pick new ones. Automatic investing is decent, but doesn’t allow me to specify certain criteria. And yes, doing taxes on the account is a pain. Also, it does appear institutional investors are scooping up most the desirable loans. I have had to continually loosen my criteria just to keep my money invested. If money market accounts were ever to return to a normal (i.e higher than inflation) interest rate, I would probably more my money back to a MMA.

What certain criteria are you looking for? They seem to have many choices, and don’t recall thinking that something was missing.

The one I can remember offhand is a listed job title. A lot of apps just say “n/a” for that. If someone isn’t willing to tell me what they do for money, I generally don’t want to loan to them. And if they are retired or independently wealthy, then they probably shouldn’t need to borrow money. Job title is not a filterable criteria. There’s another 1-2 criteria I wish they had, but can’t think of them at the moment.

The other job title I see a ton of is “Owner”. I don’t do business loans. If an applicant lists their title as Owner, how can I really be sure what they are using the money for. Is it really to pay of credit cards, and are they taking a stealth business loan. I would prefer to be able to filter the Owner job title out.

I see. I also don’t recall seeing that. I guess I focus more on debt to income ratio, that they do have, in order to gauge how risky the loan will be. I know people that are making 100k that live paycheck to paycheck and people that make 20-30k that save half their income. I think lowering the loan amount will ultimately help in repayment. This is why I only do less than 15k loans, easier to repay even when they find themselves in a bit of financial distress. If one loans 25-35k, easier for borrower to just give up and deal with the bad credit.

I learned some valuable lessons from Prosper when it came to P2P loans back in 2007. When you started your Lending Club experiment I also decided to give it another try using Lending Club instead, but made many changes to the way I picked loans. I ended up with 336 loans, spread out over A, B, and C rated borrowers only. The majority of loans issued were to B borrowers, A~32% B~65 C~3%. I’m 22 months into the loans and ended up with 2 charge-offs and 2 more that are over 30 days late, but other than that I have little complaints this time around. My adjusted return is at 8.97%, at least for now.

So what did I learn and change from before?

1. All my loans were set to $25, to spread out risk and I was extra careful with the loan criteria.

2. I only loaned to borrowers that were asking for less than 15k.

3. The loan purpose had to point to consolidation and not acquiring more debt. I stayed away from loans for business use as I saw many defaults of this type from Prosper.

4. Length of employment over 1 year.

I really enjoy that Lending Club lets me setup this criteria as a filter for automated loan purchasing. With Prosper I hand picked each loan but with Lending Club I was able to set it and not worry about hand picking loans. It saved me much time, and it took out the emotional part of P2P loan investing that I think contributed to picking bad loans from my Prosper days.

Maybe this helps someone else decide if P2P investment is for them. At the end of the day, the return should make the risk worthwhile. If I can stay above 7% then it is worth it for me, if not, I’m perfectly happy with my Vanguard funds.

Anyone else have good tips or cautionary tales of P2P investing?

I’ve been using LendingClub since 2009 and have been pretty satisfied. The tax work is a pain though I’ll admit.

My criteria tend to be: $25 per loan, A, B or C loans only, 60 months or more since last delinquency, 3-year duration only, min 2 years of employment, max debt to income at 25%, max loan amount of $25k, and I check through every request to see how long they’ve had credit, months since last derogatory, etc. I will not loan for businesses or weddings because I’m not sure that most of them will outlast the time needed to pay off the loan.

I’ve had 845 loans, broken down A=57%, B=36%, C=7%, and the default rate for me has been 6%. The defaults seem to be rising from what I’ve seen – maybe it’s because the changes to what loans are available to individuals now. I’ve been thinking about stopping the reinvestment and start withdrawing.

Thanks for providing your strategy, Ern. I’m a little nervous seeing the 6% default rate, as I have a similar strategy and currently enjoy close to a 9% adjusted return. I’m hoping that your experience is not a preview of what is to come. My oldest loan is 22 months old.

What is your adjusted return after this many defaults? Have you taken a look at where those defaults are coming from? I guess I’m hoping that most originate from your C borrowers, or from bigger loans, like over 20k.

I’ve been testing Lending Robot, which is supposed to be a smarter/fastest way to get better loan. It’s too early to say if it’s worth it but since I’m not investing enough to use the auto-invest of Lending Club..

Direct Link https://www.lendingrobot.com

Referral Link https://www.lendingrobot.com/ref/KYHzd163/

An alternative to p2p lending is crowdsourced investing. I’ve been using a site called Kickfurther which allows you to invest in small businesses by helping them purchase inventory. These companies usually take out a loan in order to help pay for new purchase orders, but the terms can be quite onerous. So on Kickfurther they can raise funds from us instead! In return for our help we get interest. The interest rates are 6-10% for 4-6 months, so if you reinvest that’s 20-30% per year!

I’ve already gotten paid back on 3 offers, made about 10% on each within 2 months. These included an organic body care company and a “smart” backpack company. Check it out! They’re offering a signup bonus as well, click my website link to check it out.

This is an excerpt from their site. “What is the guarantee on the return?

If the goods don’t sell or the company goes bankrupt, we will take ownership of the balance of inventory on your behalf. You then have an active decision to make: we can help you liquidate the goods or you can take physical posession and sell them yourself.” I don’t think I want to deal with selling stuff. I like passive investments, not deal with headaches.

This sounds too speculative for me. Even more so than when I first heard of P2P Lending. Also, I like Lending Club because they are transparent. They show you data, the historical returns and defaults. This company doesn’t appear to do that.

Would you mind displaying your returns for all to see? Or maybe Jonathan may want to invest here to give us a preview of this business model?

I’d be happy to, but there’s not a huge amount of data yet. I’ve invested for about 4 months now, haven’t seen any offers fair to pay. I started with small amounts, $100 per company, and I’ve made $30 so far. Not bad, I’m increasing the amounts I invest now. I’ll see what I can put together to visualize it.

“These returns are certainly above that of a savings account or bank CD, but not as good as many other asset classes over the same period.” Could you give a few examples of “other asset classes” ?

S&P 500?

Check out the bottom of this post for some junk bond returns, which I think are the closest asset class that is easily accessible to most investors.

http://news.morningstar.com/fund-category-returns/

Oops, I meant to include this link. The Morningstar link is also worth mentioning though.

https://www.mymoneyblog.com/lendingclub-realistic-return-expectations-chart.html

With all the time and efforts spent in picking notes, and a low return rate, simply investing in S&P 500 index fund seems so much better an alternative -it gives 10% return anuually over long term. I guess the only down side of the latter is that you might need to stick with it for 20 years if you invest in a bad year.

Another annoying factor that made me walk away from LendingClub is that cashing out all the notes is such a pain!

I’ve invested in both Lending Club and Prosper. My return on Lending Club is 8.69% (over 500 loans) and at Prosper it’s around 7% for 375 notes.

After looking at both accounts, I noticed that Prosper’s defaulted loans were more “A” loans!!! Someone did a poor job of qualifying these borrowers – or they were trying to jumpstart their borrower business by attracting more borrowers with their ultra low interest rate on A loans.

I only invest $25/loan – spread the risk. I’ve noticed in most defaults, they happen early in the loan (fraudulent borrowers, I believe). I used to invest mostly in “B” loans. I “auto-invest” at both companies.

At Lending Club, I then changed to more “C” loans – more interest, and surprisingly, less defaults.

I started thinking – if I invest in a “good borrower” (A or B), the interest rate is really low – and so should the risk be – but just not much total return :(. Then, I tried adding some in “D and E” loans….much higher interest rate, but defaults were NOT really any worse than a B, ….But at least if they default, I’ve received almost as much total interest $ in a couple of months as I did with the A & B’s did at full term (3 yrs). My head can’t be bothered to figure out the logic/math….I’m just reporting my tactics and how I’m maintaining over 8%. Can anyone else here figure out why this works and tell me if it makes sense?

My charge-offs were not that bad – was only about $225 (some are recovered) when I did my taxes. And, the taxes were surprising easier to do than I thought they’d be (using TurboTax).

“After looking at both accounts, I noticed that Prosper’s defaulted loans were more “A” loans!!!”

I also noticed this with Prosper, and is the reason why today I only use Lending Club.

“I only invest $25/loan – spread the risk. I’ve noticed in most defaults, they happen early in the loan (fraudulent borrowers, I believe).”

Yes, I also noticed this with Prosper but not with Lending Club.

“Then, I tried adding some in “D and E” loans….much higher interest rate, but defaults were NOT really any worse than a B, ….”

After Prosper I no longer try anything lower than C’s, and frankly I only have 10 of those. Most of my loans are B’s and I also have an 8% return. I think the answer is simply sample size. Even 500 loans is small when dealing with probabilities. 2 different portfolios, even with the same investment strategy and same number of loans will ultimately have different results if they invest in different borrowers. The statistics that come with credit ratings are probabilities and not absolutes. It’s an educated roll of the dice but still a roll.

I wish you continued success with your P2P loans!

Frank,

Thanks for your feedback and reasoning. Also, I read your earlier comments about how you pick loans. I’ve found the same thing! More defaults on “Home improvements”, and that type. Better results on Debt Consolidations.

Prosper had a lot more defaults – I especially noticed those loans taken out in 2012 – (I think they eased the qualifications – even AA loans defaulted. Is that the year that Prosper was trying to revamp their business? I don’t really like Prosper compared to Lending Club – I will gradually cash out. Even doing taxes, Prosper supplied minimal info – while Lending Club spelled it out better and even included an example.

That’s great about your “B” loans – I added some “C” loans because the different in the interest rate was better and the defaults were no worse. (I have only about 20% of D & E). Good luck everyone 🙂

I honestly wish I’d never heard of Lending Club. I’ve got $10k invested, but for the time involved it’s sooo not worth it. And then taxes are something of a pain.

And I think these loans are a LOT more risky than junk bonds, and if the economy crashes again, investors are going to take big haircuts.

There are two people making big money on this: LendingClub and the bloggers who earn referral fees.

I commend this blogger for being honest. It’s why I read every one of his posts.

But if I could quickly and easily get out of ALL of my notes, I would and I would buy Vanguard High Yield Corporate with the money and never look back.

It was still a good experiment.

At this point, after reading this, I’m thinking I should just stop logging in, just let all loans play out whatever they are going to play out over next 4.5 years (I’ve been reinvesting), and then cash out and move on.

Good luck to all.

“I honestly wish I’d never heard of Lending Club.”

I thought the same thing the first time I used Prosper, but I no longer feel that way. I took a second look when Jonathan started showing his initial returns before they took a dive. A better investment strategy, than previously with Prosper, changed my outlook. No reason to invest in risky borrowers. I do fine with mainly A and B borrowers.

“But if I could quickly and easily get out of ALL of my notes, I would and I would buy Vanguard High Yield Corporate with the money and never look back. ”

I’m pretty sure you can sell your notes and get out right now. Check with Jonathan, as I’m sure he has experimented with selling notes in the past.

I like Vanguard’s corporate junk bond, in fact I’m more invested in this than P2P loans. What I still like most about Lending Club is not the interest I make, but the idea. The fact that we can directly compete with banks and take some business away is what sold me on it in the first place. When people are stuck paying a credit card to a bank at 20-30% you had no recourse but to pay or default. Now you can get out from a crushing interest rate by getting a group of investors to help drive down that interest. Everyone, except the bank, wins. The thought alone makes me happy, the fact that 7-8% returns are possible is simply icing on the cake.

Jonathan, thank you for taking on this project and reporting your findings.

I have 2 Questions for Jonathan/readers:

1. If you put a $ value to your time (ie – hourly rate for your time), would the time/cost spent investigating borrowers, establishing personal lending criteria, checking progress, determining tax compliance, filing or paying to file tax returns justify your continuing to participate in the P2P lending? Sounds like a lot of effort for actual return, for $$ that could very well be safely diversified elsewhere.

2. Are the loan defaults reported to credit bureaus? I’m guessing no, generally, unless a borrower decides to pursue?

1. I get your point, and from my initial experience with Prosper I would have agreed. The time it took to look at each loan request alone made it not worth it, but back then it was an experiment with a promise of an investment. The possibility of becoming a mini-bank was too alluring. However, things are way different now with Lending Club for my portfolio. The only thing that took effort was establishing a lending criteria. After that, the criteria did the loaning for me automatically. Taking what I learned from Prosper helped to establish the good returns I’m seeing now, even that didn’t take more than a couple of hours once you know what you’re looking for. The other things you mention I believe to be somewhat irrelevant. I would do those things anyway for any other investment, be it stocks, mutual funds, bonds… What investment is such a sure thing that you simply let it ride, year after year, without ever looking at it? My first try at P2P lending I may have also agreed with “Sounds like a lot of effort for actual return, for $$ that could very well be safely diversified elsewhere.” I’ve been investing long enough now to know that this statement is false. Unless you mean a savings account, there is no guarantee for investments that try to outpace inflation. Diversification does not shield you from a recession.

The one thing very relevant that needs to be said is the higher risk involved here. In my eyes, I would have to be making at minimum 7% in order to justify the investment otherwise it would be too risky. There are better lower risk and good reward options out there.

I’m curious to know what your safely diversified portfolio consists of. What investments do you like and how do the returns compare?

2. If they didn’t do at least that then why repay unsecured debt? I would not have invested otherwise. Taken from the Lending Club website… “Yes. Lending Club reports all account experiences—positive and negative—to one or more of the credit reporting agencies. Late payments, missed payments, or other defaults on your account may be reflected in your credit report, as will a record of on-time payments.”

Frank I appreciate your feedback – I should’ve had the notify box marked and then I would’ve responded sooner.

Sounds like you have a sound, disciplined approach to selecting investments and accordingly you’ve been rewarded for it… that’s great to see. Based on what I read in Jonathan’s entries about real estate crowd funding, applying the same approach & discipline to that could lead to strong returns there as well.

To your question, “What investment is such a sure thing that you simply let it ride, year after year” I do know of something rated about as safe as treasuries which yields higher than many bonds. If you’re familiar with the efficient portfolio frontier, with this particular opportunity long-term returns are well north of the vertex of the curve (essentially, much stronger expected returns with lowest risk). I’d be happy to tell you more about it personally, directly (if you’re interested to know more), but without revealing my contact information publicly and without asking you to do the same I’m not sure how to make that happen (unless Jonathan shares my contact information with you directly via email).

Picking loans is challenging and, as you noted, institutional investors are also in this game. They will fund the best loans quickly so the pool of available loans will probably be below average. Selecting the right criteria is not to hard to an extent, however, some filters that many people use (like verified income) are not correlated with loan default rate. I have studied all past Lending Club loans and determine which criteria actually work.

As a follow up to this comment, I have been thrilled to see extraodinarily high returns with Lending Club for the past 18 months. COVID relief seems to have enabled borrowers to remain current with their loans.