Last week, the average rate for a 30-year fixed-rate mortgage fell below 4% for the first time in recorded history. Why? The Federal Reserve and the US Government.

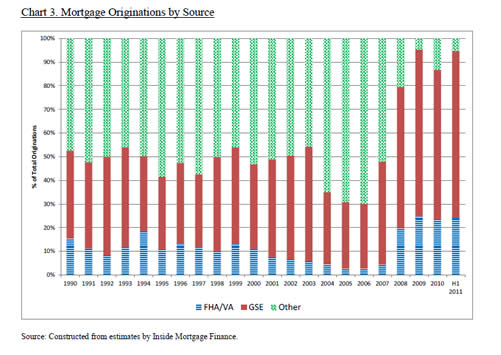

Check out this chart that breaks down the source of new mortgage originations for each year from 1990 to 2011. Blue is Federal Housing Authority (FHA) or Veteran’s Administration (VA), Red is Government Sponsored Enterprises (GSEs) including Fannie Mae and Freddie Mac, and Green is Other, presumably private sector mortgages held by banks and credit unions.

This is a fascinating and telling chart. In 1990 FHA/VA and GSE loans made up roughly 50 percent of all loan originations. This remained the story for the entire decade. The private sector got incredibly hungry with their toxic loans in 2004, 2005, 2006, and 2007. But look at 2008 up until today. For the last three full years, government backed loans made up over 90 percent of all loan originations.

Credit to Dr. Housing Bubble, found via AFM.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Unfortunately, most of the green in the “boom years” was NOT banks and credit unions (in fact, almost all mortgages originated by banks were backed by FRE and FNM). They were non-bank financial institutions, who did nothing but pump out as many mortgages as possible, and then securitize them and sell them to wall-street (this is where all the no-money-down, no-doc, stated-income, negative-amortization, baloon payment, “creative financing”, “NINJA” mortgages, etc. came from). Banks got a little crazy in these years, but nothing like the non-bank sector, which made up about two-thirds of the market. Those originators have all but disappeared.

NINJA is one of my favorite terms — No Income, No Job, no Assets. Seriously. Those people got mortgages too.

As a follow-up, it should be noted that even today, the Red is almost all bank and credit union mortgages. You can’t get a mortgage from a GSE. This post is a bit mis-leading. The only thing that has changed since 2007 is that the non-bank mortgage market has vaporized. Of course the other portions look bigger on a 100% scale like this. If you look at the absolute numbers, the Red section is probably smaller than it was.

@GregK

i was just going to say, id like to see the absolute numbers.

I’d argue that without Fannie and Freddie there is no private market for a 30-year pre-payable fixed rate mortgage, and if there is it is a significantly higher rates than we have seen in the U.S. in decades. No other market in the world offers this product, and the only reason the U.S. does is because we have had the world’s reserve currency and have essentially transferred that seignioriage benefit to homeowners.

There is no way that most banks and credit unions would be lending these days at current volumes at these rates without the secure knowledge that they can immediately sell these mortgage to Fannie or Freddie. That’s what the data here has been dug into to tell us the “real” originator. Of course, I didn’t compile this data so I don’t know the accuracy.

Some limited institutions keep mortgages in their own private portfolio, often jumbo loans that are non-conforming. These rates are always higher than conforming GSE loans.

so the government is essentially propping up the housing market.

the taxpayers should then be paid for originations and set higher lending standards

Banks,Insurance companies,drug companies,and arms companies are all on corporate welfare.They are the legal mafia.