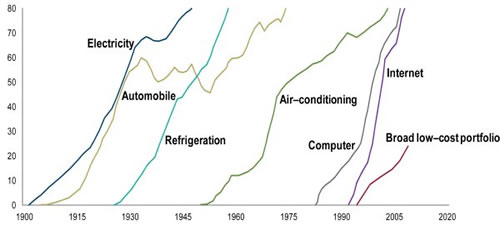

Joe Davis and Andy Clarke of The Vanguard Blog had a thought-provoking post comparing the increasing popularity of broadly-diversified, low-cost portfolios to the historical spread of certain technologies:

Much like electricity, refrigeration, and other great ideas, the broadly diversified, low-cost portfolio has the potential to raise our standard of living. […] The adoption of great ideas typically follows an “S” curve, starting slowly, then accelerating. Eventually, the great idea becomes commonplace. The adoption of the “broad low-cost portfolio” seems to be following this pattern.

Here’s a chart they created illustrating how the adoption of various technologies spread to include the majority of US households.

Defined as the percentage of U.S. mutual fund and ETF assets under management with annual expense ratios of less than 25 basis points (0.25%), low-cost investing has grown from less than 5% penetration in 1995 to about 25% of industry assets in 2012. Very few ETFs or mutual funds charge such low amounts unless they passively track an index, so at least right now low-cost is nearly synonymous with index funds. Will low-cost investing one day be as common as owning a car?

Tadas Viskanta adds more commentary in this Abnormal Returns post. It does seem like index fund investing has been gaining some momentum lately, partially because most hedge funds have been lagging major indexes for some time.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I wonder how returns will be effected as more investors move to low cost index funds…

Interesting idea. However, I see a possible a difference between low-cost investing and the examples shown such as autos, air conditioning, computers etc. That is the large “industry” that that makes its living from high-cost investments and expensive financial managers. They have a large vested interest in perpetuating the idea that stock-picking and fund-picking can consistently beat the market, and that the average person needs an expensive financial adviser because managing your own investments is just too complicated. They will not disappear without a fight.

I’m a complete devotee of the low-cost fund revolution, but we all have to admit something – we are all free-riders of those paying the fees of active management. I’m not an “efficient market” adherent; yet we do need active managers (whether it’s their own portfolio or that of others) to find fraud and mismanagement in the companies that we passively invest in. Of course one can debate how honest corporations are today, but without people reading proxy statements and disclosures looking (perhaps in vain) for a competitive advantage, I think we can agree that corporations would be less honest than today.

Yes, active managers don’t deserve the fees that they pull out of the pockets of too many Americans. But the whole investor class can’t be passive – we’ll start to get hoodwinked by the corporations that we are investing in. So, no, it’s not like electricity or TVs. At all.

I’m hoodwinked by this graph and what its trying to depict/infer.